The U.S. dollar’s demise: Old song, new music.

There’s been a good deal of digital ink spilled in recent weeks over the pending demise of the U.S dollar (USD). It makes for catchy headlines, but the underlying realities are complicated and likely to play out over a much longer period than the internet age can tolerate. As Bloomberg’s John Authers recently put it, “Any discussion along these lines swiftly gets into deep waters.” While SEI would not be surprised to see the dollar weaken in the near-to-intermediate term, the “dollar demise” thesis has more of a longterm, structural character.

A long and winding road

The dollar has been central to global trade, global finance and global monetary reserves since shortly after World War II, although the process started earlier in the 20th century. During World War I, the U.S. had become the largest national economy and a critically important creditor for Allied governments. Not long after, New York City supplanted London as the global economy’s

financial center.1 Following World War II, much of the global economy transitioned to a monetary system of fixed exchange rates. The U.S. dollar (USD) was at its center, with the dollar convertible to gold at $35 per ounce.2 The system began to struggle in the late 1960s, as domestic spending priorities in the U.S. started to run ahead of what existing gold reserves were able to support. In 1971, the system essentially came to an end when President Nixon suspended gold convertibility. In 1973, it formally came to an end as six European countries created a currency bloc with a floating exchange rate against the USD. It took some time (see 1985’s Plaza Accord and 1987’s Louvre Accord), but the world eventually adjusted to the prevailing system of floating exchange rates and currencies that are not convertible into one or more precious metals. Despite these and other major upheavals (such as the global financial crisis), the central importance of the USD has persisted, supported by a large and dynamic U.S. economy, a relatively stable political system and trustworthy legal institutions. Many analysts would throw American military might (an outgrowth of the post-WWII Cold War between the U.S. and U.S.S.R.) into the equation as well. Whatever the reasons, it’s undeniable that the USD remains the central currency in terms of international trade, global financial transactions and foreign exchange reserves.

Movin’ on?

Recent events have some wondering how much longer the dollar’s centrality can last. These include high-profile musings about over reliance on the U.S. and the USD (France’s President Macron3), the desirability of replacing USD trade finance with a BRICS4 currency or exchange system (Brazilian President Lula de Silva5), creation of more financial exchanges and market quote systems independent of the USD (China’s offer to trade energy commodities in its currency, creating a petro yuan to challenge the petrodollar’s dominance6), and so on.

These frustrations are by no means new. The difficulty of relying on a national currency for the vast majority of cross-border transactions was anticipated at the Bretton Woods Conference in 1944, where British economist John Maynard Keynes proposed an innovation he called the bancor designed to facilitate multilateral clearing and prevent the buildup of significant trade and financial imbalances (it was voted down in favor of the dollar).7 In the 1960s, French President Charles de Gaulle voiced his displeasure with the U.S. dollar’s role and what his finance minister referred to as America’s “exorbitant privilege” of being the global reserve currency’s issuer.

In the 1980s, G5 and G6 countries had to coordinate measures to weaken and strengthen the USD via the Plaza and Louvre Accords, respectively. In 1999, after a decade of work, the euro currency came into existence and was immediately seen by many as a potential rival to USD hegemony. More recently, the growing importance of China’s economy has seen its currency become a larger part of global monetary reserves. Current Congressional drama over the federal debt ceiling is a spectacle that we’ve been treated to several times this century. In other words, the demise-of-the-dollar song is an old one—we’re just hearing the 2023 remix.

The latest remix does contain some novel features. One is “weaponization” of the dollar, a term referring to aggressive actions taken by the U.S. government and its allies towards sanctioned state and non-state actors outside of formal criminal proceedings, including freezing or seizing USD assets and cutting off access to important areas of the global financial and trading systems. These measures have been particularly intense since Russia’s invasion of Ukraine, and it’s reasonable to think that they have motivated some countries to more urgently consider ways to circumvent dollar dominance (and, unsurprisingly, to try to amplify the dollar-demise narrative). To the extent this contributes to balkanization of the global payments system and capital markets, it could serve to undermine global trade and finance, a dynamic that could keep higher inflation in play. Second is U.S. fiscal profligacy which has been on full display since the onset of COVID-19. While this concern has certainly cropped up from time to time in decades past, current federal debt levels are much higher as a percentage of the U.S. economy this time around. Third is interest in returning to a system based around gold. This has been a small-but-steady drumbeat ever since President Nixon closed the U.S. Treasury’s gold window, but it’s getting more attention as a result of record central bank bullion purchases in 2022, led by the People’s Bank of China. Finally, and perhaps most importantly, are China’s geostrategic ambitions which could include a more important role for the Chinese yuan. The challenges are significant—China would have to undertake liberalization of its financial system, for example, and let its currency float freely—but we should be careful not to underestimate China’s ambitions in our increasingly multipolar world. Something will certainly upend the world’s USD-centric arrangements at some point. After all, history teaches us that change is inevitable. When that might occur and what it looks like are still wildly indeterminate. All of that noted, there remain serious hurdles to any potential alternatives displacing the USD in the near-to-intermediate term.

What’s it all mean?

The implications and outcomes of a shift away from dollar hegemony are too numerous (as well as uncertain) to list. Even if the process is underway, such an event would take a long period of time to play out. We believe investors would be well served by not reading too much into the normal variations in USD levels as signs of its ultimate demise from the world’s reserve currency. With that in mind, near term view is for USD weakness given softening U.S. economic data and the potential that the U.S. Federal Reserve is closer to the end of its tightening cycle relative to other central banks. This view on the USD has implications outside of the foreign exchange markets as well. For U.S.-based investors (and anyone else whose base currency is the USD), a weaker dollar can boost returns on non-USD denominated holdings that are not currency hedged, all else being equal. For non-U.S. investors (and anyone whose base currency is something other than USD), a weaker dollar could mean lower returns on unhedged, USD-denominated investments, all else being equal. While we see no immediate concerns related to the dollar’s status, we will continue to monitor developments and consider their implications for short-term opportunities in portfolios that offer dynamic capabilities and for long-term asset allocation decisions.

Glossary

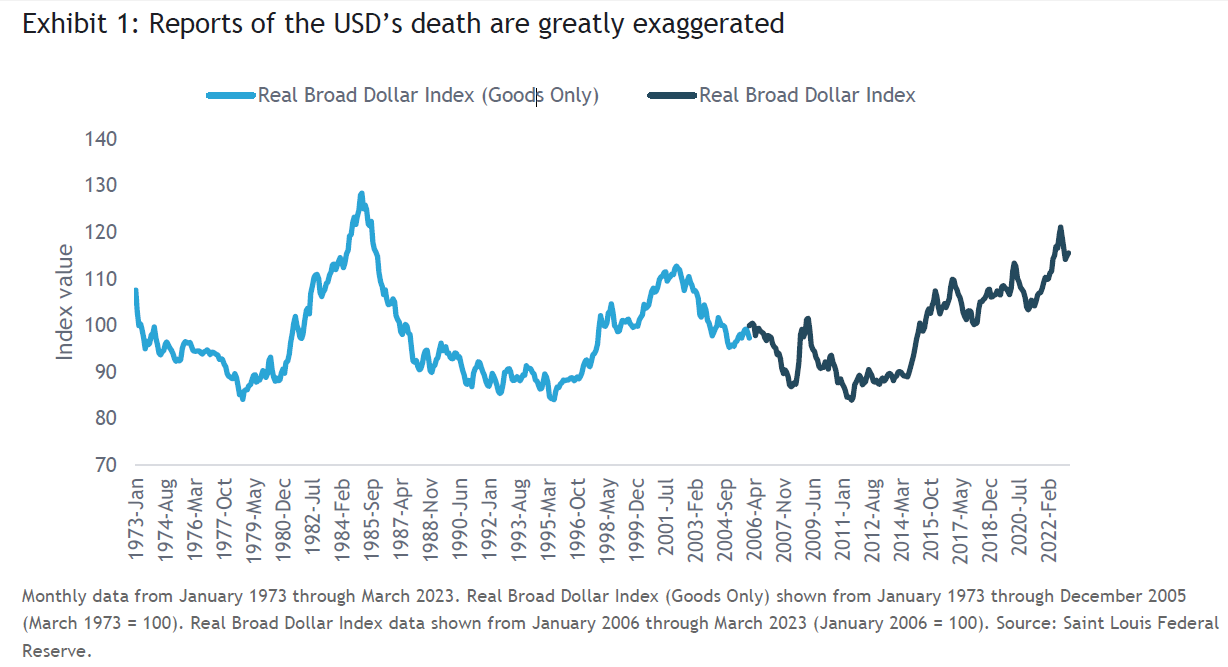

Real Broad Dollar Index: A weighted average of the foreign exchange value of the U.S. dollar against the currencies of a broad group of major U.S. trading partners. The ‘Goods Only’ methodology was discontinued in 2019. The newer methodology, which includes services trading, was introduced in 2006.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High-yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This information is being made available in Hong Kong by SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This email and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.