SEI UK Strategic Portfolios - Quarterly Investment Review Q4 2021

Summary

Market overview

- Sky-high COVID-19 cases, a volatile equity-market rally, and worry over rising interest rates can describe both the first and last weeks of 2021. An obvious is that the prospect of widespread vaccination became reality, with 9 billion vaccine doses administered worldwide through the end of 2021, rendering roughly 49% of the global population fully vaccinated.

- In financial markets, the fourth quarter began in the shadow of September’s selloff, which was the most extended shakeout of 2021. After recovering in October, equities vaulted higher through mid-November before unrestrained inflation, tightening central bank policy, and the emergence of the omicron variant combined for a choppy climb to finish the year.

- Across the UK, eurozone, and US, short-to-medium-term government bond rates increased during the fourth quarter, while long-term rates declined, resulting in flatter yield curves. Fourth-quarter fixed-income performance mirrored the full year: inflation-indexed bonds were the top performers, followed by high yield. Most other sectors were mildly negative given the impact of rising rates, but global bonds were down by more due to currency effects. Local-currency emerging-market debt had the steepest losses for the quarter and year.

Stability-Focused Funds

Performance

Portfolio contributions

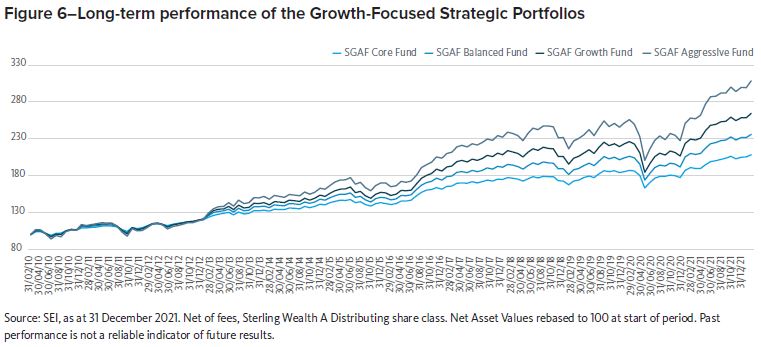

Growth-Focused Funds

Performance

Portfolio contributions

Market commentary

The final quarter of 2021 began in the shadow of September’s selloff, which was the most extended shakeout of 2021. After recovering in October, equity markets continued to move higher through mid-November before higher inflation releases, which brought with them the increasing prospect of tightening central bank policy, and the emergence of the omicron variant combined to make for a more volatile end to the year.

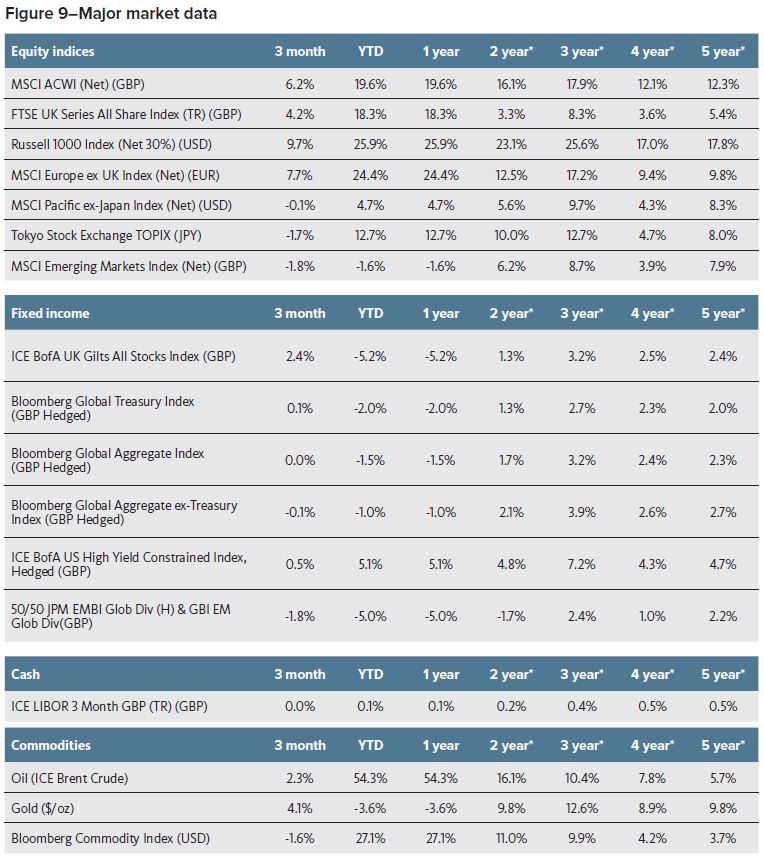

Against this backdrop, the MSCI All Countries World Index returned 6.2% in GBP terms for the fourth quarter, ending the year 19.6% higher. The US was the top-performing major equity market for the quarter and the calendar year, the European & UK markets both performed well, and Japan lagged its developed-market counterparts. Emerging markets lost ground over the quarter and year, with China delivering the deepest loss among the major markets in 2021 following a slowing Chinese economy and government regulations.

Faced with increased uncertainty over the quarter, investors shifted towards perceived safety—namely lower risk, mega cap, and higher-quality stocks across both traditional defensive sectors, such as utilities, consumer stables, and healthcare, and more cyclical growth sectors, such as luxury goods and specialty industrials. The result, from a style perspective, was that quality and low-volatility factors outperformed over the quarter. Returns from momentum were neutral in US large cap but positive outside of this segment. And results from value were mixed but generally faced headwinds due to higher exposures to energy, consumer discretionary, and financials, all of which tend to struggle during periods of rising COVID-19 concerns and a general flight to safety.

For 2021 as a whole, the environment was generally good for all three of the Portfolio’s primary equity factors. The year saw clear outperformance from those higher-quality stocks whose earnings continued to beat expectations and exhibited strong positive momentum. Cyclical stocks that recovered as economies came out of COVID lockdowns also performed strongly—IT, financials, engery, and industrials all led the way—while utilities staples, and discretionary lagged.

Across fixed-income markets, short-to-medium-term government bond rates in the UK, eurozone, and US increased, while long-term rates declined, resulting in flatter yield curves over the quarter. The performance of bond markets over the fourth quarter mirrored the full year: inflation-indexed bonds were the top performers, followed by high-yield corporate bonds. Most other segments were mildly negative given the impact of rising rates. Local-currency emerging-market debt experienced the steepest losses for the quarter and year.

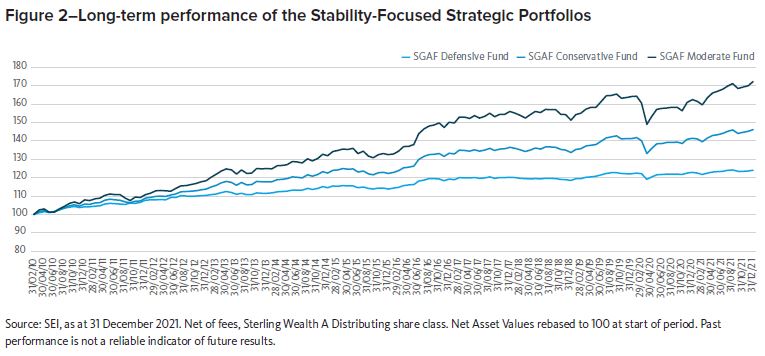

Stability-Focused Funds

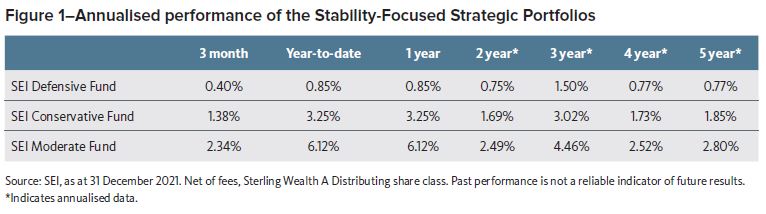

The SEI Defensive, Conservative, and Moderate Funds returned between 0.4% and 2.3% for the final quarter of 2021, with gains of between 0.9% and 6.1% for the calendar year.

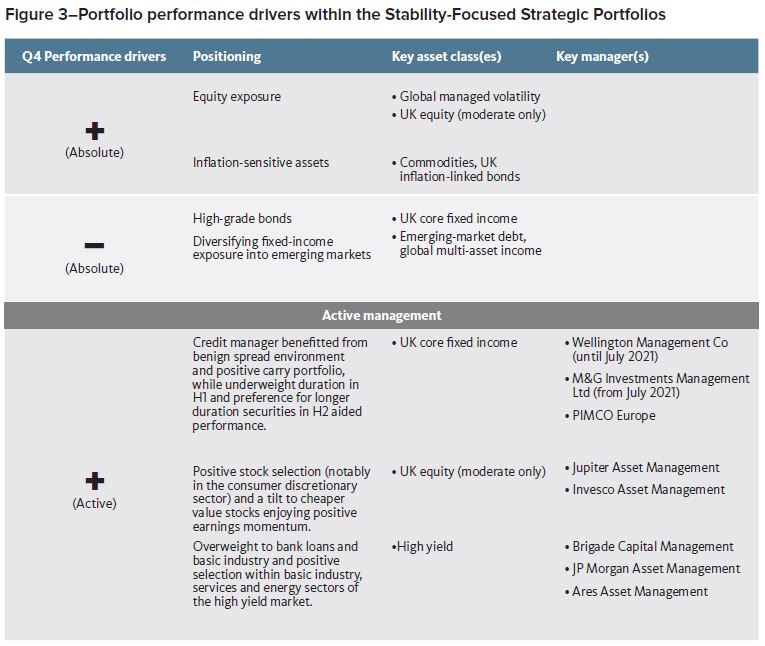

The Portfolios’ strategic positioning was broadly neutral for the quarter and positive for the year. Diversifying fixed-income exposure across high-yield and emerging-market debt worked against the Portfolios over both the quarter and the year, particularly on the back of the headwinds faced by emerging markets. However the Portfolios’ allocation to lower-volatility stocks and inflation-linked bonds were able to offset this over the quarter, and those allocations along with the commodities exposure were beneficial over the year.

Active management decisions were rewarded across the quarter and the year, thanks to positioning with UK equities, UK core fixed income, and high yields.

Within UK equities, the combination of positive stock selection (notably in the consumer discretionary sector) and a tilt to cheaper value stocks enjoying positive earnings momentum benefitted the Portfolios. At the manager level, Invesco was the strongest performer over both the quarter and the year. The manager follows a quantitative investment approach that favours higher-quality value stocks enjoying positive momentum. With the ability to take short positions in lowly rated stocks, their approach came to the fore this year. The Portfolios’ UK value manager, Jupiter, also performed strongly over the year due primarily to favourable style tailwinds, although these were mitigated in the final quarter by stock selection in financials.

UK core fixed income benefitted from a benign spread environment and positive carry portfolio provided by PIMCO (UK credit mandate), while being underweight duration in the first half of the year (through Wellington) and preference for longer duration securities in the second half of the year (M&G, who replaced Wellington in July) aided performance.

Finally the Portfolios benefitted from an overweight to bank loans and basic industry and positive selection within the basic industry, services, and energy sectors of the high-yield market. The high-yield mandates managed by Brigade, JP Morgan and Ares all performed well over year.

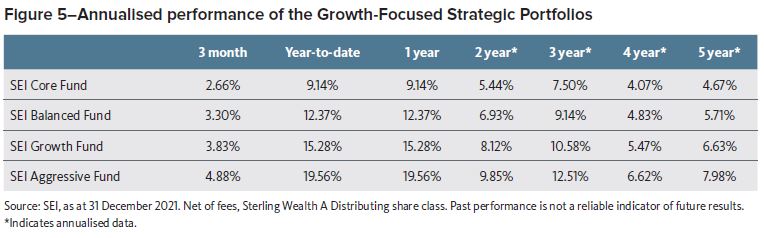

Growth-Focused Funds

The SEI Core, Balanced, Growth, and the equity-only Aggressive Fund returned between 2.7% and 4.9% for the fourth quarter, and between 9.1% and 19.6% for 2021.

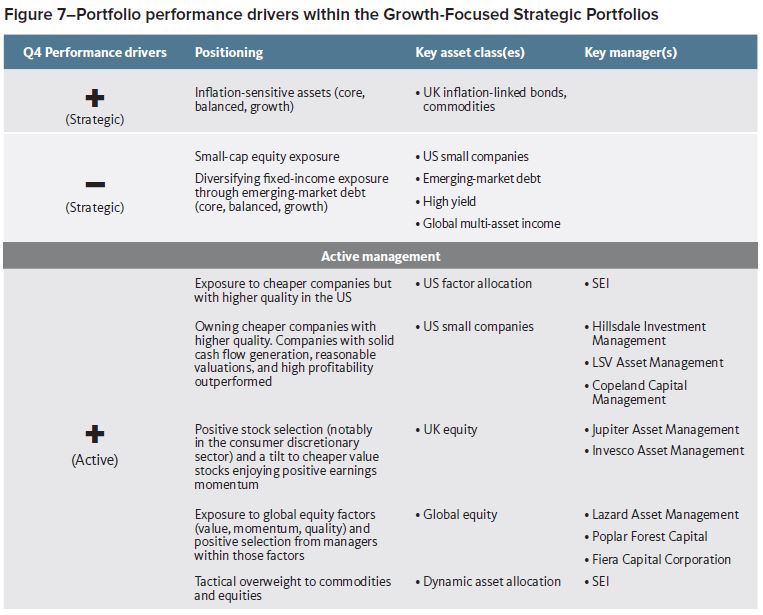

The Portfolios’ strategic positioning proved to be a mild headwind to performance over both the quarter and the year. Exposure to small-cap companies was not rewarded as smaller companies lagged their larger counterparts over both periods. With the exception of the Aggressive Portfolio, diversifying fixed-income exposure across high-yield and emerging-market debt worked against the Portfolios, particularly on the back of the headwinds faced by emerging markets. However, this was somewhat offset by exposure to inflation-linked bonds and commodities.

From an active management perspective, the Portfolios’ various equity components outperformed over the fourth quarter and the year as a whole. Within UK equities, the combination of positive stock selection (notably in the consumer discretionary sector) and a tilt to cheaper value stocks enjoying positive earnings momentum benefitted the Portfolios. At the manager level, Invesco was the strongest performer over both the quarter and the year. The manager follows a quantitative investment approach that favours higher-quality value stocks enjoying positive momentum. With the ability to take short positions in lowly rated stocks, their approach came to the fore this year. The Portfolios’ UK value manager, Jupiter, also performed strongly over the year due primarily to favourable style tailwinds, although these were mitigated in the final quarter by stock selection in financials.

The Portfolios’ allocation to US equity factors, through the SEI US Factor Allocation Fund, was also strongly beneficial over the year. Exposure to cheaper companies but with higher quality on average was the dominant driver within this component. The Portfolios also benefitted from significant outperformance within smaller-cap stocks. As market participants became more discerning, higher-risk and lower-quality stocks—those with poor earnings momentum, speculative revenue growth, or that looked very overvalued—underperformed markedly. The net result was strong outperformance from the Portfolios’ selected US and Pan European small-cap managers for both the fourth quarter and the year as a whole.

Within emerging-equity markets, concerns over a slowing Chinese economy and uncertainties surrounding its e-commerce regulations saw quality and momentum outperform over the quarter, and mildly positive results from value. While all of the Funds’ underlying emerging-market equity managers outperformed over the period, emerging Asia drove the bulk of outperformance, where positive results in IT and an underweight to the region’s healthcare stocks contributed strongly.

Across the fixed-income segments, performance was positive, largely thanks to good performance from the Portfolios’ core fixed-income and high-yield managers. Within high yield, the Portfolios benefitted from an overweight to bank loans and basic industry and positive selection within the basic industry, services and energy sectors. Brigade, JP Morgan and Ares all performed well over year.

Tactical asset allocation

The contribution from the Growth-Focused Portfolios’ tactical asset allocation positions were broadly neutral over the quarter, and strongly positive for the year as a whole. Over the fourth quarter, our tactical overweight to equities and 10-year US inflation expectations were marginally positive, commodities were neutral, and positions designed to benefit from higher yields in the US were a headwind. For the 2021, the Portfolios’ commodities exposure was the largest contributor to overall results, followed by the equity and US inflation positions.

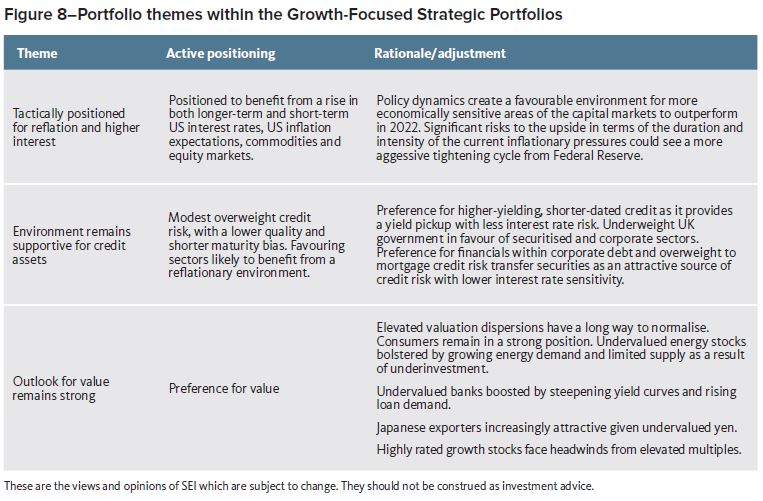

In terms of our overall positioning, we continue to express a diversified ‘reflation’ theme in the Portfolios. During the quarter, we initiated a position that allows the fund to express a view on the terminal federal funds (i.e., the rate that will be reached by the end of the next hiking cycle), which we believe may be underpriced in the current market and still reflective of a transitory view of the current inflationary pressures. We see significant risks to the upside in terms of the duration and intensity of the current inflationary pressures, and therefore to the speed and magnitude of the expected Federal Reserve tightening cycle, given easy financial conditions, the potential for additional fiscal stimulus, and a still tight labour market.

During the quarter, we also trimmed the tactical overweight to commodities. While we continue to maintain a favourable view on commodities, given the strong performance in 2021, we decided to take some profits.

Outlook and positioning

Equity markets stumbled in late 2021, owing to nervousness over the latest COVID-19 surge. This wave, too, shall pass. We remain optimistic that global growth will accelerate as the omicron wave fades. Although there have been pockets of speculative behaviour in some areas of the financial world, we do not see the sort of widespread frenzy that would point to a serious equity correction in 2022. The economy would have to slow precipitously for reasons other than the temporary impact stemming from COVID-19 mobility restrictions; the trend in earnings would need to flat-line or turn negative.

We expect a gain in overall US economic activity of around 4% in 2022—appreciably above the economy’s long-term growth potential of 2%. We also expect other countries to continue to post above-average growth as they recover from the past two years’ worth of lockdowns and shortages. With the major exception of China, which continues to pursue a zero-COVID-19 policy, most countries are unlikely to shut down their economies as fiercely or for as long as they did in 2020.

We remain optimistic that growth in the major economies will be buoyed by the strong position of households. In the US, household cash and bank deposits were still almost $2.5 trillion above the pre-pandemic trend as of the end of September. This total is equivalent to almost 14% of disposable personal income. Excess savings in the UK, meanwhile, has reached 10.6% of annual personal disposable income. Euro-area bank balances aren’t quite as high, but still amount to 5% of after-tax income.

The year ahead promises to be another one of extremely tight labour markets. We think more people will return to the workforce as COVID-19 fears fade, but there likely will still be a tremendous mismatch of demand and supply.

In our view, inflation continues to be a risk due to labour market shortages and higher raw materials cost. While central bank stimulus is set to slow down, corporate profits have remained strong, and it appears equity markets have support going into 2022. Where we depart from the crowd on inflation is in the years beyond 2022. We are sceptical that the US Fed will be sufficiently proactive as it struggles to balance full and inclusive employment against inflation pressures that are starting to look more entrenched. We believe this will be the central bank’s biggest challenge in 2022 and beyond.

In terms of Portfolio positioning, we do believe we are moving into a more supportive environment for active management in general, for a number of reasons:

- The end of easy money, brought on by policy tightening and falling liquidity in response to rising inflation

- A return to focusing on fundamentals, with unprofitable, speculative growth stocks lagging proven cash flow generators

- Headwinds to mega-cap technology stocks should see increased market breadth

- And in general, the need to be more selective

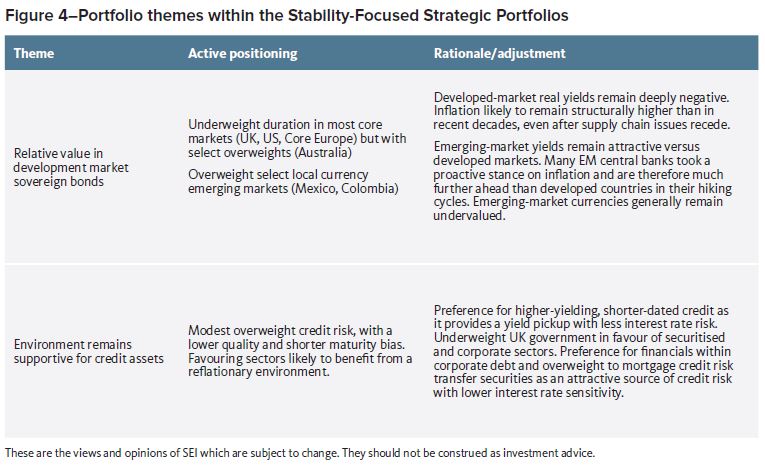

Within equities, the Portfolios target strategic allocations to value, momentum, and quality, as our key alpha sources while maintaining a tilt towards value. Elevated valuation dispersions still have a long way to normalise, and have the fundamental support to do so. From a sector perspective, consumers remain in a strong position to increase spending on discretionary items such as travel, leisure and autos, and we expect these areas of the market to recover. Undervalued energy stocks are also expected to be bolstered by growing energy demand and limited supply resulting from underinvestment, and undervalued financials should be boosted by steepening yield curves and rising demand for loans. Rising interest rates and inflation should provide a further boost to the outperformance of value and a headwind to highly rated growth stocks trading at elevated multiples.

Across the Portfolios’ fixed-income exposures, our positioning remains fairly consistent. We continue to hold a modest overweight credit risk, with a lower-quality and shorter-maturity bias, and favour sectors likely to benefit from a reflationary environment. Within government bonds markets, we remain underweight duration in the core markets (US, core Europe and UK). Within corporate credit, we have a preference for lower-quality and shorter-maturity issues, which limits our sensitivity to interest rate moves.

Manager changes

- None in the reporting period.

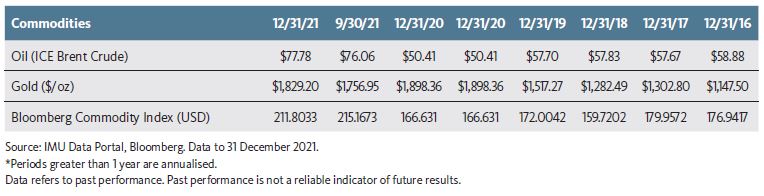

Global market performance

Representative market indices

IMPORTANT INFORMATION

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

SEI Investments (Europe) Limited acts as distributor of collective investment schemes which are authorised in Ireland pursuant to the UCITS regulations and which are collectively referred to as the “SEI Funds” in these materials. These umbrella funds are incorporated in Ireland as limited liability investment companies and are managed by SEI Investments Global Limited, an affiliate of the distributor. SEI Investments (Europe) Limited utilises the SEI funds in its asset management programme to create asset allocation strategies for its clients. Any reference in this document to any SEI funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI fund are reminded that any such application must be made solely on the basis of the information contained in the prospectus (which includes a schedule of fees and charges and maximum commission available).

The SEI Strategic Portfolios are a series of the SEI Funds and may invest in a combination of other SEI and Third-Party Funds as well as in additional manager pools based on asset classes. These manager pools are pools of assets from the respective Strategic Portfolio separately managed by Portfolio Managers, which are monitored by SEI. One cannot directly invest in these manager pools.

Past performance is not a reliable indicator of future results. Standardised performance is available upon request. All data is as at 31 December 2021.

Investments in SEI funds are generally medium to long-term investments. The value of an investment and any income from it can go down as well as up. Fluctuations or movements in exchange rates may cause the value of underlying international investments to go up or down. Investors may get back less than the original amount invested.

Asset class performance discussed is based on the majority SEI fund underlying the asset class. This does not include analysis of the manager pools, hedged share class investments within SEI Funds, additional SEI funds or any third-party funds within the Strategic Portfolios.

As a result, performance for the total asset class allocation may vary. Not all asset classes discussed are included in all Strategic Portfolios.

All asset class comparative performance is relative to the benchmark of the specific SEI fund representing the majority of the asset class investment. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the Funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

- The investment risks described below are not exhaustive and potential investors should carefully review the Prospectus prior to investing.

- The risks described below may apply to the underlying assets of the products into which the Strategic Portfolios invest.

- Investment in equity securities in general are subject to market risks that may cause their prices to fluctuate over time.

- Fixed Income securities are subject to credit risk and may also be subject to price volatility and may be sensitive to interest rate fluctuations.

Absolute return investments utilise aggressive investment techniques which may increase the volatility of returns. If the correlation between absolute return investments and other asset classes within the fund increases, absolute return investments’ expected diversification benefits may be decreased.

In addition to the normal risks associated with investing, international investments may involve risk of capital loss from differences in generally accepted accounting principles or from economic or political instability in other nations. The Funds are denominated in one currency but may hold assets which are priced in other currencies. The performance of the Fund may therefore rise and fall as a result of exchange rate fluctuations. The Fund or some of its underlying assets may hold derivatives or borrow to invest. This can make the Fund more volatile and investors should expect above-average price increases or decreases.

The views and opinions shown in this brochure are of SEI only and are subject to change. They should not be construed as investment advice.

This information is approved, issued and distributed by SEI Investments (Europe) Limited, 1st Floor, Alphabeta 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. This document and its contents are directed only at advisers of regulated intermediaries in accordance with all applicable laws and regulations. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Simplified Prospectus and latest Annual or Interim Short Reports for more information. This information can be obtained by contacting your Financial Adviser or using the contact details shown.