US Value Stocks: No. It’s not “different this time.”

Every time a group of stocks delivers sustained outperformance, there’s a tendency to want to believe that the world has changed forever and that “it’s different this time.” We saw this during the tech bubble from 1998-2000 and during the 1960s and 1970s with the “Nifty Fifty1,” to name just a few of the many examples throughout history. The tech bubble implosion in 2000 and the bear market of 1973-74 both demonstrated that the world had not changed. Today, the spectacular rise in growth stocks that began in 2009—and which has accelerated since 2017—has led some investors to believe that growth stocks will rise forever and that value stocks will never recover. We don’t believe it.

We believe in reversion to the mean

“Reversion to the mean” is a fancy investment phrase used to explain the idea that stock prices and returns will eventually return to their historical averages. Low prices won’t stay low forever. High prices won’t stay high forever. Looking at the spread between growth and value, we can’t help but think of reversion to the mean.

Relative to growth, value has performed so poorly over the past decade that only about 5 percent of previous ten-year periods have been worse. Yet, even with the past decade of significant underperformance, value has outperformed growth—on average—over all rolling 10-year periods over the last 30 years, which is why we maintain exposure to value stocks as part of our portfolio construction process.

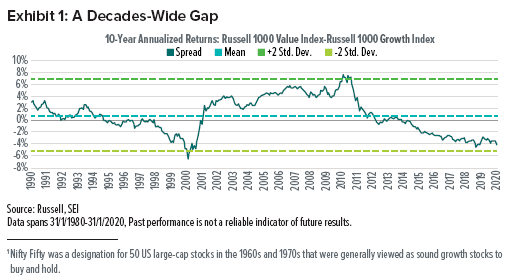

We continue to believe the current performance gap between value and growth represents what may be the most attractive investment environment for value stocks that we have seen in nearly 20 years, as seen in Exhibit 1.

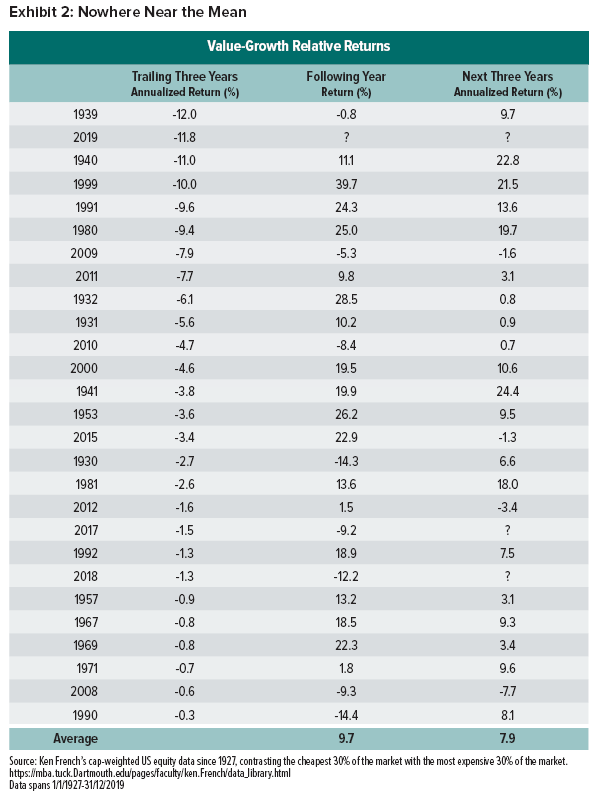

Periods in which value underperforms have historically been followed by outperformance. Value has rebounded and outperformed growth over the following three years in more than 80% of these scenarios since 1927, as Exhibit 2 highlights.

When Will Value Shine?

To the great disappointment of anxious value investors, there’s no easy answer to this question. Looking at historical data does not give us a clear answer. Looking back to the 1980s, the US started the decade in a high interest-rate environment with corresponding high rates of inflation. For much of the 1980s, 1990s and 2000s, inflation declined until it stabilised right around the Fed’s target of 2%2. In conjunction, interest rates (especially long-term rates) generally fell as well. Since the global financial crisis, interest rates and inflation have generally settled at historically low levels.

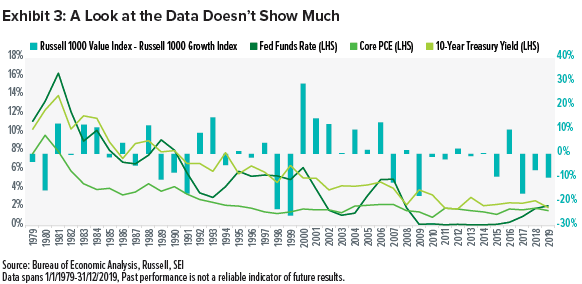

Exhibit 3 shows that the relative performance of value versus growth does not seem to be highly correlated to the environment for rates or inflation. We note, however, that value’s performance has seemingly been worse during the recent periods of historically low rates, yet we offered 2016 as an example of a time period with low rates and value outperformance.

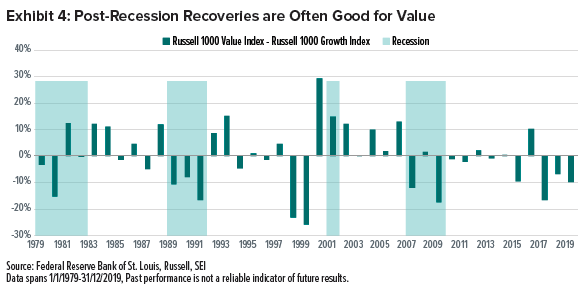

While the fundamental dispersions between growth and value are wide and the mispricing of stocks on either end (too optimistic or pessimistic) should be good for value, it is important to keep in mind that US markets are not in the “too pessimistic” scenario associated with bear markets and recession. Notably, as seen in Exhibit 4,the aftermath of recessions has often been a favourable period for value stocksversus growth stocks.

If US markets continue their current trends, growth stocks may not implode, they may simply slow to allow their earnings to catch up to the multiple, enabling value stocks to gain on a relative basis.

Our View: A Little Perspective Please

Yes. Growth has clearly beat value. Yet, value investors made money. Returns for value have been positive, with the Russell 1000 Value Index up 11.79% annualised (a more than 200% cumulative gain) over the 10-year period ending at 31 December 2019. And let’s not forget that US growth stocks have been the worldwide market leader. So value looks bad when compared to the absolute best-performing asset class in the world.

The performance of growth stocks has been dominated by the largest-capitalisation stocks, an environment that is typically challenging for active portfolio management.

Broadly speaking, active management as a whole, with its higher-volatility, smaller-cap and fundamental bias, is likely to experience an uptrend when larger-cap growth stocks eventually get recognised for the lack of upside in their valuations. Trees don’t grow to the sky.

As passively-managed strategies remain unable to alter their index-tracking mandates, actively-managed US equity strategies have the ability to seek greater exposure to high-quality companies as the market moves into an environment in which companies are valued based on their fundamentals.

This value versus growth comparison begs the question: “What is your goal?” If your goal as an investor is to generate positive returns, value has delivered. If your goal as an investor is to deliver solid risk-adjusted returns over the long term, value has done that. If your goal as in investor is to compare your portfolio to whatever the absolute best-performing investment has been over any given time period, you are probably in for a lifetime of disappointment regardless of what your portfolio holds.

Important Information

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.