Sticking with Value: Patience and Persistence Required

Over the long run, value investing has generally outperformed the broader US equity market when it comes to building wealth. Patient investors who have stayed true to a value-minded philosophy over several economic cycles have seen compelling results as the market eventually recognised the underlying worth of the assets.

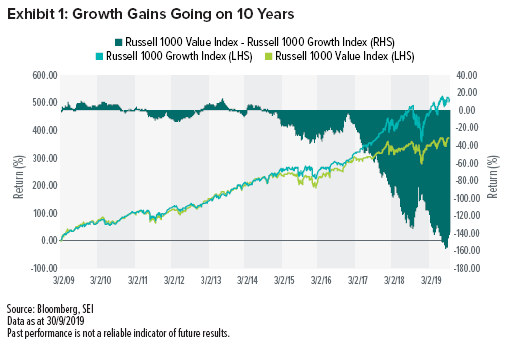

However, since the end of the global financial crisis in March 2009, the Russell 1000 Value Index has trailed the Russell 1000 Growth Index by about 3% annualised. In periods like this, when a particular area of the market underperforms relative to expectations for several years in a row, some investors are understandably tempted to stray from a commitment to their original philosophy. Exhibit 1 highlights the growing disparity between growth and value.

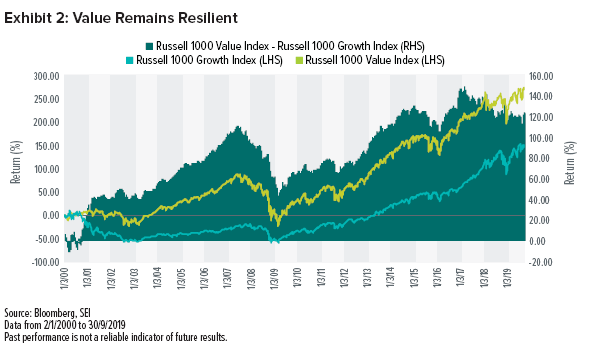

While value occasionally lagged growth over the last 20 years, value-oriented portfolios recovered each time—at least for investors who stayed the course. Despite the outperformance of growth stocks over the last 10 years, we need not look far back beyond the 10 years to witness the potential consequence of straying from value (as shown in Exhibit 2).

Between 2000 and 2019, the Russell 1000 Value Index returned 6.9% annually, besting the Russell 1000 Growth Index at 4.7%. Value investors were challenged to remain patient through multiple periods when the benchmark index underperformed its growth counterpart but still came out far ahead over full the 20-year period.

The temptation to believe that “this time is different”—that the benefit of value investing has actually run its course—becomes stronger when the outperformance of growth is fresh in investors’ minds. It is especially difficult to keep perspective when the stocks moving the growth index are those that typically receive the most media attention, including some of the larger technology companies.

There have been bouts of relatively concentrated outperformance within mega-cap growth stocks versus the broader US equity market in the past several years. Such periods often raise questions among investors about whether or not there is still a need to include value names in their portfolios. In our view, there is always a need for value exposure.

Whenever we invest in an asset class, our decision is about future opportunities. We think the lofty price of growth stocks currently suggests that near-term upside potential is limited. While it is our belief that value is poised to outperform growth in the future, there is no reliable way to predict how far into the future this shift will occur.

Value seems to be showing signs of a recovery that are still obscured by the continued rise of expensive mega-caps. We therefore believe it’s particularly important to be wary of trying to “market time” a catalyst or specific style to be in favour. Although valuation spreads are wide and there should be some reversion to the mean, we think it would still be a stretch to say with certainty that now is the exact time to buy value. Catalysts are often difficult to see or predict. Accordingly, as always, we believe in a diversified approach to investing.

In view of the vast uncertainties facing investors, the “prediction game” is arguably even more challenging than usual. We do not think it best to assume that growth stocks will always be on top—nor do we think investors should attempt a move to value that is perfectly timed with a market shift. Rather, we believe that investors are better positioned for long-term success when seeking a diversified portfolio that encompasses both asset classes, while also taking value’s historical long-run outperformance to mind. Recent volatility and sharp style rotations should serve as reminders that trends do not last forever.

Important Information

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

Past performance is not a reliable indicator of future results.

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.