Settling into the new normal. (Long Version)

The U.S. economy got off to a strong start in 2024, but it has been posting some negative surprises. Are higher interest rates finally beginning to push inflation down in a more sustainable fashion? Time will tell. Meanwhile, the U.K. and Europe seem to be in the midst of a modest economic recovery.

Employment growth in the U.S. has been slowing and the gains in consumer spending are starting to ebb. Companies in industries as varied as airlines, discount drug stores, and fast food restaurants are reporting sales revenues below target. Apparently, consumers are pushing back against high prices. The most recent month’s inflation numbers surprised to the downside, sparking a rally in the fixed-income markets that brought the benchmark 10-year Treasury yield down by one-half percentage point from its high in April. (Yields fall as bond prices rise.) Are higher interest rates finally beginning to slow the economy and push inflation down in a more sustainable fashion? Time will tell. Meanwhile, the U.K. and Europe seem to be in the midst of a modest economic recovery, tentatively moving away from last year’s stagnant and mildly recessionary conditions.

Mid-year check in

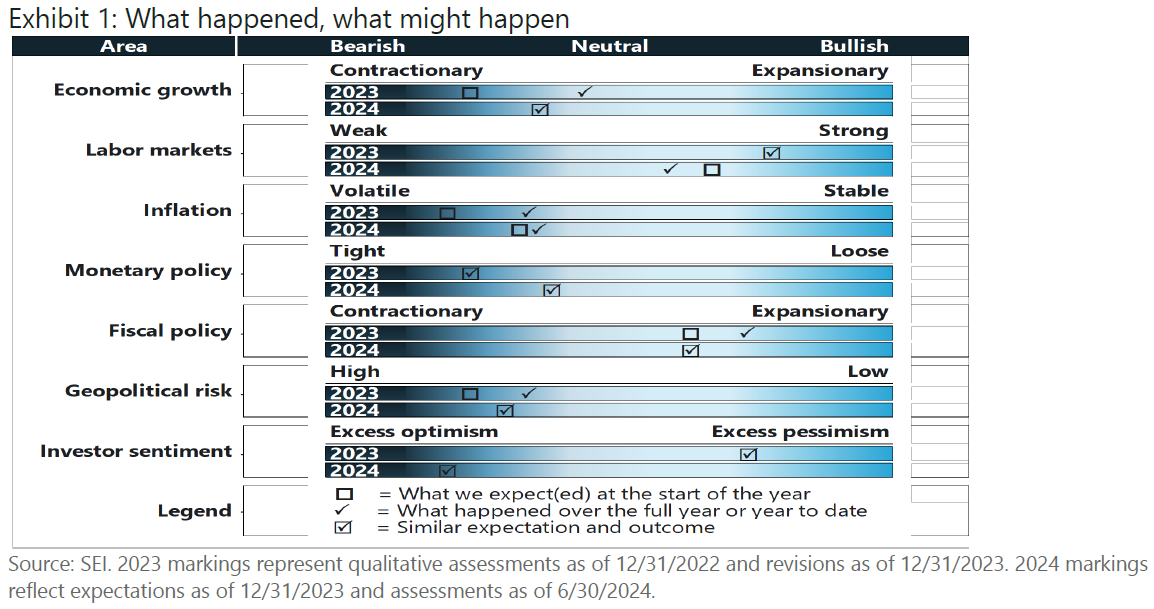

Before we delve further into the details, Exhibit 1 provides an updated version of our views on several key economic themes and policy issues that we highlighted going into the New Year. The top bar for each section reviews the forecasts we made at the end of 2022 for the year 2023. The bottom bar updates our views for 2024 versus our expectations put forth at the beginning of this year. The original forecasts are represented by the boxes in each bar, while the actual outcome for 2023 and our current assessment for 2024 at mid-year are represented by the checkmarks. Keep in mind that Exhibit 1 is only meant to provide a stylized depiction of our views.

- Economic growth: The U.S. showed signs of slowing late in the second quarter, while activity in Europe and the U.K. picked up a bit. Concerns about China remain, though policymakers there have enacted further support measures.

- Labor markets: While there are signs of marginal labor market loosening in the U.S. and some other advanced economies, overall unemployment remains low and we expect global labor market strength to persist.

- Inflation: Labor cost growth has decelerated in many countries, including the U.S. While this should help inflation pressures ease further, we believe core inflation measures will remain higher than central banks would prefer to see.

- Monetary policy: A number of central banks were expected to meaningfully loosen interest rate policy in 2024, but thus far, only a small number have, and they have done so tentatively. Cyclical upturns, still-strong labor markets, and elevated inflation are likely to keep interest rates at or near current levels for a time.

- Fiscal policy: While overall fiscal positions may be less generous than in recent years, a busy global election calendar, aging populations, and military spending should support ongoing government budget largesse. China may also encourage larger deficits in order to support its battered real estate sector.

- Geopolitical risk: The overall backdrop hasn't changed much year to date, but geopolitical risk remains above neutral. War in Eastern Europe remains a slog, hot spots continued to flare in the Middle East, and China-Taiwan remains a worry.

- Investor sentiment: Tech and AI optimism have continued to support equity markets, especially in the U.S., while credit spreads remain at or near historic lows. Financial conditions remain accommodative overall, and survey measures of investor sentiment continued to reflect optimism.

Growth trajectory as anticipated

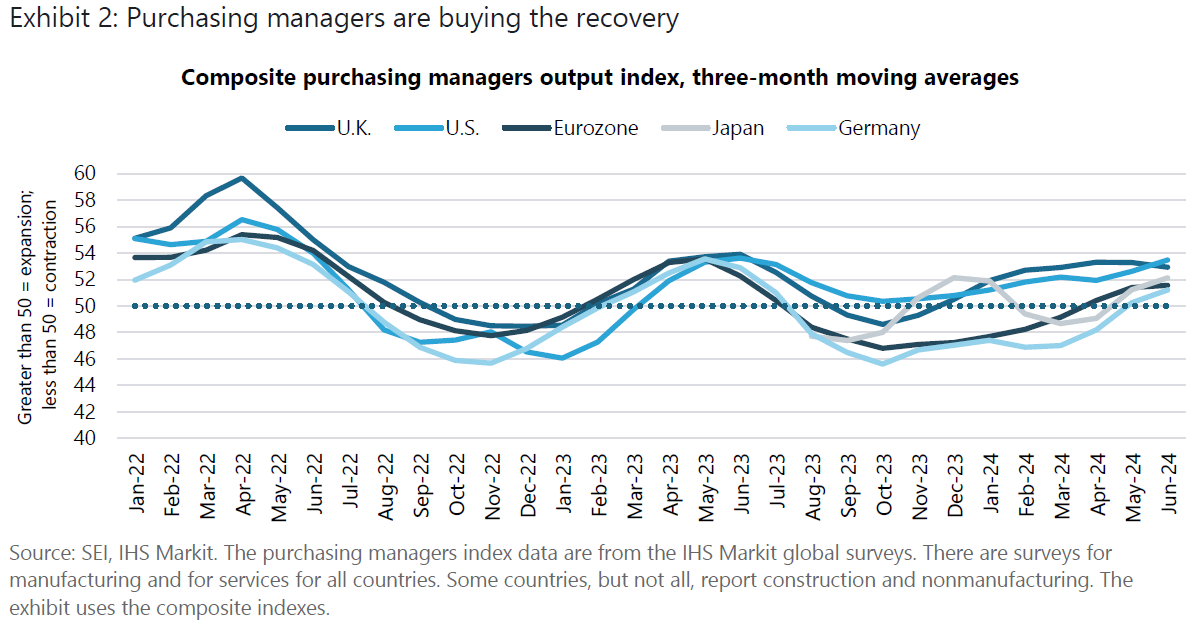

SEI anticipated that business activity in the U.S. would decelerate in 2024; so far, the economy remains fairly resilient, but signs of stress among lower-income households and mixed messages from the employment surveys suggest that the economy is downshifting to a lower growth rate, in line with our full-year expectations. Exhibit 2, which tracks the purchasing managers’ survey results for manufacturing, nonmanufacturing, and services, underscores the fact that, despite some slowing in the pace of growth, the U.S. continues to be the strongest performer among the major economies. As of May, total output was still comfortably above the 50 index level that demarcates expansion from contraction, with the index advancing to its highest level in nearly a year. Importantly, purchasing managers abroad are reporting significant improvement in their countries. Even Germany managed to get its purchasing managers index above the 50 mark in May, although other data still point to soggy economic conditions. Generally speaking, the services sector continues to be more robust than manufacturing. Globally, purchasing managers in manufacturing industries are reporting a modest expansion in output, led by the big emerging economies, especially India, Brazil, and China. From August 2022 to December 2023, global manufacturing appeared to have contracted.

Outside of the U.S., the world seems to be on sounder footing economically as we head into the second half of the year. Overall economic growth will probably continue to be somewhat below par—as we anticipated at the start of the year. The good news is that the U.S. should continue to avoid sinking into recession, while other countries enjoy somewhat better growth than experienced over the past year or two.

Labor markets are normalizing

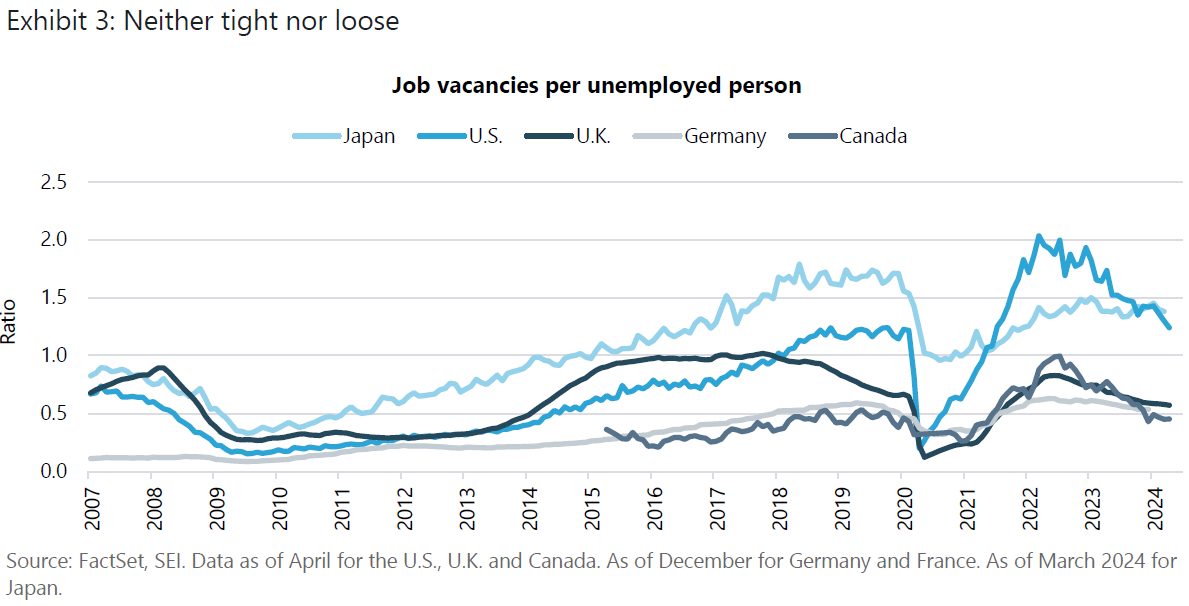

Although the global economy is growing more-or-less as expected, the labor markets in various countries seem to be loosening up a bit faster than anticipated. This doesn’t mean that employment growth is weakening in a serious way or that the unemployment rate is set to soar. Rather, labor markets among the major countries are simply returning to a more normal relationship between demand and supply. Job openings have fallen sharply relative to the number of unemployed persons. The U.S. has recorded the biggest reversion to the pre-pandemic norm, as Exhibit 3 shows. At its peak in March 2022, there were two job vacancies per unemployed person; the ratio was down to 1.2-to-1 as of April 2024. Nonetheless, even this lower level of job vacancies to the unemployed is high within the context of the last 17 years. Canada and the U.K. also have seen a significant reduction in their ratios from peaks that were considerably lower compared to the U.S.

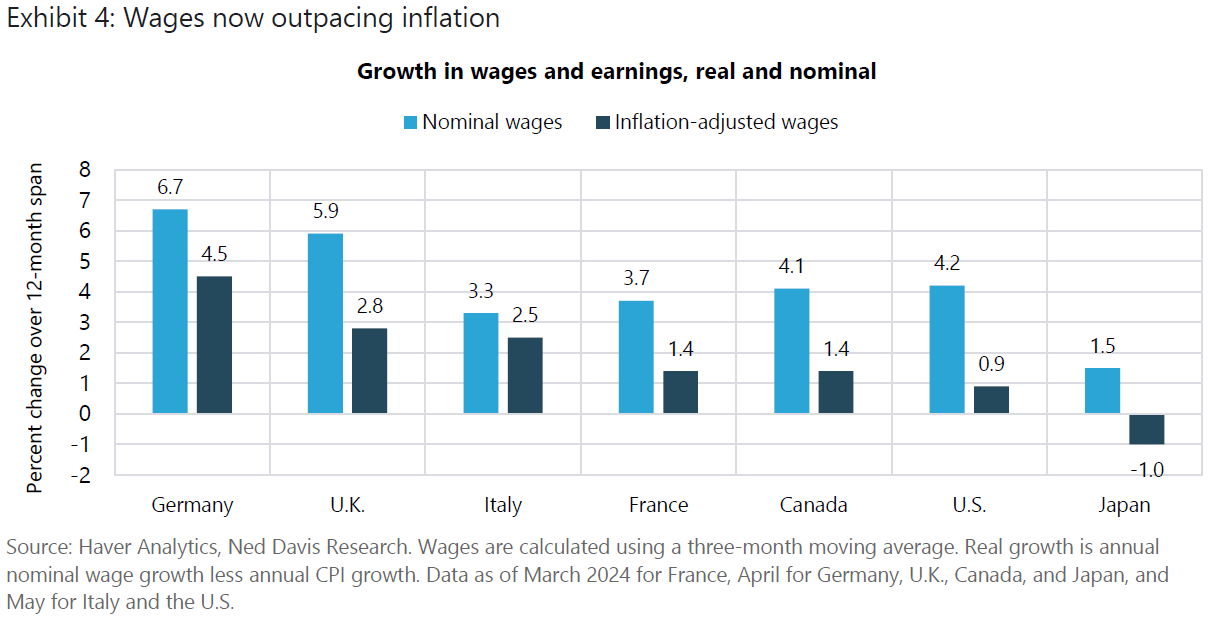

Labor markets remain strong enough, however, to keep wages at elevated levels. Exhibit 4 highlights the growth in both nominal and inflation-adjusted wages for the major developed countries. In nominal terms, the U.S., Canada, and Germany are still recording annual wage increases of more than 4%; in the U.K., the rise in earnings has been even sharper—closer to 6%. Since inflation has been declining, these nominal gains translate into positive inflation-adjusted increases for all the countries covered in the chart, excluding Japan. Given this, it’s little wonder that economic activity seems to be on the upswing. That’s the good news. The bad news is that sticky wages tend to make inflation sticky too.

Inflation is lower but not low enough

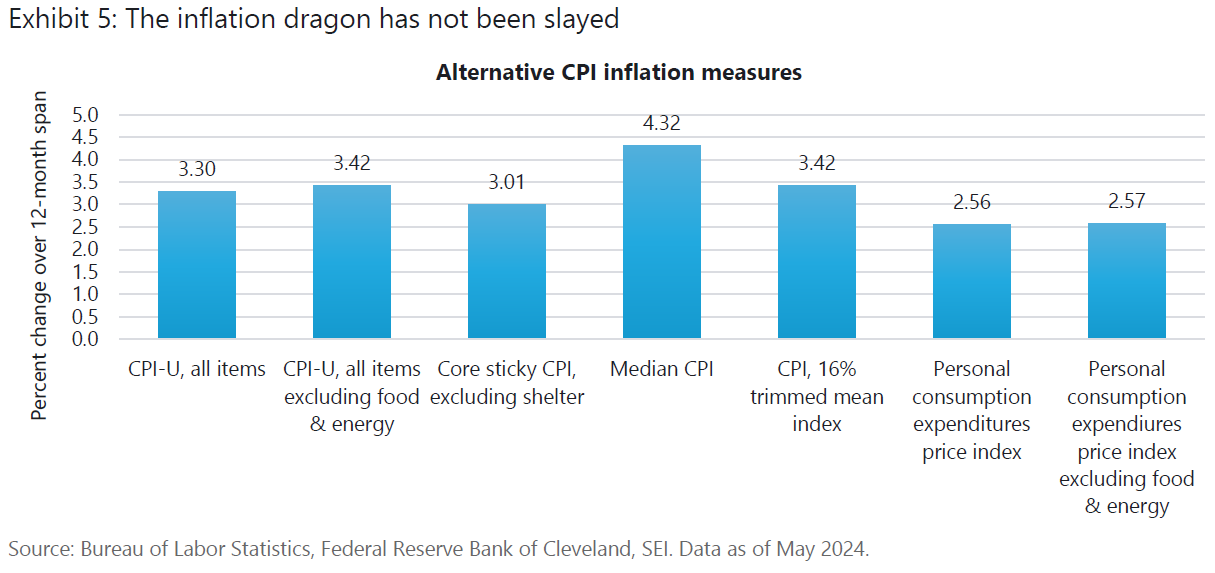

Our dashboard for consumer prices in the U.S. is highlighted in Exhibit 5. It shows that inflation remains a problem the U.S. Federal Reserve (Fed) cannot ignore. Although the headline and core personal-consumption expenditures price index have both advanced less than 3% in the past year, most other measures are still in the 3%-4% range, with the median consumer-price index up 4.3% over the 12 months ending in May. We continue to believe that inflation will remain in a new-normal range that is consistently higher than was recorded after the global financial crisis of 2007 to 2009 and before the onset of the pandemic in 2020.

Other developed countries also face a more inflationary environment, to a greater or lesser degree. The U.K. seems to have a chronic inflation problem that is somewhat worse than the U.S., notwithstanding the recent fall in the country’s CPI to a 2% year-over-year pace. The inflation deceleration in the U.K. has been powered by a 27% decline in electricity prices; services, on the other hand, continue to log price increases of nearly 6% and core inflation remains close to 3.5%.

While Canada, the eurozone, and Japan should see relatively better inflation outcomes, even they will probably endure a higher inflation rate than was typical pre-pandemic in the years ahead. Some of the potentially inflationary factors the major economies share include:

- Demographic challenges

- A burgeoning tariff war

- Realignment of supply chains and trading relationships through near-shoring and friend-shoring

- The costs of the energy transition

- Rising taxes

- Markedly higher financing costs

Monetary policy proceeding as expected

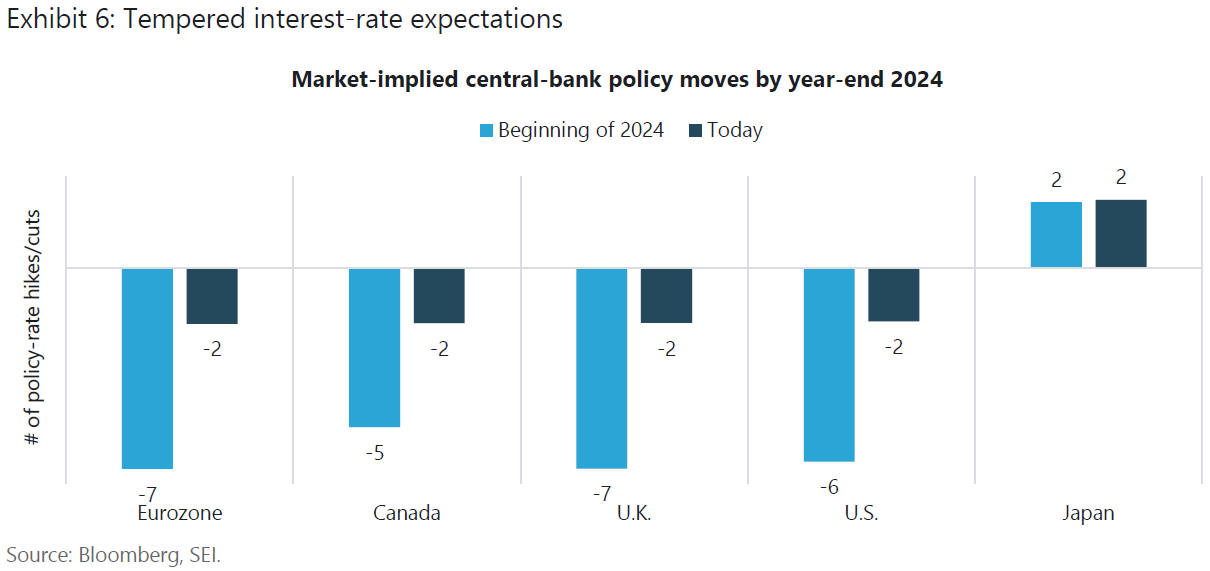

Higher-for-longer inflation should also mean higher-for-longer interest rates. At the start of the year, markets were pricing in as many as six or seven policy-rate cuts by the end of 2024 for the U.S. federal-funds rate, the Bank of England’s (BOE) bank rate, and the European Central Bank’s (ECB) deposit rate. We thought at the time that this expectation on the part of traders was overly optimistic. Sure enough, the consensus view of the number of policy-rate cuts between now and year-end have moved much closer to our own, as we show in Exhibit 6. Only Japan is expected to increase their policy rate this year, but only by 10 basis-point increments to 0.3%. By year-end, market pricing implies policy rates of 4.9% in the U.S., 4.8% in the U.K., 3.2% in the eurozone, and 4.3% in Canada.

We were not surprised that the ECB and the Bank of Canada (BOC) cut their policy rates at their respective June meetings, while the U.S. and the U.K. passed on the opportunity. We would argue that neither the BOE nor the Fed should cut rates at all for the rest of the year, but they probably will do so later in the year, with at least one reduction likely by year-end. Labor market conditions and underlying inflation pressures need to ebb further before that happens. Even the ECB seemed to be at pains to point out that further rate cuts are still dependent on signs that inflation is sustainably at or below target.

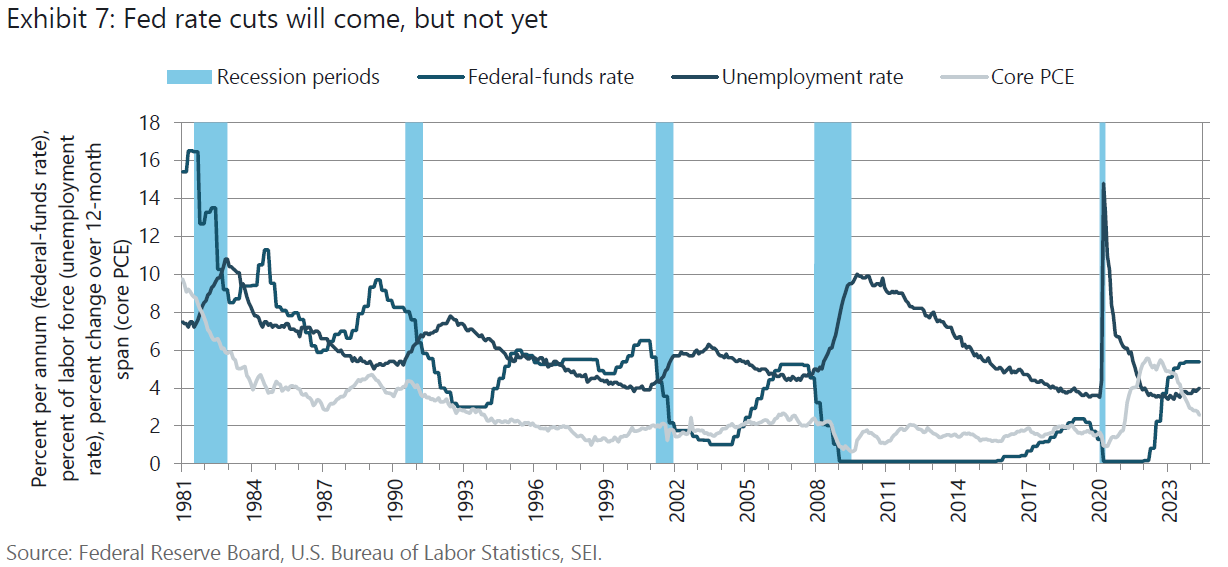

SEI does not expect the Fed to cut the federal-funds rate until November or December. Looking at history, the central bank usually engages in a sustained rate-cutting cycle when the unemployment rate starts to rise a few months before the onset of a recession. Of course, no one knows for certain that a recession is at hand, since an official determination is typically made months after the fact. During the past three downturns, the National Bureau of Economic Research (NBER) did not officially declare the start of the recession until after the business contraction had already ended.

Exhibit 7 shows the unemployment rate beginning to tick higher. Viewed in isolation, this might provide enough reason to begin an easing cycle. However, as we have noted above, the economy is still growing and the employment backdrop remains quite solid. There is still little slack in the labor market.

Additionally, the Fed’s favorite measure of core inflation—the personal-consumption expenditures price index (PCE) excluding food and energy—may be bottoming out well above the central bank’s 2% target; it remains higher than at any time since the early 1990s. If the Fed eases under these circumstances, it could cause inflation expectations to rise, perhaps pushing bond yields higher. Although the federal-funds rate is 2 1/2 percentage points above the year-over-year change in the core PCE inflation rate, that gap looks restrictive only in the aftermath of the global financial crisis and the pandemic. During the latter stages of previous economic cycles between 1989 and 2007—periods when labor markets were tight and the unemployment rate was as low as it is now—the federal-funds rate typically traded some 3%-to-5.5% above the inflation rate.

Bottom line: We continue to believe that monetary policy is restrictive, but not as much as market participants generally think. Policy rates will probably fall only gradually. Zero and near-zero interest rates are unlikely to be seen again for a long, long time, even in a recession.

Even as short-term rates decrease in response to central-bank easing moves, longer-term bond yields may not fall as far. The yield curves across the major economies, in other words, are expected to steepen. Stubborn inflation and a rise in investors’ longer-term inflation expectations are one factor. According to the Federal Reserve Bank of Cleveland, the expected U.S. 10-year CPI inflation rate has mostly fluctuated between 2.25% and 2.50% since 2022. That is roughly a percentage point higher than recorded in the years following the global financial crisis and more in line with the expectations that prevailed in the early 2000s. We think there might be more upside to yields as it becomes clear that inflation is likely to remain above the Fed’s 2% target over the course of the next several years.

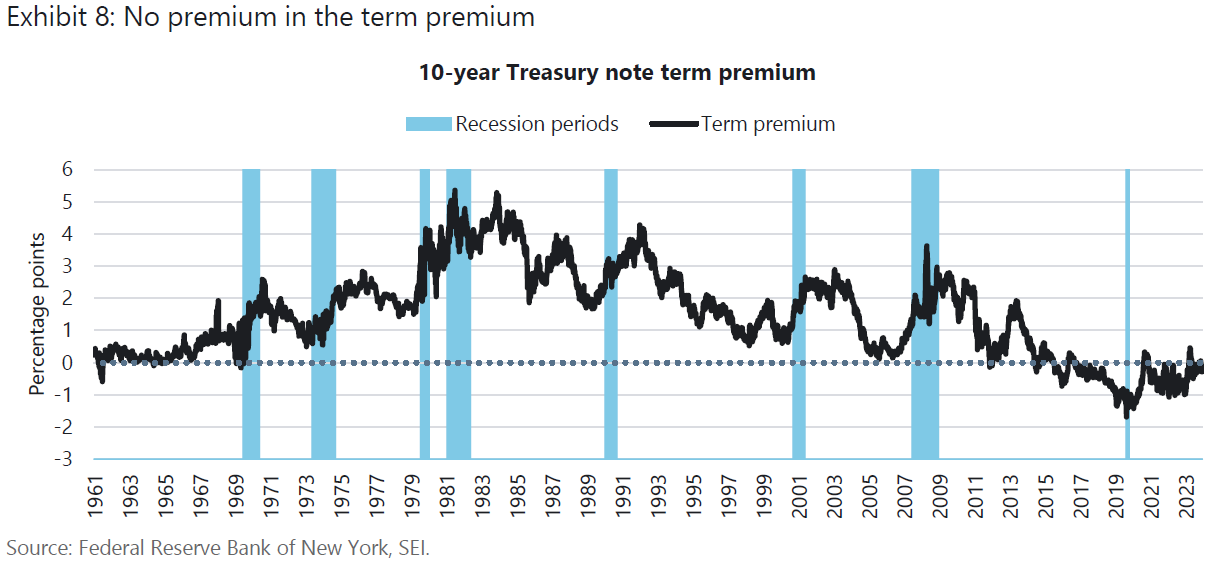

Bond yields are also likely to be bolstered by a further increase in the term premium, the additional return investors should demand for buying securities further out on the yield curve. As we show in Exhibit 8, there currently is no premium in the term premium—although it is no longer as absurdly negative as it was between 2018 and 2023. As the Fed and other central banks scale back on their purchases of fixed-income securities, the term premium on bonds is no longer being artificially depressed. This normalization of the term premium should continue in the U.S. and elsewhere because higher inflation also brings with it more volatility and uncertainty. Expansive fiscal policies and increased issuance of government securities simply exacerbate the situation.

Fiscal policy remains expansionary

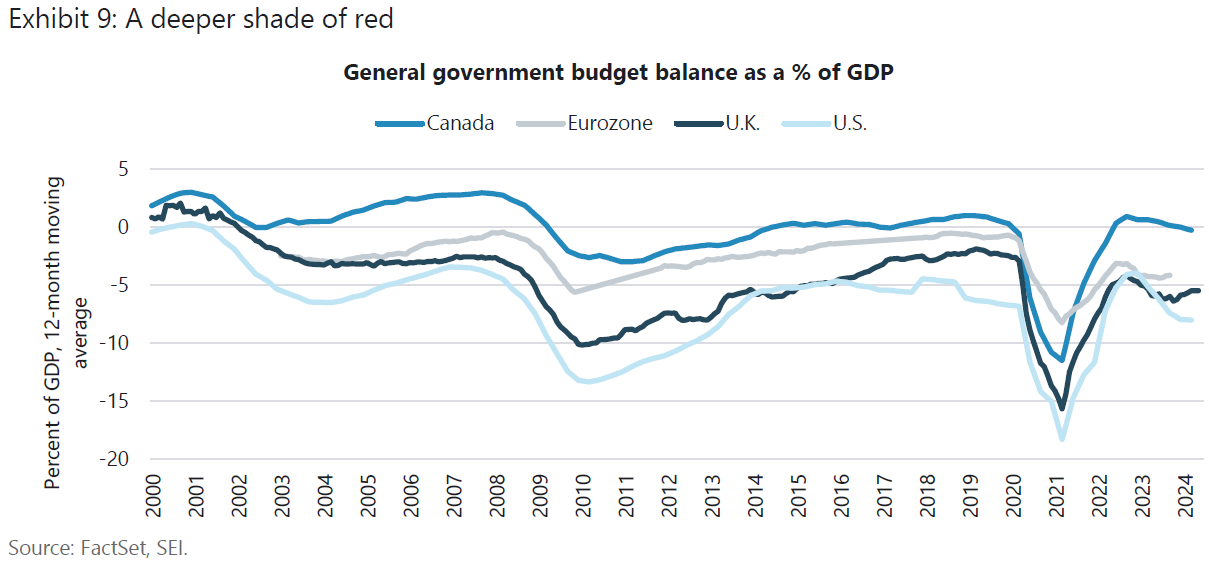

Exhibit 9 tracks the general (central plus local) government budget balances of the U.S., the U.K., the eurozone, and Canada as a percentage of gross domestic product. All have experienced at least some deterioration since 2019. Of course, the big hit to government finances occurred during the pandemic. Although there was a sharp improvement in 2021, among this group, only Canada managed to achieve a temporary surplus.

Factors that will continue to place pressure on government budgets in the years ahead include:

- Soaring interest expense

- Increased military spending in the aftermath of Russia’s invasion of Ukraine

- An aggressive push to promote industrial policy and net-zero emissions

- The inexorable increases in health care and pension costs for retiring baby boomers

At the start of this year, we anticipated some stabilization in fiscal policies at a level we would still consider stimulative to economic growth. This remains our base case.

Geopolitics remain a wild card

Geopolitical stress remains at an elevated level, although the temperature is much lower than in 2022 when Russia’s invasion of Ukraine began. Nonetheless, the war in Ukraine continues, as does the combat in Gaza. Both wars could take a sudden turn for the worse that might result in another price surge in oil and other commodities, or worse, a geographical expansion of the conflicts.

The heavy election schedule around the globe has already thrown up some surprises. In India, Prime Minister Modi suffered a surprising setback. Instead of building upon his majority in the legislature, Modi’s party lost seats, leading to a coalition government. Mexico’s election, on the other hand, gave the ruling party a near supermajority. This caused a sharp depreciation in the peso as currency traders feared there would be radical changes made to the country’s constitution that could diminish the independence of the judiciary and smooth the way for radical economic initiatives.

In Europe, the European Union’s parliamentary contest highlighted a strong performance by parties of the populist right at the expense of the center-right, center-left, and Green parties. In response, French President Macron has dissolved the National Assembly, with elections to be held on June 30 and July 7. It is quite possible that the far-right populist National Rally party, led by Marine Le Pen, will garner at least plurality of seats, ushering in a period of “cohabitation.” Under this arrangement, Macron’s responsibilities as president will be mostly limited to foreign policy and defense, while the prime minister oversees domestic and economic issues. Markets reacted quickly, with French equities falling more than 7% in a matter of days and the country’s sovereign bond yields widening sharply against German bunds.

Before the final results in France are known, the U.K. will hold its general election on July 4. The polls have consistently shown a comfortable Labour Party lead over the Conservatives. We would not anticipate a major market reaction to the potential change in government since the outcome is probably well anticipated. In addition, under Keir Starmer, the Labour Party has moved away from its more extreme economic and social positions advanced by its previous leader, Jeremy Corbyn.

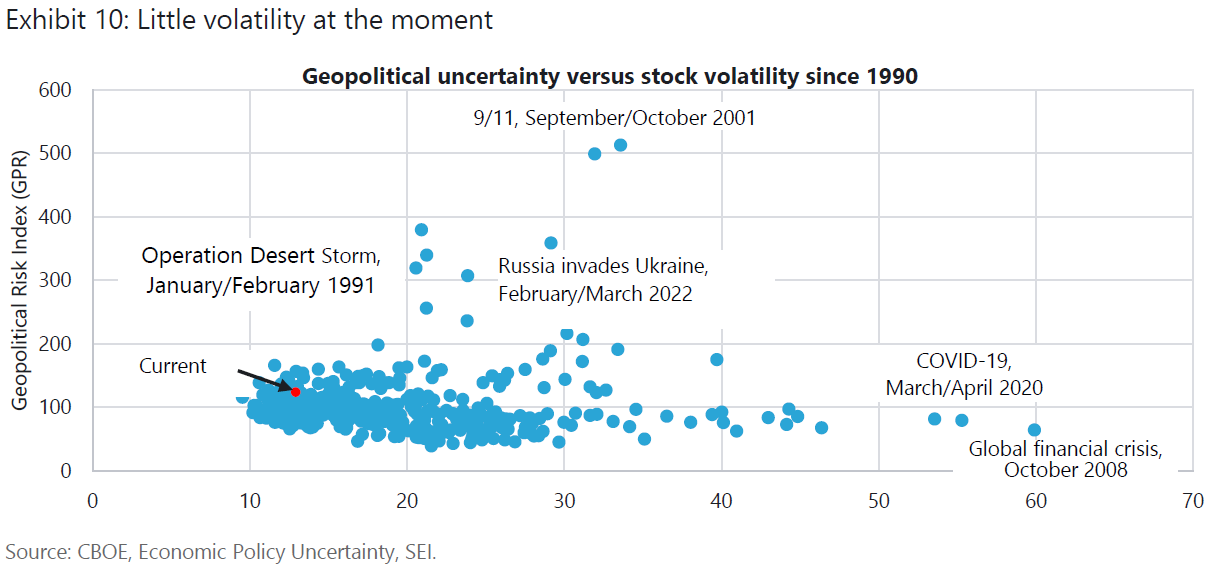

All eyes will soon turn to the U.S. elections in November. The stakes are high given the contrasting platforms of the two major parties. Not only do investors need to worry about the winner of the presidency; the composition of the Congress is just as important. Given the binary nature of the eventual outcome and the even split among the electorate, we hesitate to base any portfolio decisions purely on political considerations. Far better to stick to economic fundamentals. All in all, U.S. markets are generally taking all this geopolitical noise in stride. Exhibit 10 examines the correlation between the volatility index for the S&P 500 (the VIX index) and the Geopolitical Risk Index. The latter statistic is a measure of adverse geopolitical events and threats based on a tally of newspaper articles.

At the end of May, geopolitical tensions had calmed to their lowest level since the start of the Israeli-Hamas war in October on hopes of a near-term peace agreement (which have since diminished) and the ongoing stalemate in Ukraine. The VIX, meanwhile recently sunk to its lowest level so far this year.

While extreme geopolitical events can shock markets and cause the VIX to spike, the impact doesn’t usually last very long. The events of 9/11 and the market volatility surrounding the initial invasion of Ukraine or the First Iraq War in 1991 are cases in point. Note that the stock market has often been quite volatile when geopolitical tensions are relatively low. After all, there are factors beyond geopolitical risk that can make the stock market go haywire.

Investor optimism is high

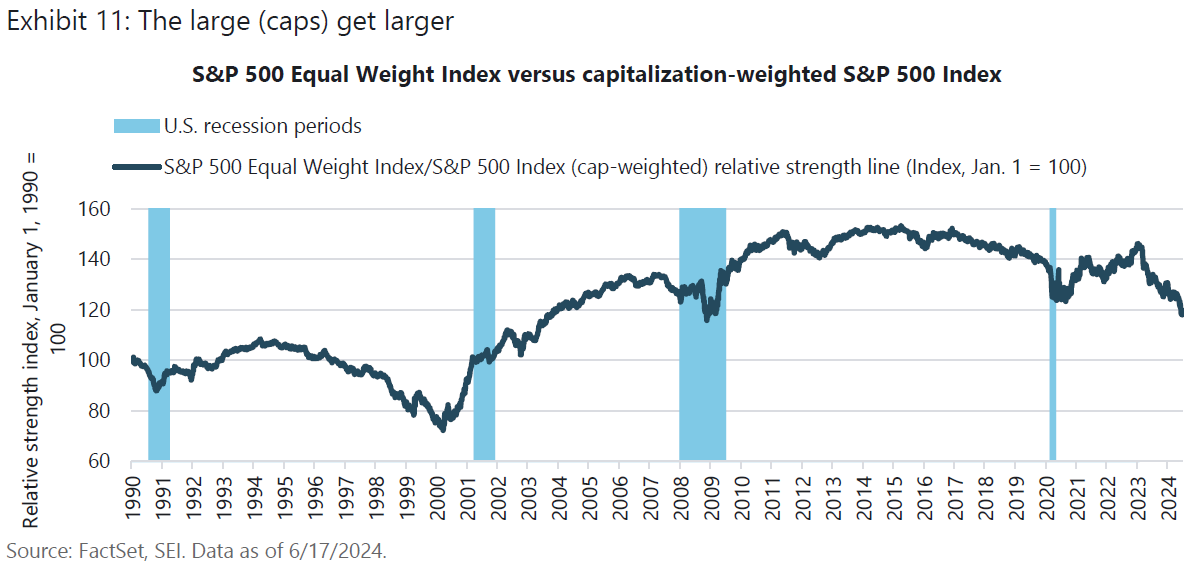

At the start of the year, SEI noted that investors were unusually optimistic. That wasn’t too surprising given the superb performance of the S&P 500 during 2023. More surprising is the strong gain in the S&P so far this year. Our expectation for a greater than 10% price correction has gone unfulfilled. Underneath the surface, however, the picture is troublesome. The performance of the S&P 500 continues to be dominated by a handful of stocks. The 10 largest companies in the S&P 500 now account for 35.6% of the total market capitalization of the index as of June 30. That is much higher than the 27% reached at the peak of the tech bubble in 2000 and in line with the concentration achieved in the early 1970s at the top of the Nifty-Fifty stock-market bubble.

Exhibit 11 tracks the relative strength of S&P 500 equal-weighted total return index (each of the components of the index is given a weight of 2.0%) versus the market capitalization-weighted (cap-weighted) index. The equal-weighted index has been lagging the cap-weighted index since January 2023, with a particularly sharp downdraft recorded in the past two months. Over this 18-month period, the total return on the equal-weighted index has trailed the cap-weighted S&P 500 by a cumulative 25.9 percentage points. Note that the performance of the equal-weighted S&P has not been all that horrible; over this span, the index has climbed a total of 19.7%. The cap-weighted total return index, however, has catapulted a phenomenal 45.6%.

There’s no denying that the extraordinary run in the biggest stocks is based on their stellar cash-flow generation and the potential impact that artificial intelligence and other technological advances could have on their future growth prospects. At the end of May, the median price-earnings ratio of the top-10 companies by market capitalization amounted to a near-record 33 times versus an elevated 23 times for the other 490 stocks in the index. The valuation gap in favor of the 10 largest companies doesn’t come close to the 30 percentage points recorded at the top of the tech bubble, but it is comparable to the levels seen in the early 1970s.

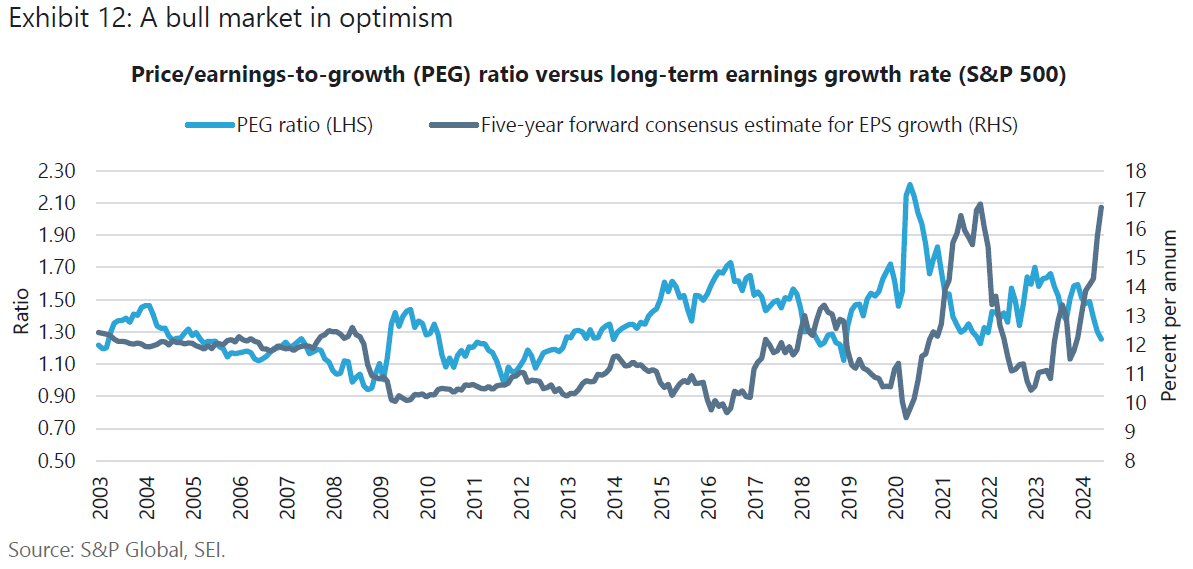

Relative to longer-term (five-year) earnings growth expectations, valuations for the S&P 500 actually appear at the lower end, based on the past 10 years, as we show in Exhibit 12. But that is because consensus estimates for growth in earnings per share (EPS) are very high, approaching 17% per annum. The only period during which this figure was higher was in the early stages of the recovery coming out of the COVID-19 lockdown. If this EPS growth estimate becomes reality, earnings for the S&P would double in just 4 1/2 years. Since 1995, there have been only three periods during which annualized five-year growth in trailing earnings surpassed 10%. The three episodes were 2002-2007 (a realized yearly gain of 13.6%), 2009-2014 (13.9%), and 2017-2022 (11.6%). In all three instances, the starting point followed five years of sub-par earnings performance. This is hardly the situation today, with actual earnings at an all-time high.

A summary of our views

SEI’s key macro themes:

- Inflation is likely to be higher for longer.

- Interest rates should settle closer to the levels that prevailed before the onset of the global financial crisis.

- Central-bank policies may diverge regarding the timing and extent of rate cuts.

- Equity and currency volatility is expected to rise from notably depressed readings.

Please refer to the latest installment of Chief Investment Officer Jim Smigiel’s SEI Forward for more details around our views and positioning.

Glossary

Policy rates are the interest rates set by central banks, used to influence other interest rates. This includes the Fed’s federal-funds rate in the U.S., the BOE’s Bank Rate in the U.K., and the ECB’s deposit rate in Europe.

The global financial crisis (GFC) refers to the period of extreme stress in global financial markets and banking systems between mid-2007 and early 2009.

Gross domestic product (GDP) is the total monetary or market value of all the goods and services produced in a country during a certain period.

P/E to growth (PEG) ratio is a variation on the traditional P/E measurement that also considers a growth component. The PEG ratio is calculated by dividing a company’s price/earnings (P/E) ratio by its growth rate of earnings. Price/earnings (P/E) ratio is calculated by dividing the current market price of a stock by the earnings per share.

Index definitions

Capitalization-weighted indexes determine the weights of their constituents based on the underlying companies’ total market capitalizations, leading larger companies to have larger allocations.

Equal-weighted indexes assign equal allocations to their constituents, leading the smaller companies in terms of market capitalization to have a larger impact than they would in a capitalization-weighted index.

The Geopolitical Risk Index is a measure of adverse geopolitical events and threats based on a tally of newspaper articles.

A purchasing managers index (PMI) tracks the prevailing direction of economic trends in the manufacturing and service sectors.

The S&P 500 Index is a market-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

The personal-consumption expenditures (PCE) Price Index measures the prices that consumers pay for goods and services to reveal underlying inflation trends. The Core PCE Price Index excludes volatile food and energy prices.

The CBOE Volatility Index (VIX) measures the constant 30-day volatility of the U.S. stock market using real-time, mid-quote prices of S&P 500 Index call and put options. A call option gives the holder the right to buy a stock at a specified price; a put option gives the holder the right to sell a stock at a specified price.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security, including futures contracts. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

Diversification does not ensure a profit or guarantee against a loss. International investments may involve risk of capital loss from unfavorable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments and smaller companies typically exhibit higher volatility. Bonds and bond funds will decrease in value as interest rates rise. High-yield bonds involve greater risks of default or downgrade and are more volatile than investment-grade securities, due to the speculative nature of their investments.

Index returns are for illustrative purposes only and do not represent actual portfolio performance. Index returns do not reflect any management fees, transaction costs or expenses. One cannot invest directly in an index.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

SEI sources data directly from FactSet, Lipper, and BlackRock unless otherwise stated.

Information provided by SEI Investments Management Corporation, a wholly owned subsidiary of SEI Investments Company (SEI). They should not be construed as investment advice.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This document has not been registered by the Registrar of Companies in Hong Kong. In addition, this document may not be issued or possessed for the purposes of issue, whether in Hong Kong or elsewhere, and the Shares may not be disposed of to any person unless such person is outside Hong Kong, such person is a “professional investor” as defined in the Ordinance and any rules made under the Ordinance or as otherwise may be permitted by the Ordinance.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This document and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs, and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.