Tracking error is for trackers (The risk of risk management).

By Eugene Barbaneagra, CFA, Head of Quantitative Equity Management

Warren Buffet warns investors not to put all of their eggs in the same basket. Harry Markowitz cites diversification is the only free lunch in investing. The notion of risk management has become ubiquitous. University degrees, financial regulations, and computer models have intertwined themselves across every asset class in every faucet of risk. In the midst of all this intense focus, tracking error has become one of the most prevalent measures of risk in active management. We see danger in such a myopic focus.

Introducing tracking error

Tracking error is the fluctuation (standard deviation) of a portfolio’s return relative to its benchmark’s return. The measure was originally invented to evaluate how well a passive fund “tracks” its index.

Tracking error is affected by two categories of inputs:

1. How active the portfolios is: the size of active positions against the benchmark (stock, sector, country, and factor level)

2. How volatile the market is: volatility of the benchmark and its components

In other words, the tracking error is affected by portfolio management choices (the size of active positions) and externalities (market volatility):

Tracking Error ~ Active Position * ?(Market Volatility)

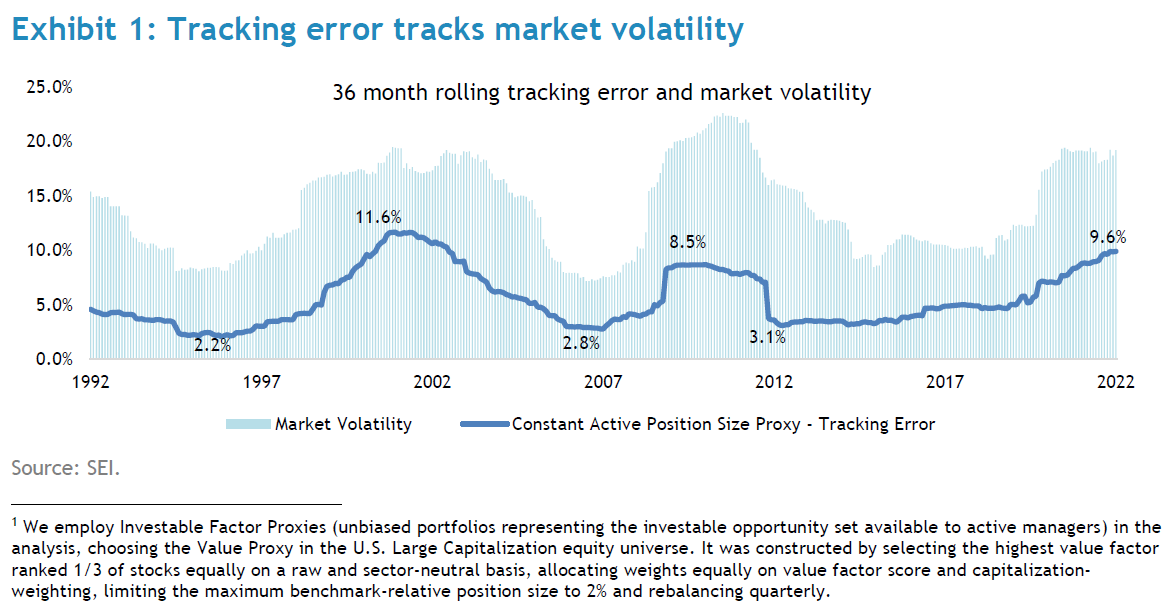

We illustrate the effect of market volatility on tracking error by keeping the size of active positions constant over the entire period using a proxy portfolio1, as shown in Exhibit 1:

From the chart, it is evident that overall market volatility has a profound effect on tracking error. Maintaining constant active positions would have produced a miniscule tracking error of just 2%-3% in some times (like 1997 and 2007) and a high tracking error of 7%-10% in others (as in 2001, 2008, and 2022). As such, even when the size of active positions is unchanged, tracking error fluctuates dramatically. The conclusion is hardly surprising–tracking error and market volatility go hand in hand, and the latter is just too variable and unpredictable.

De-risking in the rear view mirror

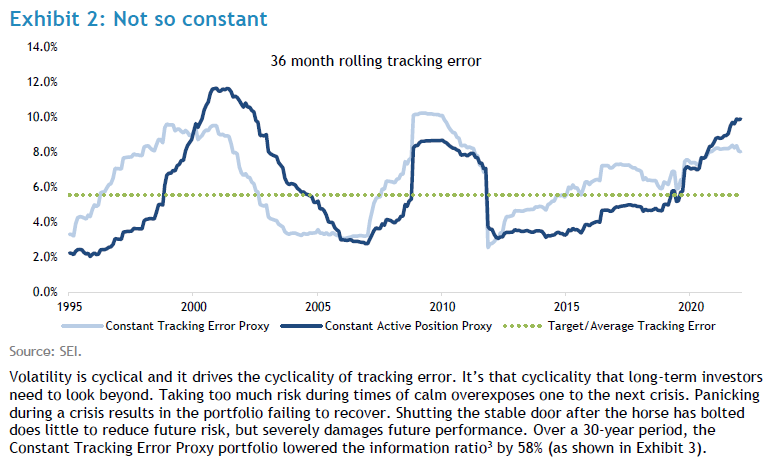

Taking the experiment a step further, whenever the observed tracking error of the Proxy portfolio deviates from the target, we mix it with the benchmark at the exact proportion so the combined past tracking error matches the target2 (which we will refer to as the Constant Tracking Error Proxy). The future tracking error will depend on future market volatility and, therefore, remains unknown.

The first obvious observation, as shown in Exhibit 2, is that the Constant Tracking Error Proxy is far from constant. In fact, it is as variable as the base case Constant Active Position Proxy. It turns out, perhaps not surprisingly, that reacting to past risk does little to mitigate future risk, particularly when such risk is out of our control, such as market volatility. Portfolio managers cannot control market volatility, so the only way to de-risk is to reduce the size of active positions.

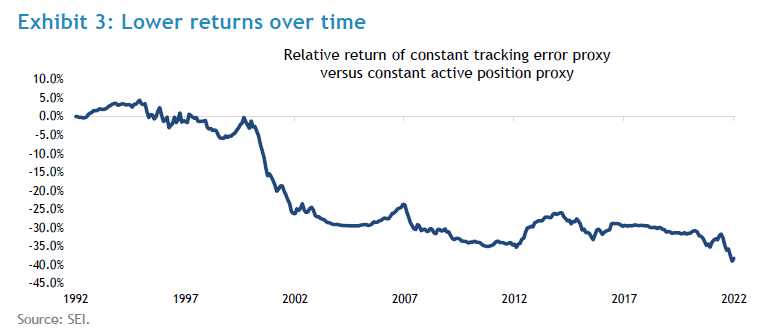

Far more worrying is the return impact of such risk management efforts. As the chart shows, the Constant Tracking Error Proxy consistently and significantly lagged the Constant Active Position Proxy portfolio.

Buyer beware

Tracking error is useful in assessing how closely an index fund tracks its benchmark. As part of the information ratio, it helps to evaluate past performance of an active manager in a relevant context: 2% alpha with 6% tracking error over the same period is well within randomness bounds, but the same alpha with 2% tracking error becomes noteworthy (albeit as elusive as ever).

Over the long-term (decades) and several market cycles, tracking error helps to form a reasonable range of expectations on relative return volatility. When this range is exceeded, it can serve as useful flag to spur deeper analysis: has the fund manager increased the size of active positions, or is it simply a more volatile market environment?

As a risk management tool, however, tracking error is dangerous. It preys on "recency" biases and breeds backward-looking mentality. It can lead to excessive risk taking at times of complacency and fuel panic during crisis episodes. Unfortunately, calculating and extrapolating it under “predicted” labels has developed into a highly profitable business line for financial systems vendors. Buyer beware!

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.