UK General Election: Markets Expect Status Quo

The clouds of uncertainty hanging over business investment, consumer confidence and the broader UK economy may begin to clear in the aftermath of the 12 December election. A prolonged state of high anxiety has restrained UK investment performance over the last three-plus years despite a strong labour market and gains in wages1.

At a high level, electoral patterns that have emerged in different corners of the developed world over recent years are also influencing expectations for the December vote. These trends are reflected in the re-alignment of political preferences in the UK and a growing divide between the country’s rural and urban communities and among voters of different education levels, for example2.

Forecast for Reign

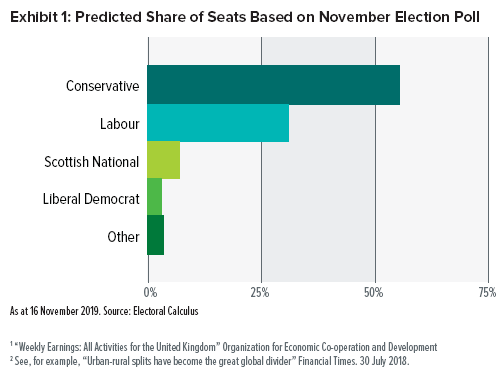

Recent polling indicates that Conservatives will likely win a comfortable parliamentary majority (Exhibit 1). There are still several weeks to go before the election, and the post-election landscape presents its own challenges regardless of the outcome. Nevertheless, we think the most probable scenario is an outright Tory win, followed by an affirmative vote in Parliament for the current Government’s deal and then an orderly Brexit.

But it’s still possible, albeit unlikely, that a coalition (perhaps comprising the Labour, Liberal Democrat and Scottish National Parties) could cobble together a majority that delays the UK’s departure from the EU. If so, it could lead to a second referendum that might result in a “soft” Brexit (wherein the UK remains in the EU’s single market and the customs union) or even a “remain” outcome (calling off the divorce altogether). A third possible Brexit outcome—a disorderly “no deal” departure—could come about under multiple election results; although this appears to be the least likely outcome at this time.

Our odds of a given post-election Brexit-related outcome are approximately as follows:

- 50%—Orderly Brexit per Johnson’s deal (functional Conservative majority)

- 10%—No Deal Departure

- 20%—Delayed Departure (followed by a second referendum)

- 20%—Remain

The End of the Beginning

These improving prospects for a resolution to the multi-year Brexit struggle offer hope. Yet regardless of which resolution comes to pass, nothing will necessarily change on the 31 January 2020 stated departure date. The UK and EU agreed to a transition period that extends to the end of 2020 to provide time for negotiating the terms of their future relationship. This means businesses will still be dealing with a great deal of economic uncertainty—and may therefore remain reluctant to make major investments.

Furthermore, the prospect of a No Deal departure still exists if the transition period ends without a deal to govern the ongoing UK-EU relationship. This would force trade between the UK and EU to take place under the rules set forth by the World Trade Organisation. The UK will also no longer be a party to the EU’s international trade agreements.

Market prices have nevertheless reflected optimism over the last few weeks, as both the EU and Parliament finally rendered the Government’s Brexit deal acceptable upon its major concession on the Irish backstop (although it was ultimately doomed by the timetable). The persistence of a stronger pound and UK equities in recent weeks suggests expectations for a status-quo election outcome.

While the Government’s backstop concession undoubtedly angered hardline Brexit proponents, most of them probably considered it better than a hung Parliament or Labour win at the polls. Indeed, if the odds of a Labour Party majority increase, we would anticipate a negative impact on sterling, equity and gilt markets. Ideology aside, higher taxes, nationalisation and an antagonistic foreign policy toward the US—a major ally and trading partner—may drastically increase uncertainty for business and investors.

We expect that a functional Conservative majority and a successfully-negotiated departure would each bolster sterling alongside higher interest rates.

SEI’s View

We find it interesting that both major parties in the UK are striving to out-promise each other on fiscal spending. This easing of restraints should be welcomed given the likelihood that uncertainty will linger for at least another year. More government spending would be a net positive in the near term.

The Bank of England’s monetary policy will probably remain on hold for the next six months as post-election Brexit policy takes shape. It’s stuck between opposing priorities given elevated UK inflation (which would normally necessitate higher interest rates) and sagging business investment (which would normally necessitate lower interest rates). A looser fiscal budget would be expected to shift this calculus by further stoking inflation and, presumably, by boosting business prospects.

It’s possible that the UK’s near-universal embrace of government spending could have implications on the Continent. The German economy has been weakening in recent quarters, and an expansive fiscal policy in the UK could set a new precedent for the region. Germany can afford to loosen its traditionally prudent approach to fiscal management and allow an expansionary government spending policy to help offset its economic sluggishness. This would be good for Europe broadly and corporate earnings as well—while enabling the Germans to remain the most prudent economic policymakers in Europe, since the UK appears to be leading the way.

Important Information

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information. Data refers to past performance. Past performance is not a reliable indicator of future results.

The opinions and views in this commentary are of SIEL only and are subject to change. They should not be construed as investment advice. This information is issued by SEI Investments (Europe) Limited (“SIEL”) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority (FRN 191713).