SEI UK Strategic Portfolios - Quarterly Investment Review Q4 2020

Summary

Market Outlook

- The fourth quarter of 2020 began at a crossroad:September delivered the first monthly loss for riskassets since the start of a rally in March, and arecovery stumbled in mid-October as a new waveof COVID-19 cases accumulated around the globe.A sharp early-November advance coincided withthe U.S. presidential election, with the market thenpropelled higher through the end of the calendaryear by a series of constructive announcementsrelating to the effectiveness, approval, anddistribution of COVID-19 vaccines.

- Emerging-market equities outpaced developedmarkets for the fourth quarter, pushing their full-yearperformance ahead as well. UK shares led amongmajor developed markets during the quarter, butstill ended up with a sizeable loss for the calendaryear. European and Japanese shares followed theUK for the quarter; both delivered positive returnsfor the full year, but Japan fared much better thanEurope

- Meanwhile, US shares had a comparably modestquarter (albeit with a double-digit gain), but had thetop major developed-market performance in 2020.Sector-level performance was shaken up duringthe final three months of the year: energy andfinancials—the top performers by a wide margin—lagged for most of 2020 and turned in full-yearlosses despite their huge fourth-quarter rallies.

- UK and Eurozone government-bond rates declinedfor the full fourth quarter. UK rates climbed throughOctober and November, before dropping sharplyacross the yield curve in December. Eurozonerates tumbled across the curve in October,before bouncing higher during November; mixedmovements in December resulting in a steeperoverall curve.1 US Treasury rates generallyincreased throughout the fourth quarter, with the10-year Treasury rate rising by more than any othermaturity

Market Overview

The end of the year forced a scramble of deal-making on both sides of the Atlantic. EU and UK negotiators attained a measure of resolution on Christmas Eve with an agreement governing some terms of their ongoing relationship.

- Trade in services, which includes the financial industry, was not addressed under the scope of the deal, and each party’s citizens will once again be subject to visa restrictions when working or travelling for an extended period in the other party’s jurisdiction.

- The Bank of England’s Monetary Policy Committee expanded its quantitative-easing programme at its early-November meeting, committing a fresh £150 billion toward bond purchases for a total of £895 billion. There were no additional policy changes at its mid-December meeting. The Committee’s latest quarterly report projected that the UK economy could contract by 11% in 2020, 2a deterioration from the 5.4% contraction estimated a quarter earlier.

- UK manufacturing activity continued to grow at a healthy rate throughout October and November before accelerating in December. The UK services sector started the fourth quarter with strong growth, which gave way to an outright contraction by November, and activity essentially maintained pace in December. The overall UK economy grew by 16%during the third quarter after falling by 19.8% in the second quarter; the economy had shrunk by 8.6%year over year through the end of the third quarter. (Source: SEI)

- The European Central Bank (ECB) made no new changes to monetary policy at its late-October meeting. Its December meeting produced a decision to increase the scale of asset purchases associated with its Pandemic Emergency Purchase Programme (PEPP) by €500 billion, for a programme total of €1.85 trillion. PEPP purchases were also extended through at least early 2022. Additionally, the ECB planned to expand theuse of its Pandemic Emergency Longer-Term Refinancing Operations (PELTRO) programme, which is designed to promote bank lending through subsidised loans. (Source: SEI)

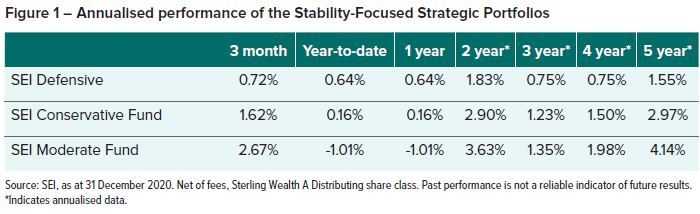

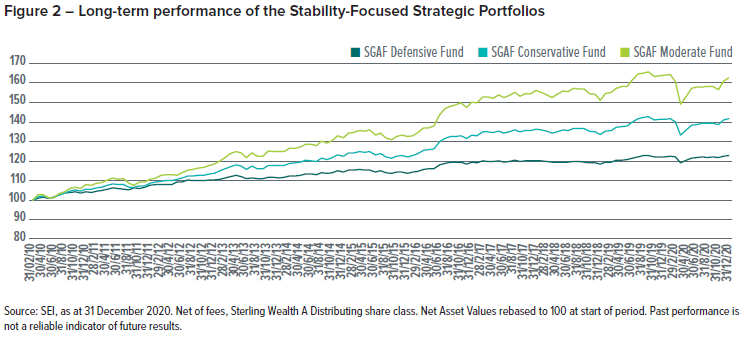

Stability Focused Funds

Performance

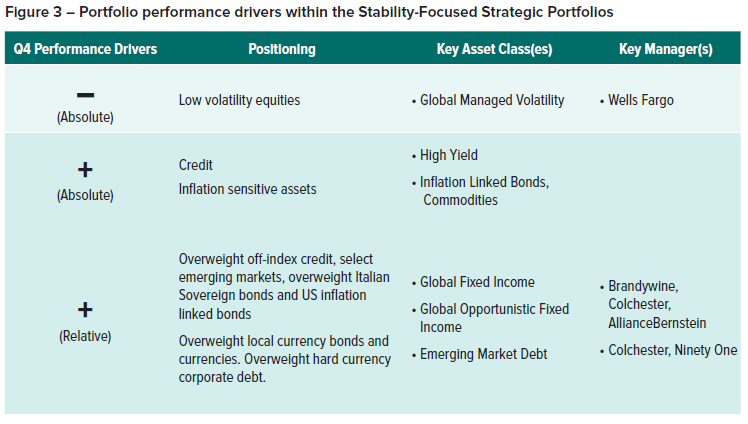

Portfolio Contributions

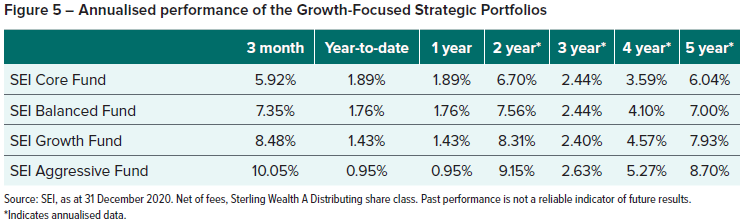

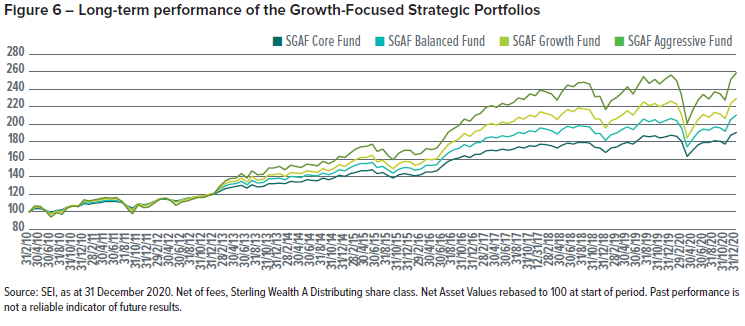

Growth Focused Funds

Performance

Portfolio Contributions

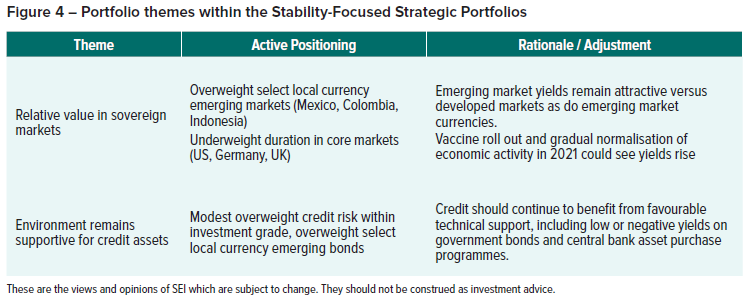

Portfolio Commentary

Fund Commentary

It was a rocky start to the final quarter of 2020 as a new wave of COVID-19 cases around the global gave investors cause for concern. However a series of constructive announcements relating to the effectiveness, approval and distribution of a number of COVID-19 vaccines along with clarity on the political front, in terms of the U.S. presidential elections and the successful conclusion of a Brexit deal, boosted investor optimism and pushed risk assets higher over the quarter.

Economically sensitive stocks, hit hardest by COVID lockdowns, led the final quarter charge as investors switched out of defensives and highly rated growth stocks. Smaller companies, Energy and Financials were amongst the strongest performing sectors while emerging market equities outpaced developed market equities.

Looked at through an alpha source lens, the scale and pace of this rotation in equity markets, out of the recent winners into cheaper laggards caused momentum orientated strategies to underperform significantly (as they always do at inflection points), higher quality, lower risk stability stocks to lag, and cheaper, higher risk, more cyclical value stocks to outperform strongly.

Within fixed income markets, global government bond yields were range bound through the fourth quarter, as markets appeared conflicted between an anticipated economic recovery in 2021 and the prospect of continued central bank support through asset purchase programmes. However, there was some notable dispersion across advanced economies, with US government bonds lagging and European peripherals, led by Italy, posted the strongest performance.

Outside of safe haven government bonds, the market exhibited an unambiguous risk-on tone: credit spreads tightened, inflation breakevens rose and emerging market yields fell, with the USD’s continued slide providing a powerful total return kicker for local currency emerging debt.

For the quarter as a whole, the Stability Focused funds returned between 0.7% and 2.7%, while the Growth Focused funds generated between 5.9% and 10.1%.

Stability Focused Portfolios

The SEI Defensive, Conservative and Moderate portfolios performed in line with expectations over the quarter.

While the risk on rally would not have favoured the lower risk portfolios’ sizable allocation to defensive, lower volatility, equities, this was largely offset by the portfolios’ strategic allocation to higher yielding credit and commodities and outperformance from the fixed income components.

From an active management perspective, the portfolios’ global fixed income component benefitted from select positions in emerging markets, a modest overweight to credit risk, Italian sovereigns and off-index positions in US inflation-protected securities. Brandywine, Colchester and AllianceBernstein were our top contributing managers in the high grade government and credit area of the portfolio.

The emerging market debt component of the portfolios also performed well over the quarter. Colchester and Ninety One, the portfolio’s local currency emerging market debt specialists, were the top contributors over the period.

Growth Focused Portfolios

Performance across the SEI Core, Balanced, Growth and Aggressive funds for the fourth quarter was strong, aided by a number of strategic allocations as well as outperformance across the fixed income strategies while results within the funds’ equity components were more mixed.

From a strategy perspective, the portfolios’ allocations to US and European smaller companies, higher yielding credit and commodities boosted returns for the quarter, although this was damped somewhat by the use of defensive, lower volatility equities within the SEI Core portfolio in particular.

Within equities, our higher quality positioning in US smaller companies, through managers like Copeland, and stock selection decisions within UK equities worked against the portfolios over the final quarter.

However within global developed market equities, the portfolios’ benefited from their pro-cyclical, contrarian positioning with an overweight to fundamental value managers, through the likes of Metropole (Europe), Poplar and Towle (US) and Jupiter (UK), who benefited from the rotation into cyclically sensitive areas of the market over the quarter.

Finally, the portfolios’ emerging market equity managers, in aggregate, made a positive contribution over the quarter. RWC was a notable outperformer, benefitting from good stock selection across Asian consumer discretionary stocks.

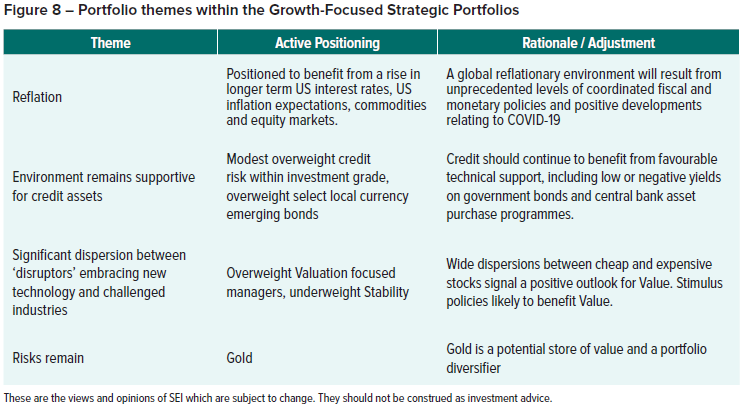

Active Asset Allocation

We believe that a global reflationary environment will emerge from the unprecedented levels of coordinated fiscal and monetary policies, as well as the positive development relating to the COVID-19 pandemic.

Central bank rhetoric continues to indicate that policy rates are on hold for the foreseeable future and that higher inflation would be welcomed. Fiscal responses to the pandemic have been significantly more concerted than they were during the global financial crisis of 2007-2009, including direct-to-consumer payments, unemployment insurance extensions, and grants and loans to small businesses, hospitals and local governments. We also expect additional rounds of fiscal measures to help address the more recent lockdown efforts.

Towards the end of the quarter, we added to, and diversified, our reflation theme within the portfolios. Specifically we have added long exposure to 1) 10-year US breakevens (which will benefit the portfolios should the market’s expectation for future inflation in the US over the next 10 years increase), 2) commodities, 3) US equities and 4) non-US equities.

We have retained our positon in gold. We continue to view gold as a safe haven asset during periods of market volatility, a portfolio diversifier and, with soaring global debt levels, increasingly likely to be seen as a store of value.

Positioning

The SEI Strategic Portfolios are positioned for a pro-cyclical economic rebound in 2021, in anticipation of vaccine roll-out programmes and normalisation of economic activity. Notwithstanding the very large output gaps that have resulted from the demand destruction caused by the pandemic, we are also positioned to take advantage of a pick-up in longer term inflation expectations.

With the fixed income components, positioning remains broadly unchanged. While we recognise that most of the capital gains from spread-compression are now largely behind us, we still think that the medium-term outlook for credit remains supportive, helped by vaccine optimism, ultra-loose monetary policy and the low (including negative) yields available on government bonds.

Within equities, we are maintaining our overall positioning in value orientated strategies. Indicators such as valuation dispersion forecast an extremely attractive outlook for value. Additionally our views are implemented through active managers, whose stock selection is expected to deliver additional returns in excess of the market over the long term.

Manager Changes

Acadian Asset Management replaced AJO’s momentum strategy in the portfolio’s US Large Companies sleeve in November. Acadian, with its well-resourced and well-experienced team, have a process that is quantitative in nature, focusing on the drivers of outperformance for the momentum alpha source.

In December, we have replaced Lazard with Robeco within the Emerging Market Equity sleeve of the portfolios. Lazard’s strategy provided various degrees of exposure to factors at various times, depending on market conditions. However, based on our current manager line-up and the market environment, we have replaced Lazard with Robeco that is expected to provide consistent value exposure over time.

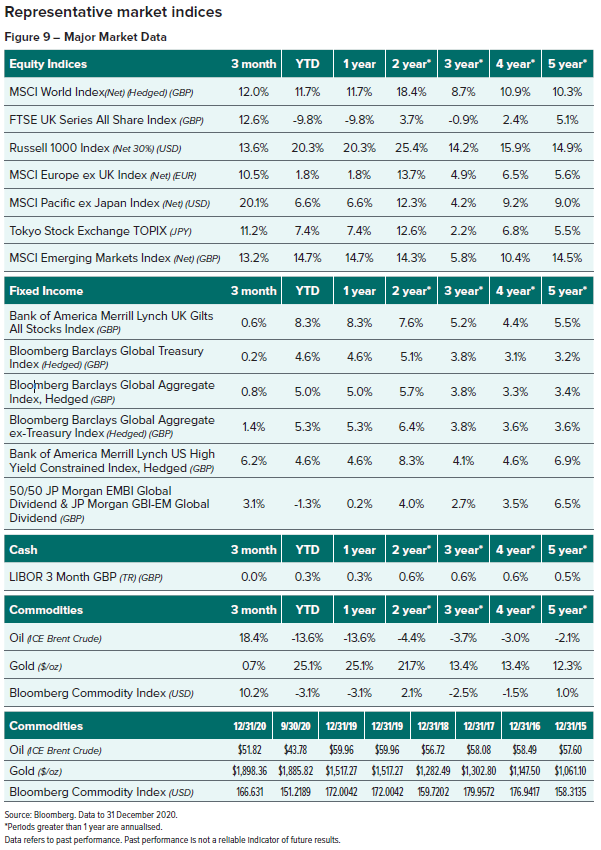

Global Market Performance

Representative market indices

IMPORTANT INFORMATION

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

SEI Investments (Europe) Limited acts as distributor of collective investment schemes which are authorised in Ireland pursuant to the UCITS regulations and which are collectively referred to as the “SEI Funds” in these materials. These umbrella funds are incorporated in Ireland as limited liability investment companies and are managed by SEI Investments Global Limited, an affiliate of the distributor.SEI Investments (Europe) Limited utilises the SEI funds in its asset management programme to create asset allocation strategies for its clients. Any reference in this document to any SEI funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI fund are reminded that any such application must be made solely on the basis of the information contained in the prospectus (which includes a schedule of fees and charges and maximum commission available).

The SEI Strategic Portfolios are a series of the SEI Funds and may invest in a combination of other SEI and Third-Party Funds as well as in additional manager pools based on asset classes. These manager pools are pools of assets from the respective Strategic Portfolio separately managed by Portfolio Managers, which are monitored by SEI. One cannot directly invest in these manager pools.

Past performance is not a reliable indicator of future results. Standardised performance is available upon request. All data is as at 31 December 2020.

Investments in SEI funds are generally medium to long-term investments. The value of an investment and any income from it can go down as well as up. Fluctuations or movements in exchange rates may cause the value of underlying international investments to go up or down. Investors may get back less than the original amount invested.

Asset class performance discussed is based on the majority SEI fund underlying the asset class. This does not include analysis of the manager pools, hedged share class investments within SEI Funds, additional SEI funds or any third-party funds within the Strategic Portfolios.

As a result, performance for the total asset class allocation may vary. Not all asset classes discussed are included in all Strategic Portfolios.

All asset class comparative performance is relative to the benchmark of the specific SEI fund representing the majority of the asset class investment. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the Funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

- The investment risks described below are not exhaustive and potential investors should carefully review the Prospectus prior toinvesting. The risks described below may apply to the underlying assets of the products into which the Strategic Portfolios invest.

- Investment in equity securities in general are subject to market risks that may cause their prices to fluctuate over time.

- Fixed Income securities are subject to credit risk and may also be subject to price volatility and may be sensitive to interest ratefluctuations.

- Absolute return investments utilise aggressive investment techniques which may increase the volatility of returns. If the correlation between absolute return investments and other assetclasses within the fund increases, absolute return investments’ expected diversification benefits may be decreased.

In addition to the normal risks associated with investing, international investments may involve risk of capital loss from differences in generally accepted accounting principles or from economic or political instability in other nations. The Funds are denominated in one currency but may hold assets which are priced in other currencies. The performance of the Fund may therefore rise and fall as a result of exchange rate fluctuations. The Fund or some of its underlying assets may hold derivatives or borrow to invest. This can make the Fund more volatile and investors should expect above-average price increases or decreases.

The views and opinions shown in this brochure are of SEI only and are subject to change. They should not be construed as investment advice.

This information is approved, issued and distributed by SEI Investments (Europe) Limited, 1st Floor, Alphabeta 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. This document and its contents are directed only at advisers of regulated intermediaries in accordance with all applicable laws and regulations. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Simplified Prospectus and latest Annual or Interim Short Reports for more information. This information can be obtained by contacting your Financial Adviser or using the contact details shown.