US/China Trade Tariffs Tax Markets

The recent trade stalemate between the US and China rattled investors,resulting in a modest stock-market decline. The unfavourable market reaction was understandable. Yet, as with other recent declines, we think this one will be limited in size and duration. Until we see many more negative fundamental developments—both in the US and globally—our long-term outlook will remain the same.

Not so Taxing

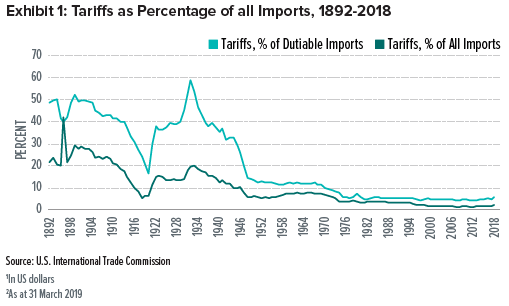

We find it hard to argue that tariffs implemented by the Trump administration have had a severely negative impact on the US economy. In fact, trade duties remain historically low; we almost need a magnifying glass to see their rise as a percentage of all imports. There is no reason to believe that current tariffs will cause the US economy to slow as they did in the 1930s, when levies were much higher and extended to most goods imported from far more countries, as highlighted in Exhibit 1. The additional 15% tariff on $200 billion1 of Chinese goods equates to a seemingly dramatic $30 billion tax increase. However, in the context of a $21.1 trillion US economy that includes $2.9 trillion of total merchandise imports2, an extra $30 billion in taxes seems less significant.

If the US applies more tariffs, American companies will likely begin to seek substitutes for the affected products. Currently, this includes mostly intermediate inputs and capital goods; last week’s round of increases affected the same items as those impacted in July 2018 and September 2018. Consumer goods have largely been left alone, which has softened the blow from tariffs for the average person.

China’s retaliation against the US has already reduced demand for US agricultural products, leading to fewer exports of American soybeans, corn and wheat to China. Yet this decline isn’t wholly attributable to Chinese retaliatory efforts. African swine flu has recently devastated China’s pigs and hogs, causing the country’s pig farmers to require fewer imports of American grain to feed their herds. While China’s retaliation against the US in response to tariffs may impact some sectors and industries, we think it can only go so far.

A Little Less Attached

The relationship between US and China began to unravel well before the Trump administration first applied tariffs. The US investment in China’s electronics industry had already been sliding for years. Meanwhile, Chinese investment in the US plummeted last year by over 80%—not only in response to US tariffs, but also because of tighter US government regulations on China’s investments amid security concerns. We view the growing divide between China and the US as an ongoing existing trend rather than the start of a new development.

Investors’ biggest concern is further escalation. The Trump administration is already considering imposing another 25% tariff on the remaining $325 billion of Chinese goods. China’s merchandise-goods exports to the US account for about 20% of total US imports and 20% of China’s total exports. These are significant numbers. If tariffs were applied to another tranche of Chinese products, it would be a huge deal—basically doubling the amount of tariffs that have already been applied. American consumers would definitely feel it—and see it in the prices of the goods they buy.

Still, we think China stands to lose more than the US if the trade situation is not resolved. The next round of tariffs would affect items such as toys, clothing and footwear—products that have low profit margins and employ millions of people in China. Doubling current tariffs would mean that most of these Chinese products would become uncompetitive virtually overnight.

Also, these types of merchandise do not necessarily need to be produced in China, which is considered a high-cost country for an emerging economy. Production could be moved over time to lower-cost Asian countries, such as Vietnam, Cambodia, Pakistan or Sri Lanka—another possible pain point for China if tariffs are applied to the rest of its US exports. In our view, the overall potential loss to the Chinese economy should be enough to convince the country to stay at the negotiating table.

Macro View: The US Looks Fine

While a few days of market volatility have rattled Wall Street, long-term performance remains strong. The S&P 500 Index is now valued near the upper end of its trading range3 over the last year at about 16x forward earnings. We expect earnings to continue rising, with year-over-year earnings gains in the S&P 500 Index north of 5% by the end of 2019. Such an advance would be far less significant than that of the last calendar year, but it would still be positive—and likely in line with most other regions of the world.

Although the US equity market recorded a strong annual gain in 2018, it fell hard during the fourth quarter of that year. Analysts were therefore busy reducing earnings estimates for 2019. However, by the time first-quarter earnings started to come out, we saw unusually large upward revisions of estimates. This reversal eased expectations of an imminent bear market, as earnings tend to fall on economic weakness before such a dramatic market downturn ensues. We don’t foresee a serious earnings slump. That is only likely to happen if we enter a recession.

We also don’t foresee the Federal Reserve (Fed) inducing a recession anytime soon. The inflation-adjusted federal-funds rate (which reflects the interest rate that banks charge when making overnight loans to other banks) is still much lower than at other points when recession hit. During the last economic cycle, the real rate (real rates are adjusted to remove the effects of inflation) was over 3% before recession occurred. Before that, in 2001, it reached well over 4%. Going back even further, in 1991, the real federal-funds rate surpassed 6%. As long as inflation remains near the Fed’s 2% target, the central bank has little incentive to engage in additional rate hikes. We expect the federal-funds rate to remain on hold for the rest of this year and perhaps into 2020, depending on what happens with the trade negotiations with China.

We previously thought an acceleration of US gross domestic product growth in the second half of 2019 may convince the Fed to raise the Federal Funds rate. With the current uncertainty, we now expect the Fed will continue to refrain from increases even if US economic growth accelerates.

Europe and the UK Look OK

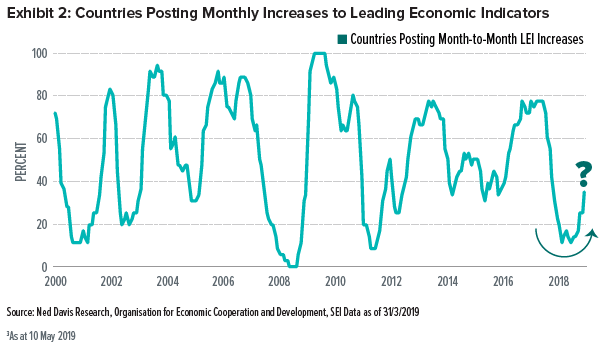

Two-fifths of the 37 economies surveyed by the Organisation for Economic Co-operation and Development reported month-over-month increases in March in its index of leading economic indicators as shown in Exhibit 2.

It remains to be seen how the current global stock-price pullback will impact future readings, but economic conditions in these countries have definitely been improving. Europe in particular has seen notable gains. The economies of both the UK and eurozone have seen positive shifts, with the data surprising on the upside since the start of 2019 despite slow growth and Brexit uncertainty. The US economy has also finally shifted to the upside in recent weeks, which was welcome news.

Currency Questions

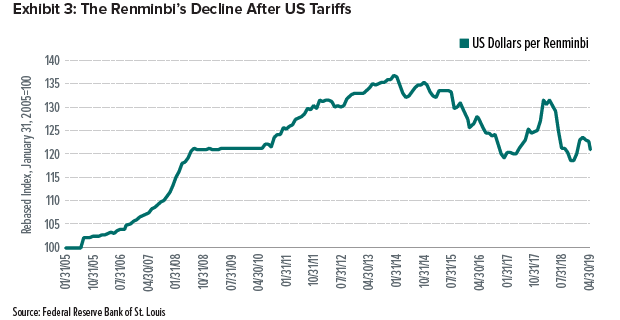

It should not be surprising that the Chinese renminbi (yuan) has declined against the US dollar in the aftermath of the latest tariff increases. The currency fell by nearly 10% after the initial round of tariffs last year, when the US applied a 10% tariff on $200 billion of Chinese goods, which basically offset any negative impact on Chinese exporters, as Exhibit 3 shows.

Whether the renminbi will decline further is a good question. We don’t expect it to be a one-for-one match against future tariffs, but it’s reasonable to expect a decline of between 5% and 10%.

The US dollar tends to rise in such periods of economic and policy uncertainty, but our outlook on America’s currency is mixed right now. It has yet to return to its peak achieved at the end of 2016, having only made begrudging gains in value on a trade-weighted basis. Neither is it showing signs of soaring higher, as it did in 2014. And we don’t expect it to. There are counter-pressures on the US dollar that reduce the chances of such gains, even in this uncertain period.

A rising US dollar could weigh on profit margins and revenues of multinational companies based in the US. We haven’t seen much downward pressure on profit margins thus far, since productivity improvements have offset the impact of rising wage and interest costs.

What’s Next?

As investors fret about whether trade talks will go from bad to worse, we expect further price corrections in the near term. With the underlying strength and resiliency of the US economy, however, along with the Fed maintaining rates and signs of improved global growth, we are confident that the downside in risk assets will be short-lived.

If anything, this situation only reinforces our mantra of “buying on the dip.” US equity prices have been resetting since the S&P 500 Index recovered from its 25% Christmas Eve bottom. We believe this should permit fundamentals to once again drive stock prices to higher levels later in the year.

Index Definitions

The S&P 500 Index is an unmanaged, market-weighted index that consists of 500 of the largest publicly-traded US companies and is considered representative of the broad US stock market.

Important Information

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

SEI Investments (Europe) Limited acts as distributor of collective investment schemes which are authorised in Ireland pursuant to the UCITS regulations and which are collectively referred to as the “SEI Funds” in these materials. These umbrella funds are incorporated in Ireland as limited liability investment companies and are managed by SEI Investments Global Limited, an affiliate of the distributor. SEI Investments (Europe) Limited utilises the SEI Funds in its asset management programme to create asset allocation strategies for its clients. Any reference in this document to any SEI Funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application must be made solely on the basis of the information contained in the Prospectus (which includes a schedule of fees and charges and maximum commission available). Commissions and incentives may be paid and if so, would be included in the overall costs.) A copy of the Prospectus can be obtained by contacting your Financial Advisor, SEI Relationship Manager or by using the contact details shown below.

Data refers to past performance. Past performance is not a reliable indicator of future results. Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Returns may increase or decrease as a result of currency fluctuations. Investors may get back less than the original amount invested. SEI Funds may use derivative instruments which may be used for hedging purposes and/or investment purposes. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events.

In addition to the usual risks associated with investing, the following risks may apply: Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High-yield bonds involve greater risks of default or downgrade and are more volatile than investment-grade securities, due to the speculative nature of their investments. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments, securities focusing on a single country, and investments in smaller companies typically exhibit higher volatility.

The opinions and views in this commentary are of SIEL only and are subject to change. They should not be construed as investment advice.

This information is issued by SEI Investments (Europe) Limited (“SIEL”) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority (FRN 191713).

SEI sources data directly from FactSet, Lipper, and BlackRock unless otherwise stated.

Important Notes

The SEI Funds may not be offered or sold to the public in Argentina, Brazil, Chile, Colombia, Mexico, Peru, Venezuela or any other country in Central or South America. Accordingly, the offering of shares of the SEI Funds has not been submitted for approval in these jurisdictions. Documents relating to the SEI Funds (as well as information contained herein) may not be supplied to the general public for purposes of a public offering in the above jurisdictions or be used in connection with any offer or subscription for sale to the public in such jurisdictions.