The Shape of the Recovery: V, W or L? Looking Beyond the Letters

Major economic setbacks can trigger a complex re-ordering of entire industries. Our current predicament has gone even further, forcing society to function under challenging conditions with consequences for every corner of the economy.

It’s challenging to make accurate economic calls even under more normal circumstances. Add in the direct and knock-on impacts of lockdowns, the range of potential paths that the COVID-19 outbreak could take, and the countless combinations of business and policy responses under each of these scenarios, and it is truly anyone’s guess what the future holds.

Why, then, do we try to distil these setbacks into simple shapes? Because humans—and financial markets—don’t like uncertainty. Despite that, guessing whether a recession and the ensuing recovery will look like a U, V or W provides minimal benefit to long-term investors. Focusing on the underlying fundamentals and economics, we believe, is more useful for framing investment decisions.

Searching for Clues

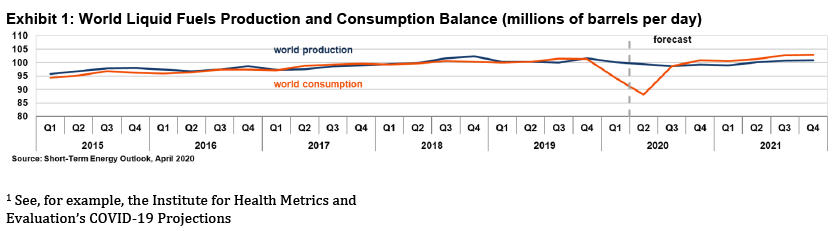

What do markets themselves suggest about the road ahead? A glance at the path of oil prices over the last few months certainly doesn’t project confidence for a strong rebound. The West Texas Intermediate oil price turned negative—a first—as its May 2020 contract neared expiration, and the June contract slid to between $10 and $20 per barrel at the end of April.

Low (and negative) prices imply that storage capacity has gotten full as demand plummeted during lockdown. The U.S. Energy Information Administration’s (EIA) April 2020 Short-Term Energy Outlook estimated “that the 2020 build could add 1.6 billion barrels to global inventories, which would fill them at or near their estimated full storage capacity levels.”

The EIA doesn’t see demand begin to cut into inventories until fourth-quarter 2020, and that assumes global consumption returns close to its long-term level starting in the third quarter (see Exhibit 1).

Interest rates also reflect considerable economic uncertainty. After falling sharply in late February and early March, long-term U.S. Treasury rates bounced into the second half of March. They have inched lower again in recent weeks. Long-term rates generally decline as economic conditions soften, so a flattening yield curve—anchored near zero on the short end—suggests there’s still great uncertainty about the economic road ahead.

Contagion Contingencies

Projections for the spread and fallout from COVID-19 have been subject to revision in recent weeks.1 First, they declined as the public adhered to social distancing and lockdown measures at a greater-than-expected rate. Then, as epidemiological models moved through their peaks and the narrative rolled on to the timing of re-opening society, policies were forced to follow—loosening restrictions and pushing projections back upward.

The fluidity of COVID-19 forecasts is compounded by their wide potential ranges of outcomes. It’s completely in keeping with honest statistical modelling to offer a base case along with low and high projections, but such a wide range limits their utility for health-system planning purposes, let alone forecasts about the economy and financial markets.

SEI’s View

We spent much of February, March and April preaching patience and moderation in the face of steep selloffs and historic volatility. We contended that the decline was too fast and that it would likely be followed by a substantial rebound.

We think moderation is warranted again, albeit in the other direction. The rebound (notably driven by the same mega-cap technology firms that led the bull market) could eventually yield to another pullback, especially given the widespread uncertainty and shortage of concrete positive developments.

We expect the re-opening of the global economy to proceed cautiously and unevenly within and across countries. Many major developed-market countries still need to establish enhanced testing to track and isolate the outbreak before returning to broader re-opening. It will take time before this accrues to a meaningful increase in economic activity.

Many emerging markets are still seeing increased infection rates, so we’re far from a return to normal conditions. Moreover, there’s a possibility we may return to lockdown later this year if COVID-19 cases appear set to spike again.

Our investment managers are thinking in terms of years, rather than months, before the corporate earnings environment recovers from below-trend economic activity to more normal conditions. We believe there will be plenty of opportunities for skilled managers to capitalise on and that investors will be rewarded for their patience and moderation through shorter-term advances and declines.

Important Information

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.