There Will Be Bumps in the Road

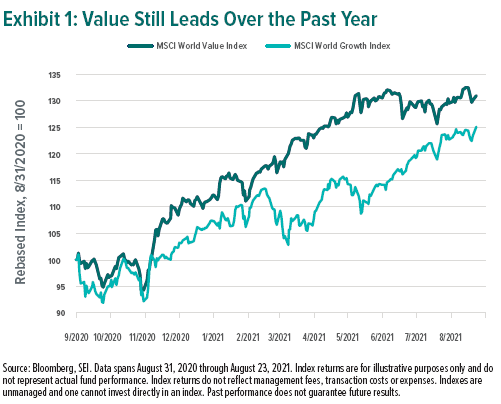

Toward the end of 2020, after several years of spectacular performance of a select group of technology-focused companies driving growth stocks (as measured by the MSCI World Growth Index) to outpace the broader equity markets, value stocks (as measured by the MSCI World Value Index) began to take the lead as a wider group of more economically sensitive companies started to push higher. Exhibit 1 shows the steady outperformance of value stocks over growth for much of the ensuing 12 months.

However, as we entered the second half of 2021, growth stocks managed to claw back some relative performance against their value counterparts—leaving some investors to wonder if the best has already come for value stocks. We do not share their unease. In our view, those relative gains for growth stocks simply represent a natural blip within a long-term market cycle—which is to be expected and should not cause concern.

Why? Because the optimistic occurrences that pushed value stocks higher at the end of 2020—broadening global earnings recovery, favorable developments on the COVID-19 vaccine front, and expanded fiscal support by central banks—are not going anywhere anytime soon.

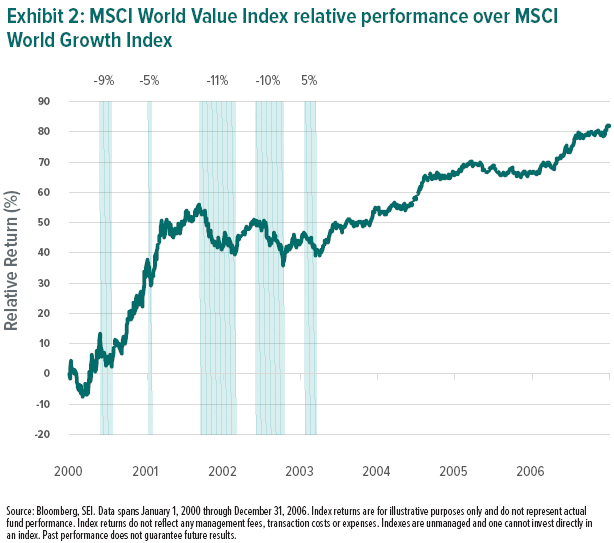

History supports this view. After the tech bubble of the late 1990s (which similarly saw growth stocks trounce their value counterparts) imploded in 2000, value trended higher over a period of about six years—even with occasional setbacks throughout that time. This is illustrated in Exhibit 2, which shows the MSCI World Value Index outperforming the MSCI World Growth Index by about 80% cumulatively from 2000 to 2006.

Investors were given reason to doubt the fundamental case for value several times throughout the long period when value steadily outgained growth. Three months after the first phase of strong outperformance—a two-year stretch that saw the MSCI World Value Index outgain the MSCI World Growth Index by about 50%—growth rebounded and gave tech shares a boost. Later, there were a handful of short-term snapbacks where the trend reversed and value gave up over 5% of its relative gains. For three of those times, growth clawed back about 10% relative to value before the value trend resumed. Looking back, we can see that investors who capitulated on their value positioning at the bottom of one of those short-term reversals may have given up on as much as half of the outperformance recorded over the entire period.

While we recognize the significant differences between the current market environment and that of 20 years ago, we believe that comparing the two periods provides useful context in understanding how a strong rotation to value leadership can play out. Most notably, it serves as a reminder that the path is often long and winding, but history showsthat growth stocks will not lead the market forever.

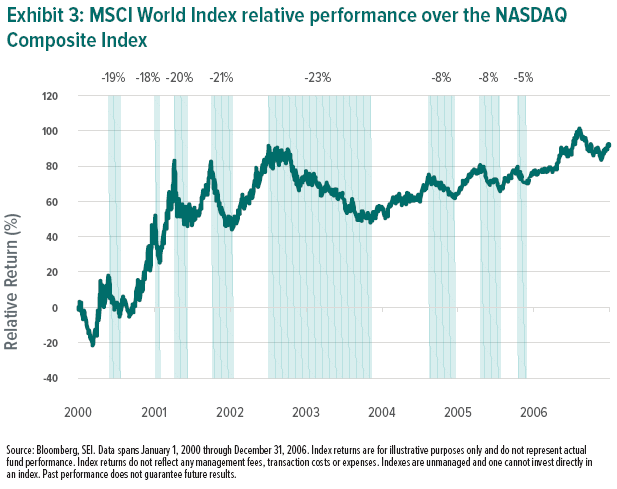

To see this through a more powerful microscope, we can examine U.S. technology stocks during the same time period as above. Using the NASDAQ Composite Index as a proxy, Exhibit 3 illustrates that U.S. technology stocks had an even bumpier ride during a long-term trend that was favorable to the rest of the world outside U.S. tech names. This time, we see even greater short-term reversals, both in magnitude and the length of time that they persisted.

While the NASDAQ Composite Index clawed back about 23% of its underperformance at one point, the overall trend continued—with the MSCI World Index extending its lead from about 50% cumulative outperformance all the way up to almost 90%. Again, an investor would have risked forfeiting significant gains if they had allowed the brief downturns to scare them into abandoning their value positions. The lesson here? Short-term reversals are not uncommon throughout the course of a long-term trend.

Our View

In our view, it’s especially important to maintain a disciplined investing approach when market environments feature unexpected (and unwelcome) setbacks. As such, we believe that the most effective investing approaches are those that focus on building diversified portfolios that are designed to strive for consistent returns over a specific time horizon in accordance with an investor’s risk tolerance.

While it’s understandable that one may want to monitor daily events, it’s crucial to bear in mind that daily, weekly, monthly, and even quarterly market movements are often relatively inconsequential for a portfolio that has a time horizon of more than a few years. If investment time horizons are measured in years, we do not think it does any good to worry about day-to-day reports of market anxieties. Instead, we believe that an investor who maintains a diversified portfolio and keeps a level head as a crisis runs its courseshould be better served in the long run.

Glossary

Bull market refers to a period of steadily increasing stock prices.

Growth stocks exhibit earnings growth above that of the broader market.

Tech bubble refers to a stock market bubble caused by excessive speculation in Internet-related companies in the late 1990s.

Value stocks are those that are considered to be cheap and are trading for less than they are worth.

Index Definitions

MSCI World Index is a free float-adjusted market capitalization weighted index that is designed to measure the equity market performance of large- and mid-cap companies in developed markets.

MSCI World Growth Index measures the performance of large- and mid-cap stocks exhibiting overall growth style characteristics in developed markets.

MSCI World Value Index measures the performance of large- and mid-cap stocks exhibiting overall value style characteristics in developed markets.

NASDAQ Composite Index measures the performance of stocks listed on the NASDAQ stock exchange. It is generally considered a stand-in for technology sector performance due to its heavy weighting in technology.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Diversification may not protect against market risk. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.