SEI Forward

Trick or treat?

The third quarter prepared investors well for the upcoming Halloween season as several pivotal events heightened uncertainties regarding the direction of the economy, geopolitics, and capital markets. Will central banks deliver the treat of a soft landing, or will subsiding inflationary trends prove to be a temporary trick as stimulus measures and spreading geopolitical tensions act as catalysts for a reversal? Is broadening equity market performance a reflationary treat as the global economy remains robust and financing rates fall, or just the trick of a short-term junk risk rally? Finally, will long-term interest rates treat investors by following short-term rates lower or will the summer rally prove to be just a trick upended by overly simulative monetary policy and every increasing debt levels?

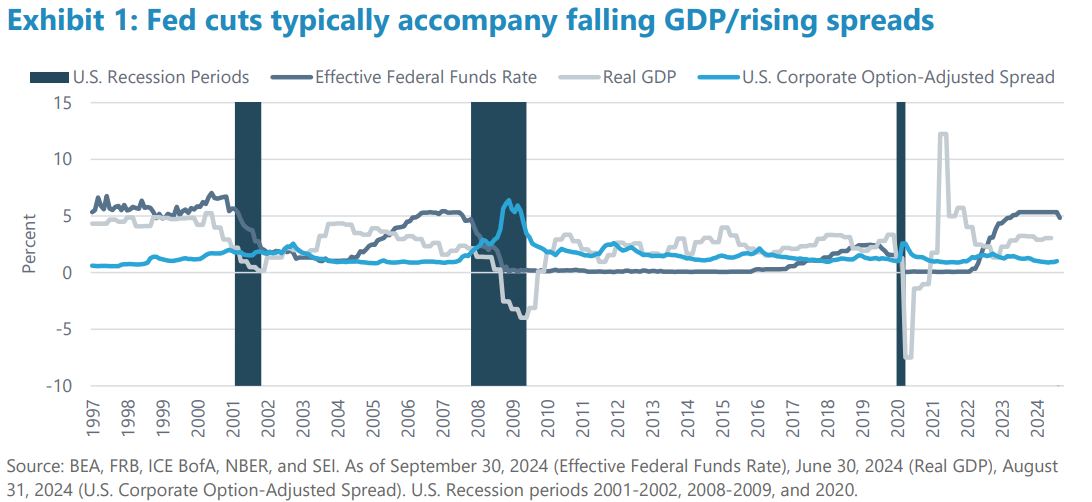

As we enter the final quarter of 2024, the world’s two largest economies are handing out plenty of sweets in the form of easing monetary policies and a broad range of fiscal stimulus measures that should provide ballast to the global economy. U.S. Federal Reserve (Fed) policy-makers delivered a somewhat surprising 50-basis point interest rate cut in September. It is likely to be followed by an additional 50 basis points of easing by year-end. Reductions in the federal funds rate, particularly of this magnitude, are typically accompanied by a decline in gross domestic product (GDP) and rising credit spreads.

This pivot to lower rates, however, comes at a time when third-quarter GDP is tracking at roughly 3%, stock markets are at all-time highs, and credit spreads are near all-time lows. Therefore, while we are not overly concerned with a bit of monetary policy stance adjustment at this point in the cycle, the market’s expectations for more than 200 basis points of additional cuts into 2025 seems, frankly, out of touch. Inflation remains well above target, and employment is showing signs of slack relative to the recent historically tight levels. Long story short, too much candy can be bad for the economy. We see a policy mistake brewing that should provide a short-term boost to risk assets, but also upwards pressure on long-term interest rates.

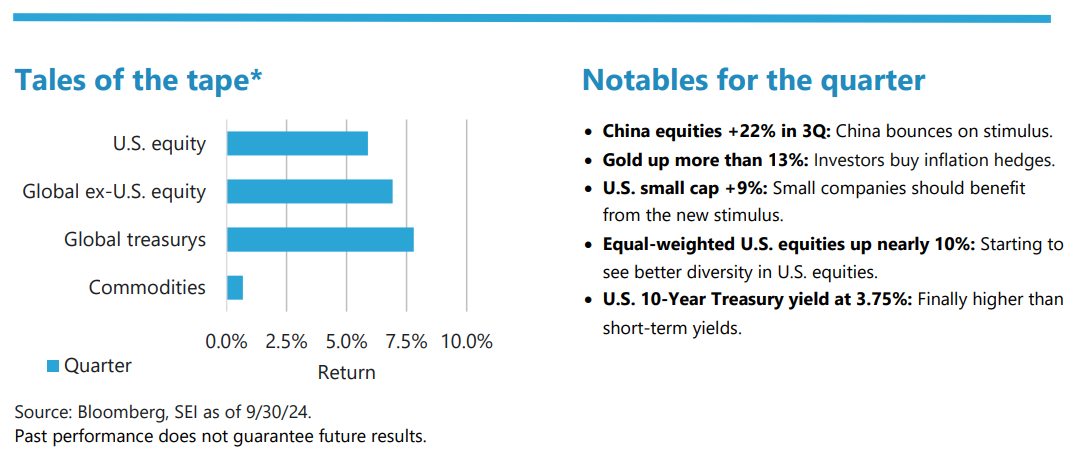

Outside of the U.S., the Chinese government finally blinked and put out its own candy bowl—a plethora of stimulus measures that were welcomed with open arms by frustrated investors. Interest-rate cuts, direct cash transfers, loan extensions, and programs that directly affect equity markets were all included in the sweeping policies introduced at the end of the quarter. The market’s reaction was swift, and Chinese equities finished the period as a top-performing asset class. Whether or not this short-term bounce has staying power remains to be seen. We remain interested observers at this point.

Finally, Europe remains a bit of a mixed bag economically; therefore, we expect the European Central Bank (ECB) to match the market’s dovish expectations for future policy moves. In contrast to our view that the Fed will disappoint, we see the ECB delivering, given the somewhat surprising and continued weakness in Germany.

The short-term sugar high from the stimulus candy bowl…

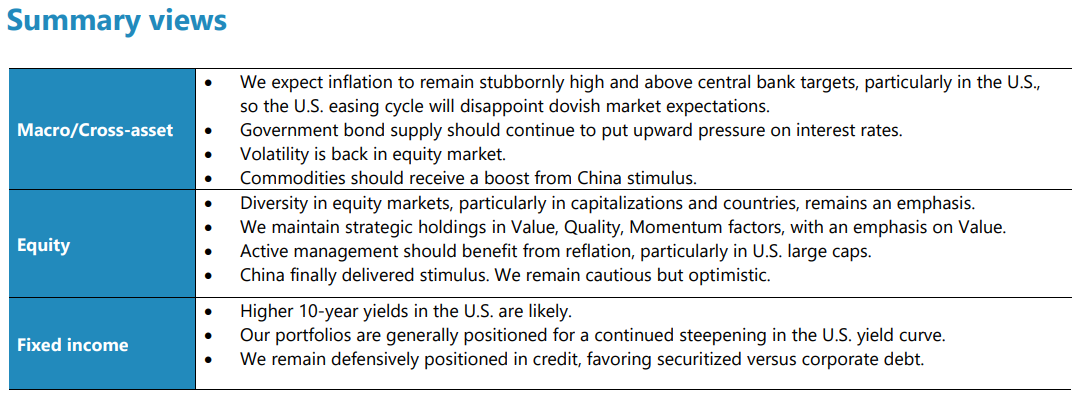

Given the near-term effects of early stimulus measures in the U.S. on an already healthy economy and the wide ranging efforts from China to prompt a rebound, we see lower recession probabilities and a favorable environment for risk assets in the fourth quarter. Broader participation in global equities is our key viewpoint, as performance should expand beyond a handful of names in a few sectors from one country. The rest of the world outperforming the U.S., emerging markets outperforming developed, small caps outperforming large, value stocks outperforming growth, and active management outperforming passive are all versions of the reflation theme we see potentially playing out for the remainder of 2024. Therefore, while we remain, as always, strategically diversified among profitable companies with strong earnings momentum at reasonable prices, we are particularly confident in global value and active management in the U.S. large-cap space. Value looks particularly attractive as the magnitude of the dispersion between cheap and expensive names has reached historically wide levels. Likewise, we favor active management in U.S. large caps given the unusually high amount of idiosyncratic risk in passive strategies from increased concentration in high-multiple, mega-tech names.

Our positive view on broad commodities has also been reinforced, in particular, by the Chinese stimulus efforts. Most complexes should benefit, including industrial and precious metals, despite the latter’s strong performance this year. Energy is worth another look as rhetoric from Saudi Arabia regarding increased production levels raises concerns; however, elevated tensions in the Middle East are enough of an offset in the near term.

…may haunt the economy with higher long-term rates.

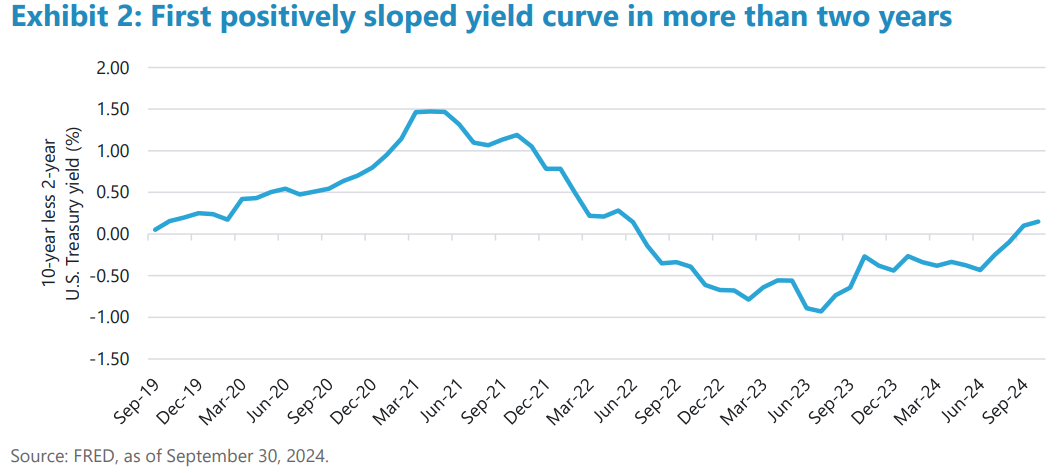

One of the key events of the third quarter was the sharp drop in interest rates as investors priced in central bank pivots around the globe. In the U.S. for instance, the yield on the 10-year note started the quarter at just under 4.50%, reaching a low of 3.62% just before the September Fed meeting. Interestingly, after the Fed lowered overnight rates, the 10-year yield rose to close out the quarter at roughly 3.75%. This combination of lower short-term rates but higher longer-rates finally reversed the two-year-long inversion of the U.S. yield curve. More importantly, we see this trend as the market beginning to question the effects of monetary stimulus and fiscal excess on longer-term yields. We couldn’t agree more. We see upward pressure on longer-term rates in the U.S. even with additional interest rate cuts from policy-makers in 2024.

Speaking of fiscal excess, we would be remiss to not mention the upcoming U.S. presidential election. While differences are stark between the two major-party candidates, there are actually areas of common ground. Unfortunately, one of those areas is a lack of any interest in reigning in government spending. As we have noted before, government debt has reached the point where it must be addressed. Sadly, entitlement reform remains a “third rail” in U.S. politics, which should keep upward pressure on long-term interest rates. With regards to the election outcome, for what it’s worth, our sense is that the most likely result in some combination of divided government, which tends to be the most favorable outcome for markets. We will not be positioning for anything specific, but will continue to emphasize truly diversified portfolios, which we believe remain the best approach in managing uncertainty.

Indexes

*Tales of the tape: U.S. equity: S&P 500 Index; Global ex-U.S. equity: MSCI ACWI ex-U.S. Index; Global treasurys: Bloomberg Global Treasury Index; Commodities: Bloomberg Commodity Index; China equities: MSCI China All Shares Index; U.S. small cap: Russell 2000 Index; Equally-weighted U.S. equities: S&P 500 Equally Weighted Index.

Indexes definitions

The Bloomberg Commodity Index comprises futures contracts and tracks the performance of a fully collateralized investment in the index. This combines the returns of the index with the returns on cash collateral invested in 13-week (three-month) U.S. Treasury bills.

The Bloomberg Global Treasury Index tracks fixed-rate, local currency government debt of investment grade countries, including both developed and emerging markets.

The MSCI ACWI ex USA Index tracks the performance of both developed-market and emerging market countries, excluding the United States.

The MSCI China All Shares Index tracks the performance of large- and mid-cap stocks in China. The index’s 151 constituents, comprise about 85% of the China equity universe.

The S&P 500 Index is a market-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

The S&P 500 Equally Weighted Index is an equally-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

The Russell 2000 Index tracks the performance of the small-cap segment of the U S. equity market. The index is a subset of the Russell 3000 Index, which comprises the 3,000 largest U.S. companies, and includes approximately 2,000 of the smallest securities based on a combination of their market cap and current index membership.

Glossary

A basis point equals .01%. A credit spread is the difference between the yields of two bonds with the same maturity but different credit quality.

The Federal funds rate is established by the Fed and is the interest rate that large financial institutions use to borrow/lend in the overnight market.

Gross domestic product (GDP) is the total monetary or market value of all the goods and services produced in a country during a certain period.

Momentum is a trend-following investment strategy that is based on acquiring assets with recent improvement in their price, earnings, or other relevant fundamentals.

The option-adjusted spread the measurement of the spread of a fixed-income security rate and the risk-free rate of return, which is then adjusted to consider an embedded option.

Quality comprises a long-term buy-and-hold strategy that is based on acquiring shares of companies with strong and stable profitability with high barriers of entry (factors that can prevent or impede newcomers into a market or industry sector, thereby limiting competition).

Risk assets, such as equities, commodities, high-yield bonds, real estate, and currencies, carry a degree of risk and generally are subject to significant price volatility.

Value is an investment strategy that is based on acquiring assets at a discount to their fair valuations. Mean reversion is a theory that prices and returns eventually move back towards their historical average.

The 10-Year U.S. Treasury Yield is the interest rate the U.S. government pays to borrow money for 10 years. It is also known as the 10-year bond rate and is a key indicator of economic conditions and investor sentiment.

The yield curve shows the interest rates for bonds with the same credit quality but different maturity dates.

Important information

Index returns are for illustrative purposes only and do not represent actual investment performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

The opinions and views in this commentary are of SIEL only and are subject to change. They should not be construed as investment advice.

This information is issued by SEI Investments (Europe) Limited (SIEL) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority (FRN 191713).

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

SEI sources data directly from FactSet, Lipper, and BlackRock unless otherwise stated.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This document has not been registered by the Registrar of Companies in Hong Kong. In addition, this document may not be issued or possessed for the purposes of issue, whether in Hong Kong or elsewhere, and the Shares may not be disposed of to any person unless such person is outside Hong Kong, such person is a “professional investor” as defined in the Ordinance and any rules made under the Ordinance or as otherwise may be permitted by the Ordinance.

This information is made available in Latin America, the Middle East, the Nordics, and Australia FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755- 1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This email and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa