Virus Spread Rattles Markets

The coronavirus outbreak has accelerated in recent days, amplifying the anxiety of already-concerned investors about its impact on global growth and corporate earnings. As a result, global equity-market volatility has increased and share prices have declined. These events have understandably brought back some of the investor fear felt during the 2008 market meltdown.

We expect volatility to continue for the short-term—as long as the extent of the impact on global economic activity remains unknown, which will likely be until the virus runs its course. But once it does, we have every reason to believe that business activity will return to normal.

Market indicators: mixed messages

We are seeing a mix of current global economic news:

- Initial (“flash”) US Purchasing Managers Index (PMI) readings for February were surprisingly negative—with services at 49.4 versus an expected 53.3, and manufacturing at 50.8 versus an expectation of 51.5. (PMI readings are viewed as an indication of future economic activity. Readings above 50 are considered expansionary/positive. Those below 50 are considered contractionary/negative).

- On the other hand, eurozone flash PMIs improved unexpectedly. Manufacturing moved closer to expansion territory, increasing to 49.1 from 47.9 (beating the forecasted drop to 47.5). Services rose to 52.8 from 52.5 (surpassing an excepted deceleration to 52.2).

- Last week, China’s top leaders pledged a more proactive stance in fiscal and monetary stimulus, with the goal of limiting the outbreak’s impact on gross domestic product growth. If engaged, the efforts are expected to be broad-based. China also recently announced measures to alleviate debt pressures faced by small businesses as well as a temporary value-added tax exemption. Should the spread of the coronavirus slow, this stimulus boost could provide a tailwind to China’s domestic economy and create the potential for a quicker recovery.

- As of last Friday, 24 February 2020, S&P 500 Index blended revenue growth showed some upside surprise for the fourth quarter of last year. FactSet showed blended earnings growth for the Index in the final quarter of 2019, at 0.9% versus an expectation of -1.7%, with 87% of companies reporting actual results. In addition, there are encouraging results on the revenue side. Fourth-quarter blended revenue growth came in at 3.6% versus 2.9% forecasted, with 66% of companies beating top-line estimates. Obviously, the concern is in the future earnings guidance coming from companies after they evaluated the impact of the outbreak on their businesses. Of the 89 companies in the S&P 500 Index that issued their future earnings-per-share guidance, 61 guided lower for the first quarter of 20201—but that’s more or less in line with five-year averages. Anecdotal comments from US companies have mostly noted supply-chain disruptions due to reduced business activity in China.

Portfolio managers: business as usual

The coronavirus only became a prominent investor concern about a month ago. As such, we have seen little impact on the general views of our international and emerging-markets managers’, their ability to carry out their investment processes, or the way our managers cover stocks. While this could change if the problem persists, we would anticipate any disruption to be temporary.

In terms of on-the-ground activity, although mainland China is essentially shut down and Korea is on high alert, other cities (including Hong Kong and Singapore) are still accessible despite much less traffic. Singapore, in particular, is mostly business-as-usual despite the cancellation of large gatherings like conferences.

While investment manager research trips may be cancelled, phone and virtual meetings are still taking place, and networks of contacts continue to provide the same level of information, research and local insight.

Markets: muted outlook

As for the impact on stocks, the biggest uncertainty is how long this virus will last. Unfortunately, the forecast changes daily and there are many unknowns. While our managers are closely monitoring the situation, they have not made material changes at this point.

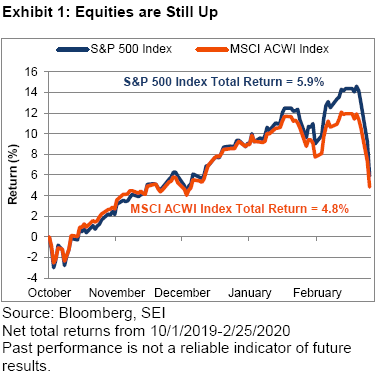

It’s also worth noting that major equity markets are still well-above where they started the fourth quarter of 2019 despite the sharp decline over the last few days (Exhibit 1) Extending that outlook back in time would reinforce the significant gains equities have posted in recent years. Some degree of pullback, whether virus-driven or not, is to be expected.

Important Information

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.