Trump’s trade war: Not tariff-ic.

The possible imposition of tariffs on Canada and Mexico and the actual implementation of a 10% across-the-board tariff on China have the potential to increase prices and lower economic growth. The precise impact is still unclear since we do not know how aggressive the tariffs will be or how long they will stay in place. We do know that tariffs on goods from Colombia were short-lived and that this president loves to make deals.

Tariffs imposed on Mexico, Canada, and China

It almost looked as if that guacamole dip and the tequila for those margaritas on Super Bowl Sunday were about to get more expensive for U.S. consumers after President Trump announced his intention to impose a 25% across-the-board tariff on Mexico beginning February 4. However, the day before the tariffs were to become effective, the implementation was delayed for a month after Mexico agreed to send 10,000 troops to the border to combat the flow of fentanyl into the U.S. A few hours later, Canada also gained a one-month reprieve from a planned 25% tariff (with an exception for energy, which faced a 10% duty). Meanwhile, China has been hit with a 10% tariff, but might be rescinded or altered pending negotiations.

While investors, businesses, and consumers are breathing a collective sigh of relief, President Trump’s plans regarding future tariffs remain a great unknown. We may see more product-specific duties on semiconductors, steel, aluminum, pharmaceuticals, and other items by mid-February. Until now, markets had taken all the tariff talk pretty much in stride, perhaps on the assumption that Trump’s threats were more negotiating bluster than a serious policy. Even with the reprieve, investors face a new and uncomfortable reality.

Why?

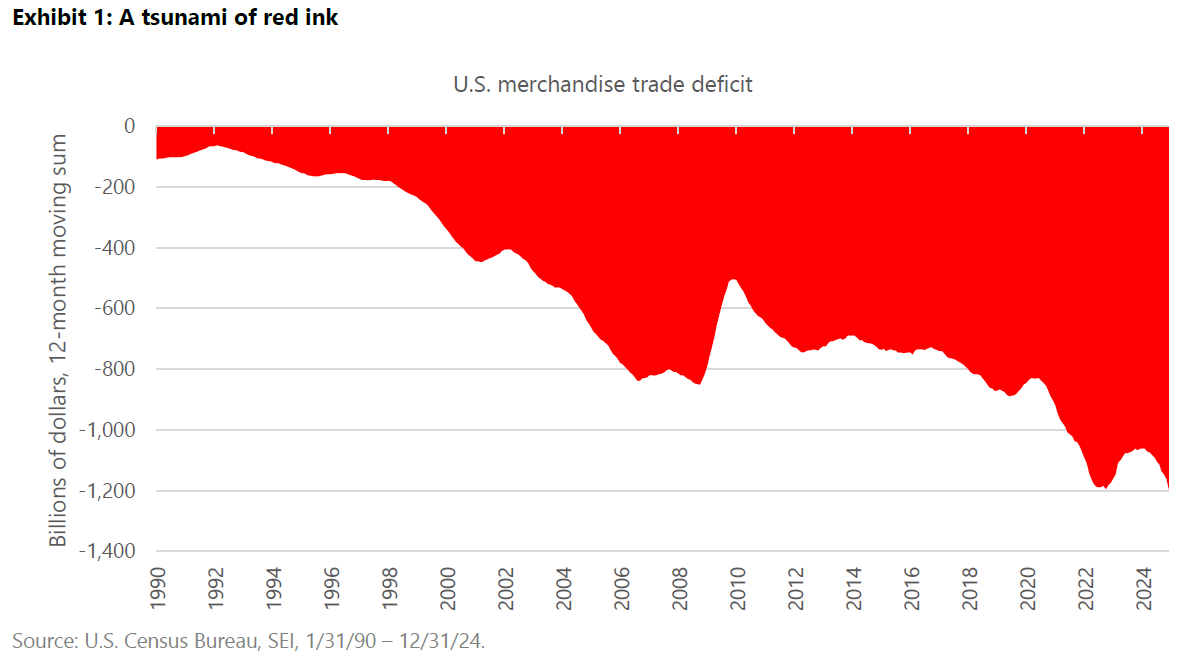

First, it is well known that Donald Trump for decades has been incensed over the U.S. trade deficit. As shown in Exhibit 1, the merchandise trade balance has been widening for the past three decades, well before the emergence of China as an exporting powerhouse after it joined the World Trade Organization (WTO) in December 2001. There are many reasons for this deterioration in the U.S. trade balance, including:

- A heavily consumption-focused economy

- The impact of globalization and the hollowing out of U.S. manufacturing capabilities

- A national savings rate that is well below the rate of investment (requiring massive capital inflows that are the mirror image of the current account deficit)

- Disparities in tariff and non-tariff barriers that disadvantage U.S. exports, especially for agricultural commodities

What’s next?

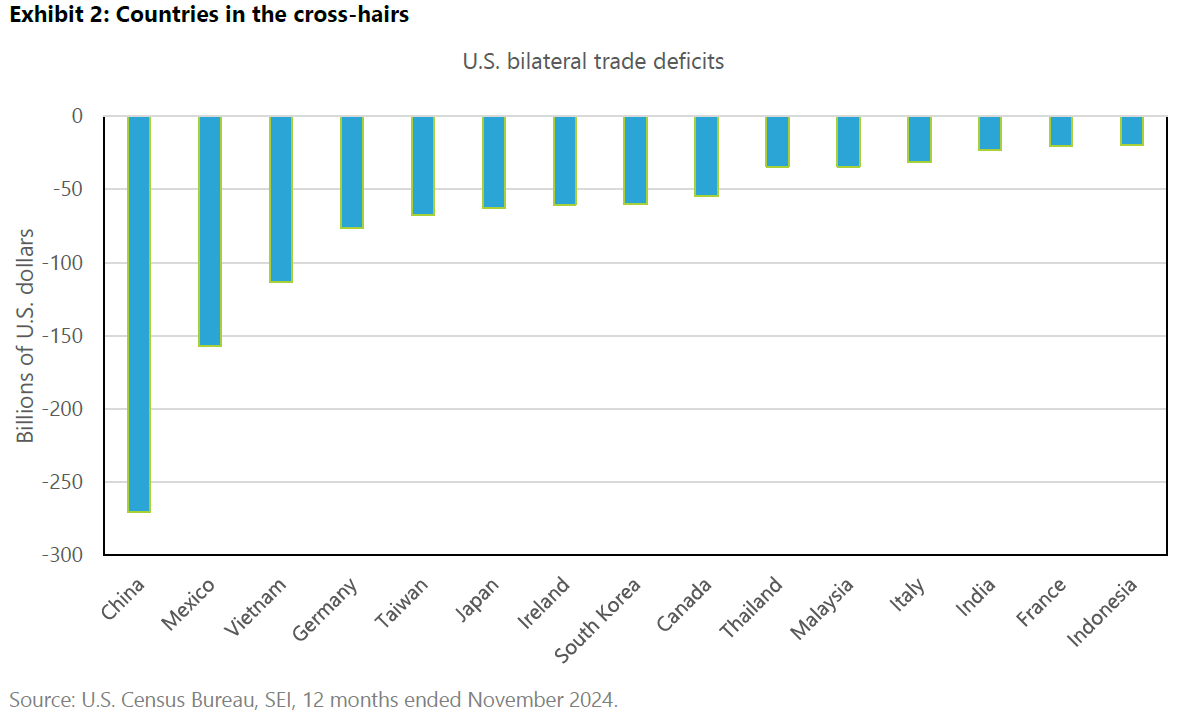

Trump believes trade deficits are bad for the country, and he has consistently viewed tariffs as the best way to level the playing field. Exhibit 2 highlights the countries in Trump’s direct line of fire. Obviously, China tops the list, followed by Mexico and Vietnam. It is a bit surprising that Trump’s initial tariffs would have been harsher towards Mexico and Canada than towards China. Of course, there are other considerations involved.

Sticking points

Trump is pressing both countries to reduce illegal border crossings and the flow of fentanyl and other drugs. Illegal crossings, especially from the southern border, were already declining after former President Biden signed an executive order back in June. Enforcement has been tightened further since Trump’s inauguration. Although official data have not yet been released, illegal crossings are indisputably much lower than they were in the 2021-to-2024 period when they averaged nearly 5,500 per day1. In addition, the United States-Mexico-Canada Agreement (USMCA) free-trade deal that went into effect July 1, 2020, is up for review in July 2026. Trump wants to reopen the negotiations now. He appears especially interested in forcing vehicle and parts manufacturing back inside the U.S. and eliminating China’s foothold in Mexico.

Mexico and Canada have taken different approaches when dealing with Trump. Mexico’s new president, Claudia Sheinbaum, has taken a more conciliatory tack. The country will abide by Trump’s “remain in Mexico” policy, is willing to collaborate and coordinate with the U.S. in the fight against the drug cartels, and has announced incentives to encourage the production of goods with local content aimed at reducing its dependence on Chinese imports. The approach has paid off—at least in the near term. Canada’s rhetoric has been more defiant, although it, too, has agreed to ramp up its monitoring of the border. The postponement of tariff implementation buys time but probably does not improve Canada’s negotiating leverage.

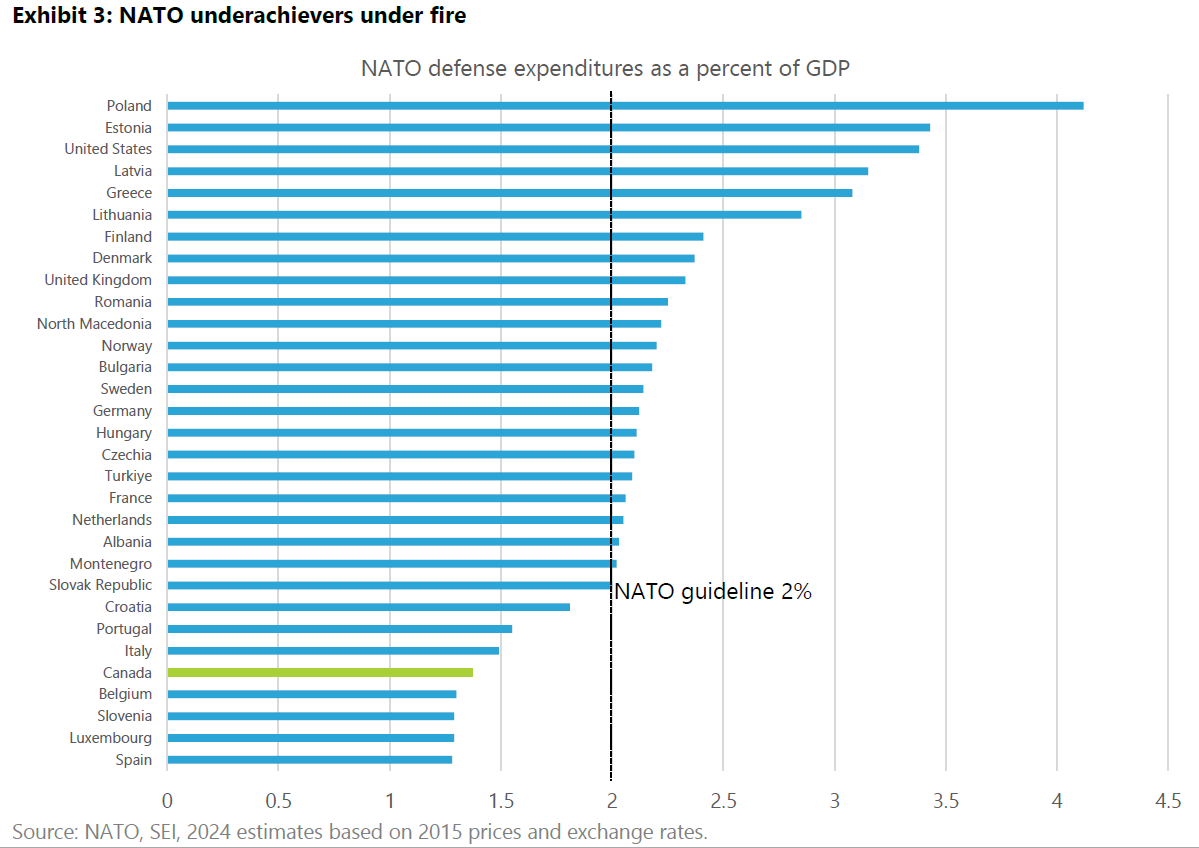

Although the border and the renegotiation of the USMCA is currently front-and-center, Canada may face additional flak from the Trump administration owing to its low military expenditures as a member of the North Atlantic Treaty Organization (NATO) alliance. Exhibit 3 highlights defense spending as a percent of gross domestic product (GDP) for each NATO member versus the 2% guideline that was established in 2006. Although most members are finally in alignment with the guideline, Canada remains near the bottom of the pack, spending just 1.4% of GDP.

1 Interim Staff Report of the Committee on the Judiciary and Subcommittee on Immigration Integrity, Security, and Enforcement U.S. House of Representatives

In his first term, President Trump threatened to pull out of the alliance if other members failed to meet the guideline. His threats, and Russia’s invasion of Ukraine, galvanized several NATO countries to ramp up their defense spending in recent years. However, Canada, Italy, and Spain, among a few others, are still not pulling their weight. Perhaps this time around, Trump will threaten the laggards with punitive tariffs instead.

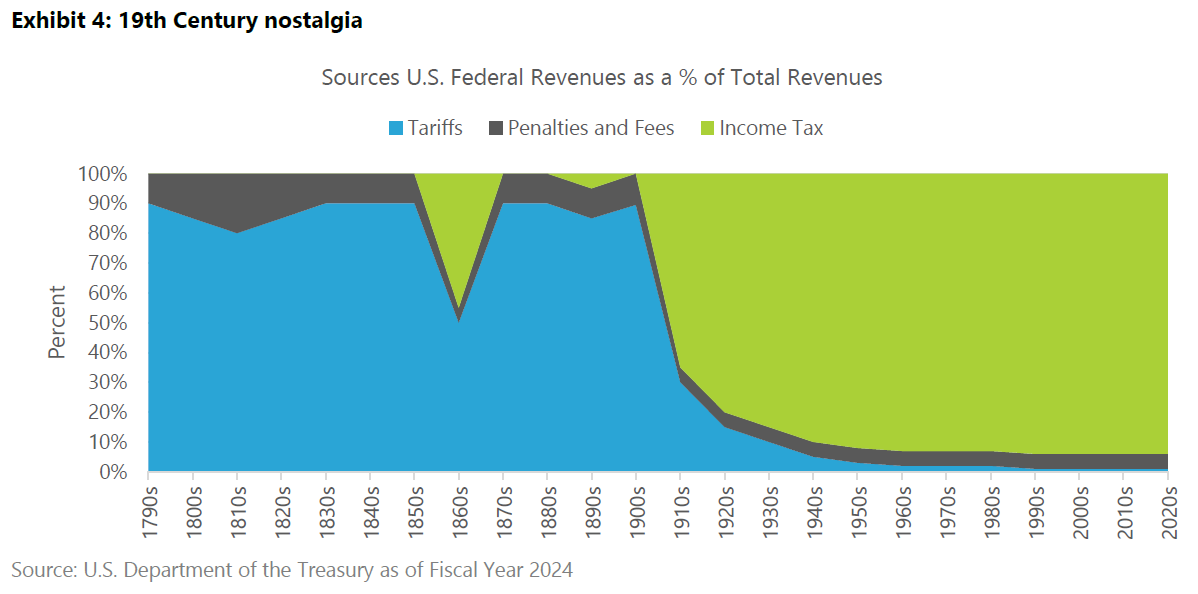

Up to this point, the discussion has been centered on tariffs as a tool to wrest concessions from specific countries. There is also a good chance that an across-the-board tariff will be imposed on every country. Trump has been voicing his admiration for William McKinley, the 25th president of the U.S. from 1897 until his assassination in 1901. He refers to McKinley as the original “tariff man.” As shown in Exhibit 4, until the early 1900s, the U.S. had no income tax. The vast bulk of the federal government’s revenues were derived from tariffs. An income tax was introduced during the Civil War, but was repealed in 1872. A permanent income tax was not established until the passage of the 16th Amendment to the Constitution in 1913.

Of course, there is no going back to a time when tariffs comprised 90% of federal revenues and the federal government itself was a much smaller part of the overall economy. However, Trump may want to impose an across-the-board tariff to pay for a corporate tax rate reduction or additional individual income tax-rate cuts. If he wants to fold tariff revenues into a reconciliation bill that sets overall tax and spending levels for the next 10 years, the president will need the approval of Congress. Treasury Secretary Scott Bessent is reportedly pushing for a 2.5% universal tariff, but Trump has consistently called for a blanket tariff of 10% or more.

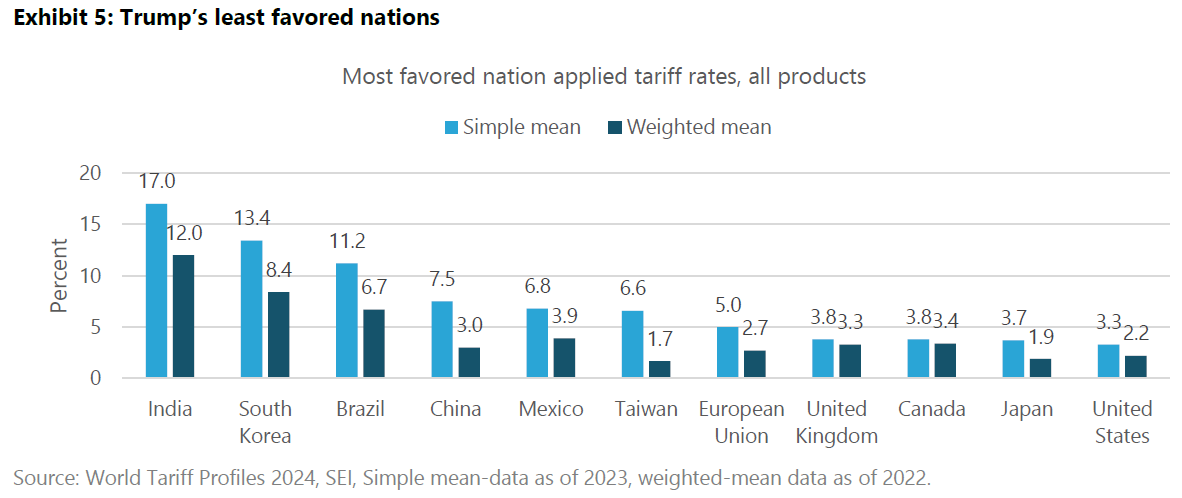

Exhibit 5 highlights the average tariff rates of the largest trading partners with the U.S. Note that the U.S. has some of the lowest tariff rates among this group. However, according to the WTO, the U.S. is exposed to an applied weighted tariff in its major export markets of 1.7% (9.8% for agricultural products versus 0.8% for non-agricultural products). A move to impose a high across-the-board tariff would almost certainly elicit retaliation, hurting U.S. exporters that are already at a competitive disadvantage from the strong dollar. The U.S. government might get more tariff revenue but would likely lose revenues from income taxes if economic growth were to slow. Virtually all exports to Canada and Mexico are now duty-free owing to the USMCA, for example. A tit-for-tat trade war would end that arrangement.

Economic implications

A tariff war obviously will not be without cost; it has the potential of increasing prices and slowing economic growth. The precise impact is unclear, since we do not know how aggressive the tariffs will be, how long they will stay in place, and whether they will extend to all, most, or some countries and products. In addition, the impact on prices, growth, and earnings will depend on the demand for the products subject to tariffs.

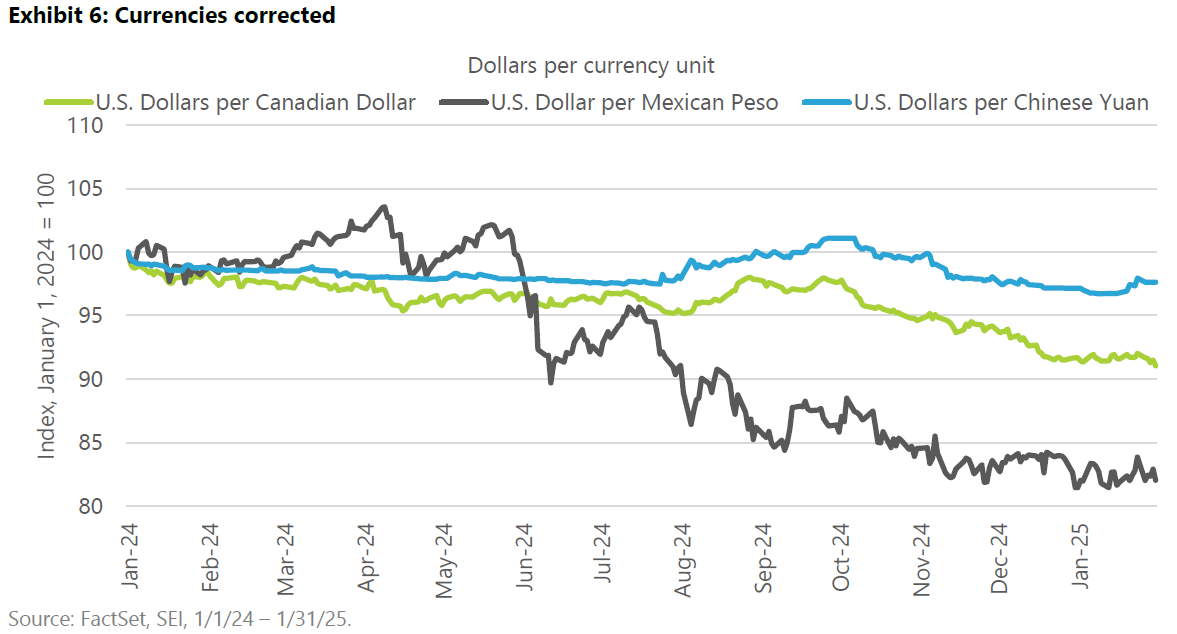

The impact could also be softened by a depreciation of foreign currencies versus the U.S. dollar. Exhibit 6 shows that the Canadian dollar, the Mexican peso, and the Chinese yuan have all declined against the dollar since the beginning of 2024. The Mexican peso has already plunged 18% over the past 13 months, while the Canadian dollar has depreciated 9%. These declines will substantially reduce the pain associated with the tariff increases on profit margins, but both countries will still be hurt by declining U.S. demand for their products and the severe disruption to supply chains for automakers and other major manufacturers.

It is important to remember that the details of the tariffs could change at any time, as we have just seen. We would not be surprised if some accommodation is given to trade in autos and motor vehicle parts, for example. Even if Trump is determined to bring back more car manufacturing to the U.S., it cannot happen overnight. To say the least, U.S. trade policy will be highlighted by many twists and turns in the months ahead.

Looking ahead:

- The economies of Mexico and Canada could dip into a moderate recession in the months ahead given their high dependence on the U.S. market if tariffs are imposed and held indefinitely at high rates.

- The U.S. could sustain a sharp deceleration of growth and may even experience a pullback in industrial output given the extent of economic integration with its two major trading partners.

- A broadening of the trade war to include Europe and Asia would further depress economic growth, but on a global scale.

- In the near term, supply-chain disruptions and retaliatory actions could increase U.S. inflation beyond 3%.

- Monetary policy across the developed world was already diverging, with interest rates falling more rapidly in Canada and the eurozone than in the U.S. An expanding trade war would exacerbate this trend.

- Monetary policy divergence also implies a further strengthening of the U.S. dollar.

There are no winners in a trade war. The initial reaction of markets has been predictable, with equities sliding and the U.S. dollar rising until Trump delayed the start date of the tariff increases. Whether Trump makes a full retreat from this full-out assault on trade remains to be seen. The tariffs on Colombia came and went in a blink of an eye. His executive order freezing federal grants also was quickly withdrawn amid fierce blowback.

The notable asymmetry in trade relationships is another big consideration. Using figures from the Office of the U.S. Trade Representative, U.S. exports to Canada and Mexico are roughly 1.5% and 1.3% of U.S. GDP, respectively, while exports to the U.S. represent 28% of Mexico’s GDP and 22% of Canada’s GDP. In other words, there is motivation for Mexico and Canada to bring this to a quick resolution, and this president prides himself on his deal-making prowess.

In the short term:

- Trade uncertainty should remain a positive for the U.S. dollar. The previously cited imbalances, particularly if there are monetary policy responses, will continue to boost the U.S. dollar versus the Mexican peso, Canadian dollar, Chinese yuan, and the euro.

- Commodities will likely benefit given Canada’s substantial presence in the U.S. energy market, as well as Mexico’s role in supplying agricultural products.

- Not surprisingly, SEI expects volatility strategies to perform well. The Chicago Board Options Exchange (Cboe) Volatility Index (VIX), also known as the “fear index,” a measure of implied volatility in the S&P 500 Index, topped 20 on February 3, up about 15% in the session before falling back in response to the delay in tariff implementation. Higher volatility should remain a feature as the reactions and negotiations begin to play out.

- U.S. interest rates are a bit of a wildcard; they may benefit as investors move away from the volatility in the equity market. However, given the potential inflationary pressures and the tightening of financial conditions, we could see a resumption of yield-curve steepening as long-term rates track higher inflation, while short rates await further Federal Reserve guidance.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security, including futures contracts. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

Diversification does not ensure a profit or guarantee against a loss. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments and smaller companies typically exhibit higher volatility. Bonds and bond funds will decrease in value as interest rates rise. High-yield bonds involve greater risks of default or downgrade and are more volatile than investment-grade securities, due to the speculative nature of their investments.

Index returns are for illustrative purposes only and do not represent actual portfolio performance. Index returns do not reflect any management fees, transaction costs or expenses. One cannot invest directly in an index.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

SEI sources data directly from FactSet, Lipper, and BlackRock unless otherwise stated.

Information provided by SEI Investments Management Corporation, a wholly owned subsidiary of SEI Investments Company (SEI). They should not be construed as investment advice.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This document has not been registered by the Registrar of Companies in Hong Kong. In addition, this document may not be issued or possessed for the purposes of issue, whether in Hong Kong or elsewhere, and the Shares may not be disposed of to any person unless such person is outside Hong Kong, such person is a “professional investor” as defined in the Ordinance and any rules made under the Ordinance or as otherwise may be permitted by the Ordinance.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This document and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs, and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.