Value Stocks: Popular? No. Necessary? Yes.

Value stocks have been unloved for so long that it’s getting difficult to remember why anyone ever wanted them. From a portfolio construction standpoint, their unpopularity doesn’t change their appeal. From a stock picker’s standpoint, it makes them interesting.

Value defined

When we talk about value stocks, we’re typically referring to companies that have fairly well-established and stable business models. However, because they are well established, their prospects for high rates of profit growth are low. Value companies tend to be priced based on their near-term ability to maintain or improve upon current levels of profitability, as opposed to a more speculative assessment of the potential for future profits. They also tend to have attractive dividend yields. The fortunes of value stocks tend to be highly sensitive to the business cycle and, therefore, to changes in the strength of the underlying economy. For example, the financials and energy sectors contain a number of value stocks.

For value investors, the potential for compensation (in the form of near-term profits and dividends) tends to be more front-loaded, relative to growth-oriented stocks. This also means that value stocks are typically less sensitive to interest rates, as discount rates have less impact on nearer-term cash flows than longer-term cash flows. In a relative sense, low or falling interest rates may be bad for value stocks. By contrast, growth stocks with typically lower dividend yields that are priced according to their potential for generating profits in the distant future will often be far more sensitive to interest-rate moves. This is analogous to comparing a high-coupon bond (value stocks) to a low-coupon bond (growth stocks). All else equal, the high-coupon bond, with its more front-loaded compensation, will have less interest-rate sensitivity (or duration, in fixed-income terminology) than the low-coupon bond whose compensation is more back-loaded.

Interest rates and value stocks

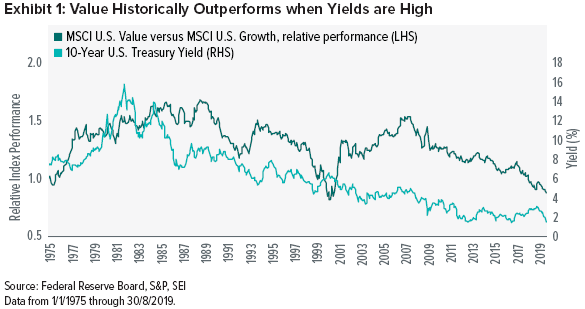

The current environment, with interest rates at historically low levels around the world—even negative throughout much of Europe and Japan—has provided a strong tailwind for growth-oriented sectors such as technology and consumer discretionary. While value stocks have not performed quite as strongly, they have still performed quite well overall. Exhibit 1 shows a long-term perspective on the relationship between interest rates and the relative performance of value stocks versus growth stocks. The historical record generally corroborates the idea that falling or low interest rates create a favourable environment for growth stocks, which puts value stocks at a relative disadvantage.

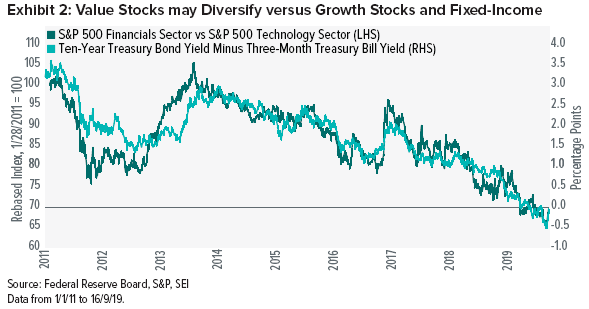

Historically, a trough in interest rates has resulted in the relative outperformance of growth over value, but also has signalled the start of a period of rising rates and of value outperforming growth. Rising rates have also historically challenged the performance of fixed-income assets. As such, a portfolio that has significant exposure to value stocks, as opposed to a more simplistic market-capitalisation-weighted equity exposure, may provide improved diversification versus fixed-income assets. Exhibit 2 shows this potential benefit by highlighting the positive correlation of the relative performance of financial stocks (a proxy for value stocks) and technology stocks (a proxy for growth stocks) versus the yield spread between 10-year Treasury bonds and 3-month Treasury bills. Because yields and prices move in an inverse manner, this demonstrates a negative correlation for the performance of value stocks versus fixed income. Negative correlations between investments are the most powerful implements of diversification.

We still believe in value regardless of interest rates

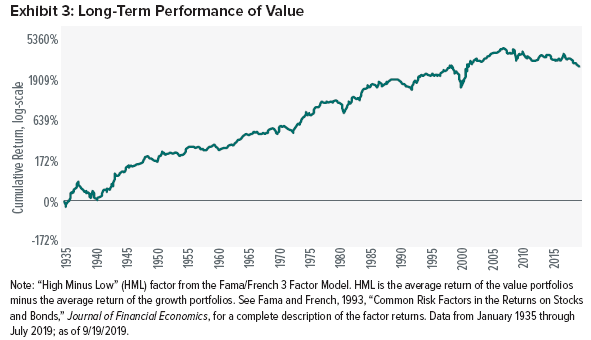

Over long periods of time, equity portfolios with a focus on favourable valuation characteristics have demonstrated a clear trend toward positive excess returns. Stock selection on the basis of valuation measures has been well documented as a source of excess returns. Having this sort of exposure or positioning within your equity portfolio makes sense on its own merits, but it becomes even more attractive when combined with the potential ancillary benefit of additional diversification versus fixed-income exposure. In our view, this diversification benefit is particularly worthwhile at a time when interest rates are near all-time lows.

Conclusion

Today, value stocks are trading at historically low valuations versus their growth peers. This makes them attractive. While it doesn’t guarantee the timing of potential outperformance, it provides a logical reason to invest in them. Performance and valuation aside, the tenets of diversification remain intact. It is impossible to say with complete certainty which asset class will outperform in a given period. Accordingly, in our view, value stocks should continue to have a place in a diversified portfolio.

Important Information

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information. Data refers to past performance. Past performance is not a reliable indicator of future results.

The opinions and views in this commentary are of SIEL only and are subject to change. They should not be construed as investment advice. This information is issued by SEI Investments (Europe) Limited (“SIEL”) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority (FRN 191713).