A widening of the U.S. versus European central bank policy rates.

SEI has entered a position designed to benefit from the widening of relative central bank policy rate expectations over the coming year.

Federal Reserve vs. European Central Bank

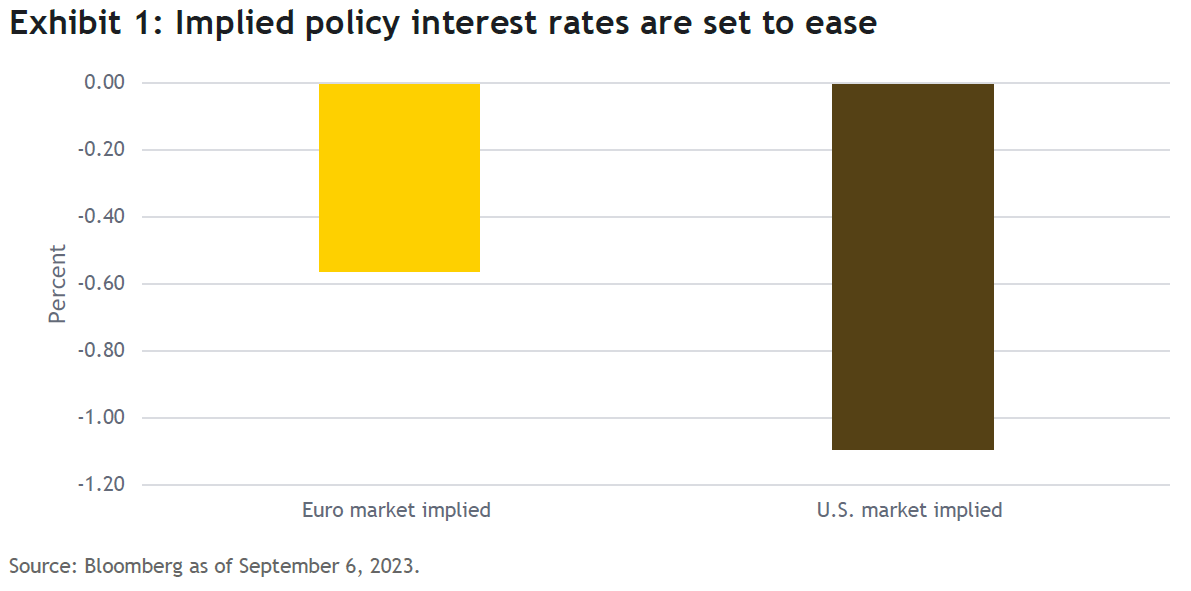

In the U.S., SEI believes the rates market has priced in overly optimistic expectations for interest rate cuts, given resilient economic growth and persistent inflation. In our view, the Federal Reserve’s dependency on economic growth and inflation data tilts risk in favor of higher short-term interest rates in the U.S. In contrast, the European rates market is priced for a more muted easing cycle. We view this as misaligned with the sharp deterioration in European economic activity. Accordingly, we believe the risk is skewed towards lower short-term interest rates for the European yield curve. As can be seen in Exhibit 1, implied policy interest rates indicate expectations are for about two 0.25% rate cuts in Europe. Meanwhile, the implied policy interest rates for the U.S. indicate the potential for about four 0.25% rate cuts.

In an effort to capitalize on these perceived dislocations we have structured a relative value trade that will benefit from the widening of the short-term rate differential in the U.S. versus Europe. As a relative value trade, the position may benefit from either reduced easing in the U.S. (fewer cuts than the market currently expects) or increased easing in Europe (more cuts than the market currently expects).

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice and is intended for educational purposes only. There are risks involved with investing, including possible loss of principal. Diversification may not protect against market risk

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information issued in the UK by SEI Investments (Europe) Ltd, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.