Trade Tensions Escalate from Skirmish to War

Ever since Donald Trump’s presidential victory in November 2016, we have worried about U.S. trade policy taking a major protectionist turn. For the most part, though, the U.S. president’s bark during his first year in office was worse than his bite. That no longer appears to be the case.

The imposition of U.S tariffs on aluminium and steel on most trading partners, including their closest ally, Canada, on the basis of national security, represented a small but significant signal that the Trump administration is prepared to stress the global trading system in pursuit of its “America First” goals. The personal feud between President Trump and Canadian Prime Minister Justin Trudeau not only torpedoed a calm ending to the G-7 meeting but endangered the North American Free Trade Agreement (NAFTA) negotiations which had seen some progress in recent months.

Punch and Counterpunch

A skirmish between America and China, meanwhile, has escalated into a limited-scale war. The exchanges began when President Trump proposed a 25% import tax on $50 billion worth of Chinese exports arguably to penalize China for stealing industrially-significant technologies. China immediately retaliated, announcing its own tariffs on U.S. products worth $50 billion. Not to be outdone, the White House hit back last week with suggested tariffs on an additional $200 billion worth of Chinese exports.

While these initial numbers are notable, total trade in goods between the countries (both imports and exports) totaled $636 billion during 2017, so the current level of engagement comes in at more than a mere skirmish but less than a full-scale war.

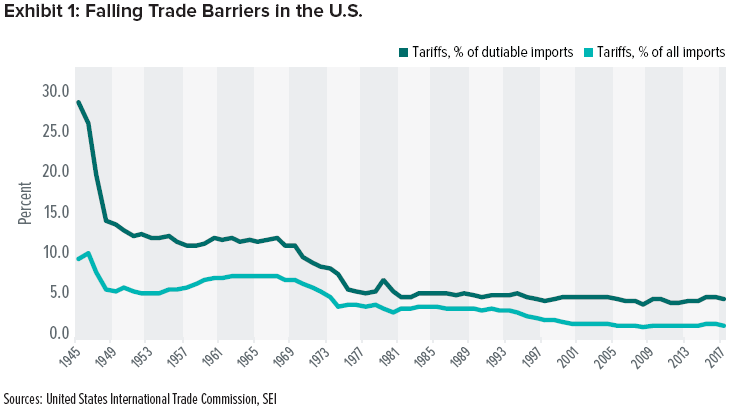

The total effect of the latest proposed tariffs would raise the overall effective U.S. tariff rate from 1.4% to about 3.4%, in line with levels last seen about 20 years ago as shown in Exhibit 1. (Effective tariff rates reflect duties collected divided by total imports. The chart captures this for all U.S. goods, not just steel or aluminium for example.)

However, there is no guarantee that this spat will be contained. While there is still time for negotiation, the Administration’s negotiating position seems to be toughening. Global stock markets have been retreating in the face of the escalation in the tariff war.

Playing to the Base

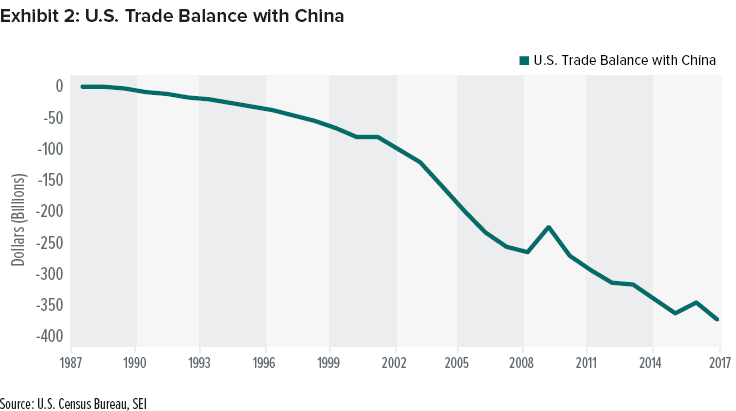

While Wall Street worries, Main Street approves. Trump was elected because he successfully tapped into the angst and discontent of Americans devastated by the loss of industries and jobs to China and other low-cost, emerging economies in recent decades. Those in the U.S. on the losing side of the global trade equation have lost big over the past 30-plus years, while emerging economies like China certainly have profited (Exhibit 2). Note the acceleration in the U.S. merchandise trade deficit with China following the latter’s 2001 admission into the World Trade Organisation.

Our View

We do not think these protectionist measures will result in some sort of American renaissance in manufacturing employment, but Trump’s political base still will likely applaud. While investors will be unhappy, it is worth mentioning that only 32% of Americans are saving for retirement in a 401(k)—an employer-sponsored retirement savings plan—according to data from the U.S. Census Bureau, and a variety of studies show that only roughly 50% invest in stock or mutual funds at all.

In our view, the imposition of tariffs on any product is harmful in and of itself—it hurts consumers and industrial users of the product much more than it helps the producers. We will be carefully watching how this drama plays out in the days and months ahead. With any luck, the Trump administration will shy away from ratcheting tensions up further. However, we must admit that doesn’t seem to be in the cards in the near term. There will be blood if the U.S. engages in a full-on trade war with China, a multi-front trade war with the rest of the world or pulls out of NAFTA.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.