UK property market: Outlook 2022-2026

The Bank of England cautions that an unusually long recession may already be underway. In this environment, we believe the UK property market will generate weak performance for 2023 before rebounding in 2024 and beyond.

Rising rates, high inflation, weak currency=weak property market

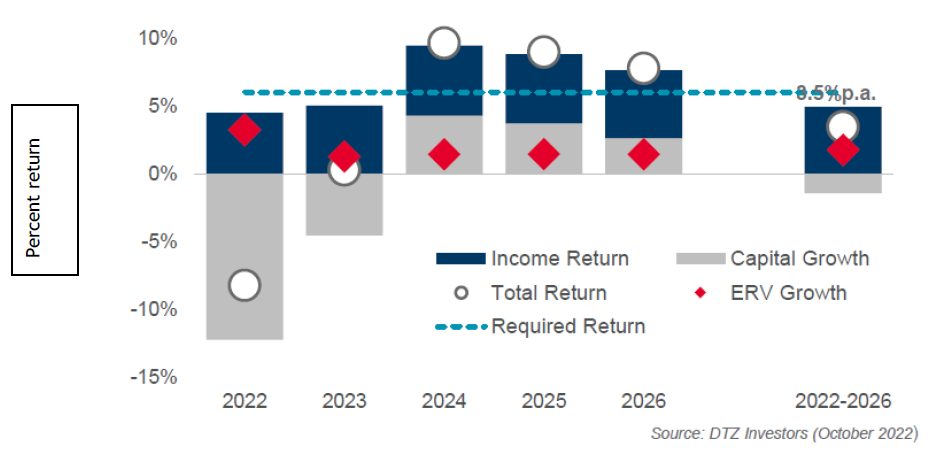

The UK economy has been posting troubling economic warning signs. Historically high inflation, a weakening pound relative to the dollar, and strong wage growth led the Bank of England’s Monetary Policy Committee (MPC) to raise rates interest rates by 50 basis points in September and then another 75 a little over a month later (its largest rate hike in over 30 years as shown by www.bankofengland.co.uk/boeapps/database/Bank-Rate.asp). While these moves may be have been necessary to combat inflation, they put increased pressure on an already struggling economy. As the country’s broader economy faces the prospect of a prolonged recession lasting through 2023, we believe that the UK property market will fare similarly. We expect the UK property market to deliver weak returns through the end of 2023. As economic conditions improve in 2024 and beyond the property market should rebound for the remainder of the forecast period (2024-2026).

“Very challenging” economic conditions hit real estate prices

In early November, the Bank of England warned that the UK was on the brink of a recession that could potentially extend into 2024. Facing an economic downturn that could be the nation’s longest on record, the central bank described the outlook as “very challenging”. Meanwhile, increasing fuel and food prices pushed the annual rate of Consumer Price Index inflation to multiple 40-year highs on multiple occasions in 2022 as per the Office for National Statistics. It is within the context of these extreme and adverse market conditions that we believe that the UK property market is experiencing a broad repricing and we believe the aforementioned recession and inflation will likely cause weak performance through 2023. Estimated rental value growth (ERV) is projected to remain low through 2026.

All property direct market return forecasts (2022-2026)

Data refers to predicted future performance. Predicted future performance is no guarantee of future results. Investment may lead to a financial loss if no guarantee on the capital is in place.

The challenges to the property market

The UK economy contracted in the third quarter of 2022 based on estimates from the Bank of England. While policymakers raised rates to combat persistent inflation, this had an adverse impact on the real estate investment market. Higher rates can translate into higher costs for borrowers, pushing purchases further out of reach for potential home buyers. In relative terms, an increase in bond yields can also make real estate investments less attractive; why lock up one’s capital in an illiquid property when a more liquid vehicle offers a competitive return? Furthermore, the persistent rises in inflation serve to push up operational costs, potentially reducing the profit margins for real estate investments. Finally, a combination of higher cost of living and low consumer confidence has the potential to drag consumer-led property segments lower.

Bright spots

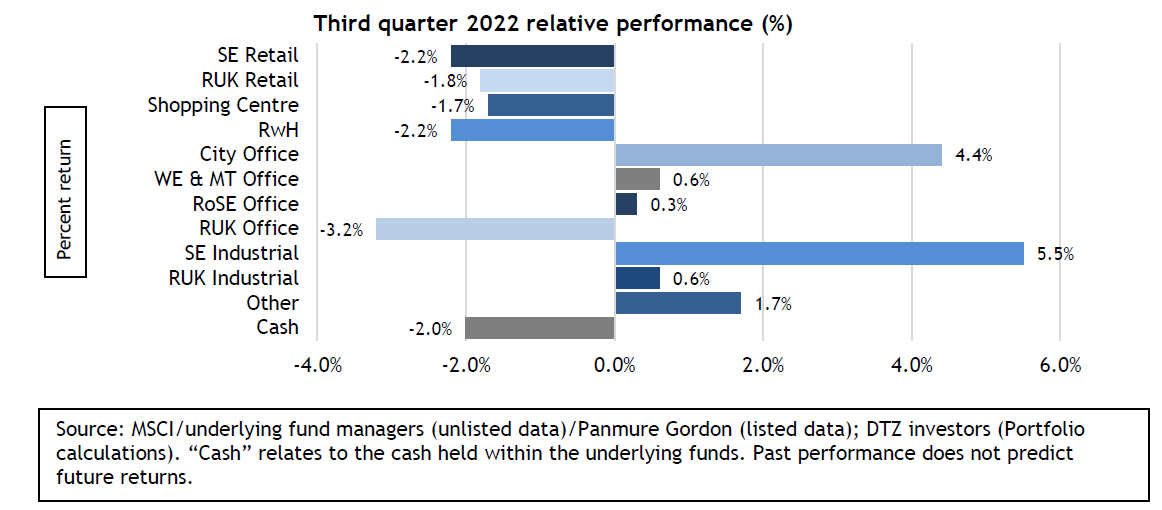

While we expect poor performance for the broad UK property market in the short term, not all segments of the market are created equal. Retail, for example, was down in the third quarter, as the first three bars in Exhibit 1 show. Retail warehouse was as well, as highlighted by the fourth bar. Office space was mixed. Industrial properties were positive to varying degrees. On the bright side, we believe that alternative real estate segments (ex. student housing) have the potential to behave differently than the rest of the market, with positive near-term prospects for rent growth and returns. Conversely, we expect to see a sharp near-term reversal in the industrial sector, which had outperformed in the second quarter. We don’t expect this trend to be long lived however, believing that positive supply/demand metrics and limited development activity in this segment should lead to a quicker recovery than in others in 2023.

Exhibit 1: Not all market segments move in lockstep

Our Fund

The SEI UK Property Fund remains overweight to South East Industrial. The supply/demand dynamics in this market remain favorable, and looking beyond the near-term capital market re-pricing, the prospects for rental growth look positive.

We anticipate a reduction in the long position in City offices, as the sector has a negative outlook given the long- term headwinds.

The portfolio’s overweight exposure to alternative real estate segments, categorized by MSCI as “Other”, is considered favorable in the current market context because these segments have strong fundamentals that are less tied to UK gross domestic product and are likely to prove more resilient in the near-term. Values are expected to hold up relatively well in the residential, student housing and healthcare segments where the portfolio is overweight. The overweight to real estate debt should also be helpful.

Important Information

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

The UK Property Fund is an Irish Common Contractual Fund (“Irish CCFs”) which is authorised by the Central Bank of Ireland pursuant to the Investment Funds, Companies and Miscellaneous Provisions Act 2005 and the European Union (Alternative Investment Funds Managers)

Regulations (as amended) (the “AIFM Regulations”). The Irish CCFs are managed by SEI Investments Global, Limited an Irish private limited liability company which is authorized by the CBI pursuant to the AIFM Regulations. The Irish CCFs are subject to the Central Bank of Ireland’s regulatory regime for alternative investment funds contained in the AIF Rulebook and qualify as qualifying investors scheme for the purpose of the AIF Rulebook. As such, the Irish CCFs may be marketed solely to Qualifying Investors. SEI Investments (Europe) Ltd acts as the distributor of the Irish CCFs.

SEI Alternative Investment Funds may be non-standardised and bespoke, and may invest in a variety of underlying assets such as shares in unregulated collective investment schemes which do not provide a level of investor protection equivalent to collective investment schemes, debt securities including collateralized loan instruments, asset backed securities and other forms of structured credit, property, commodities or fund-of funds. Alternative Investment Funds by their nature involve a substantial degree of risk, including limited liquidity, lack of regulatory oversight, tax risks, investment risks, risks inherent to investments in highly volatile markets, risks related to international investment, risks pertaining to various investment techniques that may be employed by the fund, risks related to the ability to diversify investments, risks related to the accuracy of valuations of investments, and conflicts of interest and the risk of complete loss of capital and are only appropriate for parties who can bear that high degree of risk and the highly illiquid nature of an investment.

SEI Alternative Investment Funds often engage in leveraging and other speculative investment practices that may increase the risk of investment loss. It should be noted that they may not be required to provide periodic pricing or valuation information to investors and may involve complex tax structures and delays in distributing important tax information, are not subject to the same regulatory requirements as SEI’s range of UCITS and may often charge higher fees and offer limited liquidity.

The SEI UK Property Fund invests in unregulated collective investment schemes which may not be subject to the same legal and regulatory protection as afforded by collective investment schemes authorised and regulated in the European Union or equivalent jurisdictions. Investment in unregulated schemes involves special risks that could lead to a loss of all or a substantial portion of such investment. Due to the nature of property investment, and in particular the potential delays connected with the sale or realisation of investments in the property market, investment properties may not be readily realisable from time to time which may give rise to a delay in giving effect to redemptions.

This information is issued by SEI Investments (Europe) Limited (“SIEL”) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. This document and its contents are directed only at persons who have been categorised by SIEL as a Professional Client, for the purposes of the FCA Conduct of Business Sourcebook. SIEL is authorised and regulated by the Financial Conduct Authority.

Past performance does not predict future returns. Investments in SEI Funds are generally medium to long term investments. The value of an investment and any income from it can go down as well as up. Fluctuations or movements in exchange rates may cause the value of underlying international investments to go up or down. Investors may not get back the original amount invested. SEI Funds may use derivative instruments which may be used for hedging purposes and/or investment purposes. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events.

Any reference in this document to any SEI Funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application must be made solely on the basis of the information contained in the Prospectus (which includes a schedule of fees and charges and maximum commission available). Commissions and incentives may be paid and if so, would be included in the overall costs. A copy of the Prospectus can be obtained by contacting your Financial Advisor, SEI Relationship Manager or by using the contact details shown above.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Singapore

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

Hong Kong

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

South Africa Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.