Trade Tweets: A Negotiating Tactic or a Catalyst for a Crash?

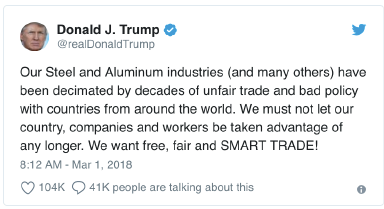

With that tweet on 1 March, 2018, at 7:12 a.m. ET, President Donald Trump launched a major effort to enact the trade policy that he promised on the campaign trail. Later that day, he convened corporate executives from the industrial metals industry at the White House to offer assurances that he would help shield their businesses and workers from foreign competition by imposing tariffs of 25% on steel and 10% on aluminium. The announcement ignited investor fears of a trade war and sent stocks sharply lower around the world.

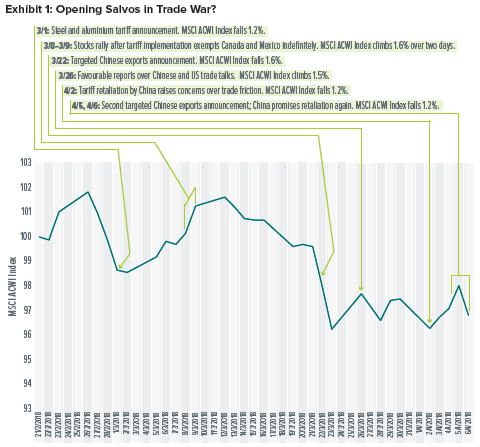

At the very least, the 1 March tweet represented the first time an economic superpower previewed a major trade policy action via social media. But it would certainly not be the last. Over the ensuing weeks, Trump followed up with a series of tweets that revealed his thinking on several trade-policy issues: the US trade deficit, disputes with major trade partners, as well as the potential for new and renegotiated trade agreements.The president’s character-limited communications served as the primary catalyst for these issues arguably having the greatest influence on global stock-market conditions in March and early April (Exhibit 1 on the next page).

A Great Wall of Trade Barriers

Dated 22 March, 2018, this tweet referenced President Trump’s signing of an executive memorandum that day imposing tariffs on up to $60 billion worth of Chinese imports (ultimately clarified in early April as 25% tariffs on 1,300 products totalling about $50 billion in goods). If stock markets were unsettled by the early March salvo, they were downright shaken by this proclamation. The MSCI ACWI Index declined by more than 1.6 percent on 22 March and then again the next day.By the following Monday, 26 March, US equities experienced a large relief rally as word circulated that the US and China were engaged in trade talks that could alleviate some of the pressure between the two countries.Trump even weighed in with some direct reassurance:By the following Monday, 26 March, US equities experienced a large relief rally as word circulated that the US and China were engaged in trade talks that could alleviate some of the pressure between the two countries.Trump even weighed in with some direct reassurance:

But market relief was short-lived. On 2 April—exactly one week after Trump’s 26 March tweet—the Chinese government announced retaliatory 25% tariffs on approximately 100 US products. The MSCI ACWI Index subsequently tumbled by more than 1.2%.Not to be outdone, the US president threatened new tariffs on an additional $100 billion of Chinese products on 5 April—inviting a promise of immediate retaliation from the Chinese government. Stock markets opened lower on the next day. Additional salvos are likely.

What’s Next?

President Trump has stated his intention to reduce the nation’s trade deficit with China—but, as is often the case with his major policy initiatives, it is hard to determine how far Trump will press his position. There has been a crackdown on China’s ability to take over certain US-based companies, yet it should be noted that this is not necessarily limited to China; the Committee on Foreign Investment in the United States is getting more aggressive on all transactions potentially involving sensitive technology transfers or national-security concerns.While the stock market’s reaction to Trump’s trade tweets has been primarily negative thus far, the first round of China-specific tariffs will take effect no earlier than 22 May-only after the US government officially stops seeking public comment on its trade plans. And even then, the US government will have 180 days at that point to decide whether to follow through with the tariffs—providing plenty of time for further trade negotiations.

The View from Wall Street: Trade Wars are Bad

The rapid market decline in response to trade concerns come as no surprise. First and foremost, markets dislike uncertainty—and trade wars are the embodiment of uncertainty. Second, the president’s perspective on trade runs counter to that of business leaders, economists and investment professionals. Trump’s tariffs, he says, are motivated by the outsourcing of jobs to low-wage countries that has eliminated high-wage jobs in the US. We agree with our industry colleagues, however, that this narrow view misses the bigger picture: the innovation that capitalism inspires has been a net benefit for the US as a whole, even accounting for its disruptive potential. Meanwhile, impediments to trade (tariffs, quotas and non-tariff barriers) have the negative effects of raising costs and reducing demand—which hurts profits and pushes share prices down.

The View from Main Street: Someone is Finally Listening to Us

When he campaigned for president, Trump successfully tapped into the angst and discontent among the vast areas of the US devastated by the loss of industries and jobs to China, Mexico, and other low-cost emerging economies over the past four decades. American textile, auto, steel and other manufacturing workers all saw high-paying jobs disappear. While the experts agree that more jobs have historically been lost than gained by the implementation of trade barriers, this offers little solace to the unemployed. Then-candidate Trump therefore drew big support in Appalachia, where tens of thousands of jobs have been lost as environmental concerns and an abundance of natural gas (associated with the fracking boom) have hastened the transition away from coal as an energy source.

Our View

While we find ourselves firmly in the majority camp of those who do not think protectionist measures will result in some sort of American renaissance in manufacturing employment, the president’s political base applauds his efforts. Trump’s approval rating has been rising steadily since the middle of December, from 37.3% to almost 42% at the end of March, according to the RealClearPolitics website, approaching its highest level since the early months of his presidency.

From an investment perspective, we maintain a positive view of equities and other risk assets, but must admit that our optimism is being tested as the Trump administration uses protectionism as a bargaining tool against friend and foe alike. We do believe the president has a legitimate criticism in the way China engages in unfair trading practices in areas like intellectual property and the forced transfer of technology from foreign companies that do business in China. However, we do not expect to see a significant reversal in terms of manufacturing jobs coming back to the US.

In our view, the imposition of tariffs on any product is harmful in and of itself—it hurts consumers and industrial users of the product much more than it helps the producers. The only good news regarding tariffs: the specific measures on aluminium and steel announced thus far should have a limited impact on economic growth and inflation. Besides, the US administration has been handing out temporary exemptions to its allies, with the notable exception of Japan. South Korea, thus far, is the only country to gain a permanent exemption from the steel tariffs, since it agreed to steel quotas and other measures beneficial to US auto and truck makers. North American Free Trade Agreement partners, Canada and Mexico, are high on the list of countries that export steel and aluminium to the U.S. They were the first two countries to be given temporary reprieves by the Trump administration as encouragement to come to terms on a revised agreement more favourable to US interests. We are in watchful waiting mode when it comes to trade.

The unveiling of tariffs on Chinese goods is concerning. A trade war of consequence could add to the inflation pressures that already are emerging as a result of the pick-up in economic activity and the tightening employment situation. We think it’s premature to expect the worst, however. Negotiations with China are already underway, and both countries stand to lose from an escalation of the trade dispute.

Until there is more clarity on the extent of the US protectionist measures being put into place and China’s response, we anticipate periodic bouts of trade-related stock market volatility will continue. Despite this, we think it’s best to focus on the strong fundamental backdrop. Profits growth remains vibrant, inflation is still well-contained, and Federal Reserve decision makers have made clear they’d prefer to normalise monetary policy in a steady, predictable fashion. For now, we favour maintaining a “risk-on” investment orientation.

Glossary of Financial Terms

Fundamentals: Fundamentals refers to data that can be used to assess a country or company’s financial health such as amount of debt, level of profitability, cash-flow, inventory size, etc.

Index Descriptions

MSCI ACWI Index: The MSCI ACWI Index is a market-capitalization-weighted index composed of over 2,000 companies, representing the market structure of developed- and emerging-market countries in North and South America, Europe, Africa and the Pacific Rim.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.