SEI UK Strategic Portfolios - Quarterly Investment Review Q2 2021

Summary

Market Overview

A path to a strong restart

- It looks to be full-steam ahead for the global economy and the rally in risk assets (equities, commodities, high-yield bonds, real estate and currencies).

- Equity and equity-like fixed income markets delivered gains in Q2 2021, while concerns over the state of the pandemic partially reversed the ‘great rotation/reopening’ trade.

- The big question is whether the inflationary pressures seen this year are as transitory as central bankers claim.

- Potential stock market movers include global central-bank actions on interest rates, US political support for fiscal stimulus/tax hikes and COVID-19.

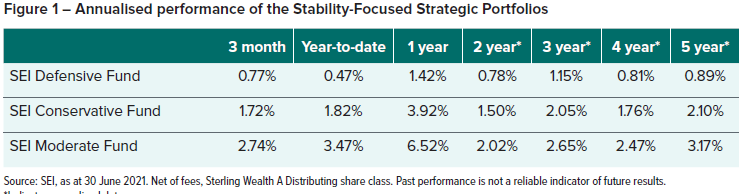

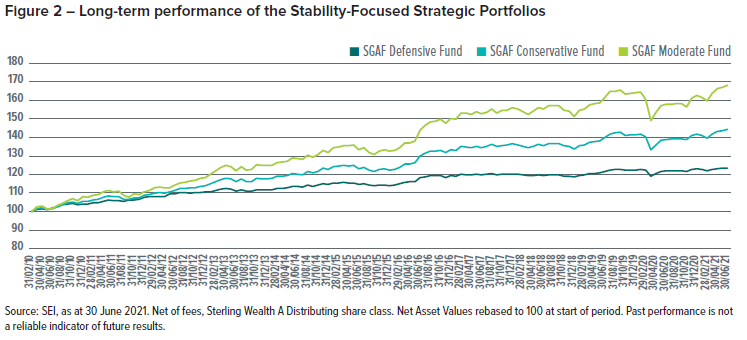

Stability Focused Funds

Performance

Portfolio Contributions

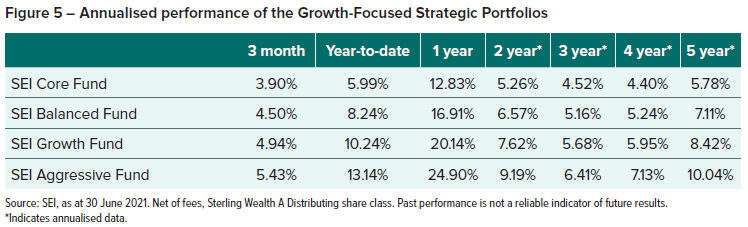

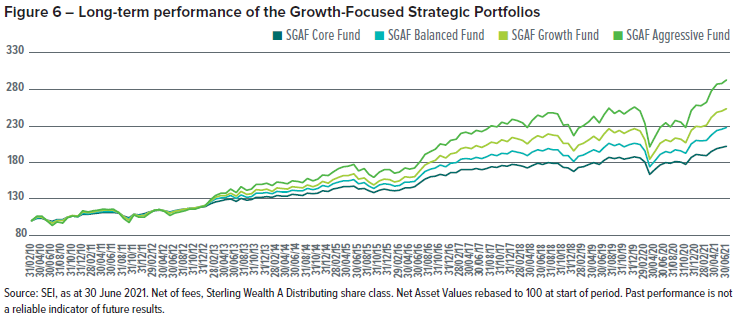

Growth Focused Funds

Performance

Portfolio Contributions

Fund Commentary

Risk assets – equities, commodities and higher yielding corporate credit - achieved solid gains over the second quarter as the global economic recovery continued to gather pace. Global equity markets, having long anticipated the economic improvement we are now seeing, for the most part delivered strong and rather uniform performance.

While equity markets continued to display a strong upward trajectory this quarter, the dynamics within markets were notably different. The reflation trade that had characterised the end of last year and the start of this year took a pause over the second quarter as investors digested recent gains and took on board falling inflation expectations and bond yields. This was compounded by a slightly more hawkish tone on inflation from the US Federal Reserve and an indication that interest rate hikes and a tapering of asset purchases may occur sooner than initially anticipated, calling into question the Fed’s tolerance for periods of higher inflation.

As a result, within equity markets, leadership rotated from non-US to US, and within the US in particular, from smaller companies to larger companies, from value to growth. Value stocks, expected to benefit from faster economic growth, rising yields and price increase, sold off sharply in June. By contrast, growth and mega-cap technology stocks strongly rebounded on lower anticipated inflation and lower interest rates. High quality and profitable companies also outperformed over the second quarter, while low volatility names lagged. Results across Momentum were mixed; the rotation away from cyclicals was a headwind for Price Momentum that had begun to gravitate towards this segment of the market, while the Earnings Revision component of Momentum was able to adjust more swiftly and generally made a positive contribution over this quarter.

Within bond markets, the quarter proved to be a relatively benign environment for government bonds and credit. Yield of development market government bonds broadly tracked sideways or slightly lower, yield curves flattened, inflation expectations receded and credit spreads continued to grid tighter. Range-bound government bond yields at an aggregate level did mask some regional differences though. After being one of the main casualties of the first quarter bond market sell-off, US Treasuries recovered somewhat this quarter, while European government bonds took their turn to feel the pressure as Europe’s vaccine rollout programme gathered pace.

Despite the slight shift in Fed rhetoric, credit spreads continued to rally against a backdrop of strong and improving credit fundamentals, abundant liquidity and persistently strong investor appetite for yield. Emerging market debt produced the strongest returns this quarter, followed closely by higher yielding corporate debt.

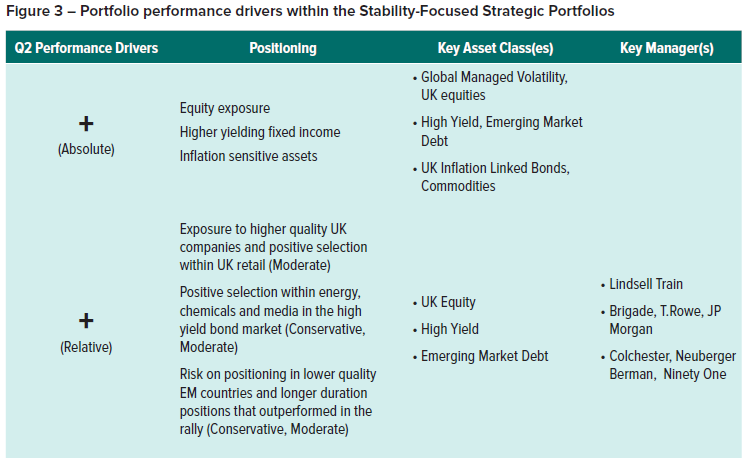

Stability Focused Portfolios

Against this backdrop, the SEI Defensive, Conservative and Moderate Funds returned between 0.77% and 2.74% this quarter.

The Funds’ exposure to equities, mostly in the form of defensive, low volatility equities, had the largest positive impact on performance. While defensive equities did not keep pace with the broad market in what was a constructive environment for global equities, they continued to provide meaningful risk reduction while posting solid positive total returns.

The Funds’ were also positively impacted by exposure to commodities as well as allocations to High Yield and Emerging Market Debt.

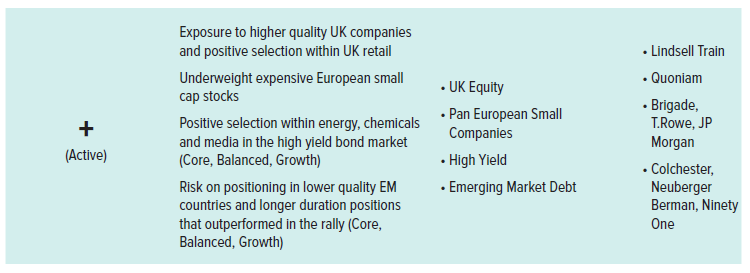

From an active management perspective, the Portfolios’ High Yield component benefitted from good security selection within the energy, chemicals and media sectors. Brigade, T.Rowe Price and JPMorgan were our top performing high yield managers over the quarter. Within Emerging Market Debt, the Portfolios’ benefitted from a general risk-on positioning and as well as longer duration positioning in those countries that performed strongly over the quarter. Colchester and Ninety One, both local currency mandates, and Neuberger Berman, who manage a blended hard and local currency mandate, were our top contributing managers.

Finally the SEI Moderate Portfolio, with a higher weight to UK equities, benefitted from its quality exposure through Lindsell Train, and positive stock selection within the retail sector.

Growth Focused Portfolios

Results for the SEI Core, Balanced, Growth and Aggressive Portfolios ranged from 3.9% to 5.43% over the second quarter.

With the change in equity market leadership this quarter, the Portfolios’ strategic allocations to smaller capitalisation stocks and diversification across higher yielding credit (with the exception of SEI Aggressive) were relative headwinds. Although in most cases was offset by the Funds’ allocation to inflation sensitive assets, most notably Commodities.

From an active management perspective, results were mixed. For those Portfolios’ with fixed income exposure, active positioning was modestly beneficial, aided by our managers’ positioning within High Yield (positive security selection within energy, chemicals and media) and emerging market debt (general risk-on positioning as well as longer duration positions in those countries that outperformed this quarter).

Within equities, and echoing the market environment from much of last year, higher risk value stocks in sectors such as Financials underperformed. The Portfolios’ pro-value positioning, as well as increased diversity by being underweight the mega-cap stocks, limited their participation in this quarter’s big-tech bounce. Those style headwinds were reflected in the portfolio of the Portfolio’s Value managers, who lagged over the quarter in line with the performance of the alpha source and diversity stance.

Small cap equity though, with its lack of exposure to mega-cap technology names, experienced contrasting style outcomes this quarter with Value extending its recent outperformance. Quoniam, the Portfolios’ Pan European Small Cap manager, benefitted by being underweight expensive European small cap stocks.

The Portfolios’ also experienced some modest outperformance from its UK equity sleeve, with strong results from our quality orientated manager, Lindsell Train, who performed well as a result of their core holdings in established consumer franchises.

Tactical Asset Allocation

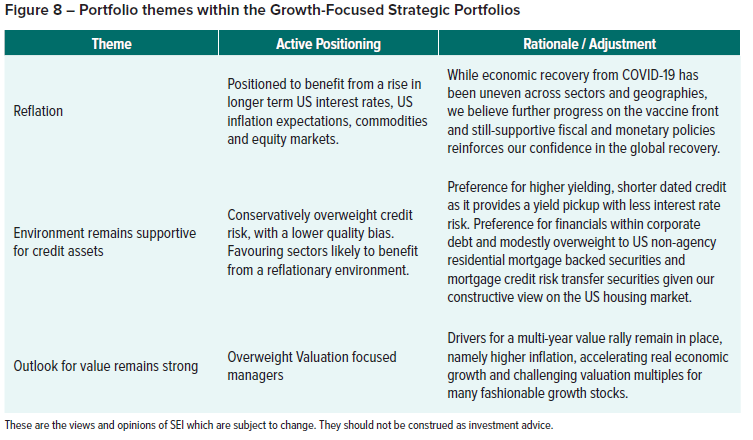

The Portfolios’ various tactical asset allocation positions experienced mixed results over the quarter, although in aggregate added value over the period. The strongest performing position was our exposure to broad commodities. All major commodity sectors produced positive returns over the quarter, led by the energy sector. Our pro-cyclical equity tilt and inflation swaps also contributed, while our positions designed to benefit from steeper yield curves and higher long term interest rates in the US detracted.

Our tactical position in Gold, which was initiated in March 2020 and reduced more recently, was closed out at the end of the quarter on the view that current prices reflect much of our original rationale for holding the position.

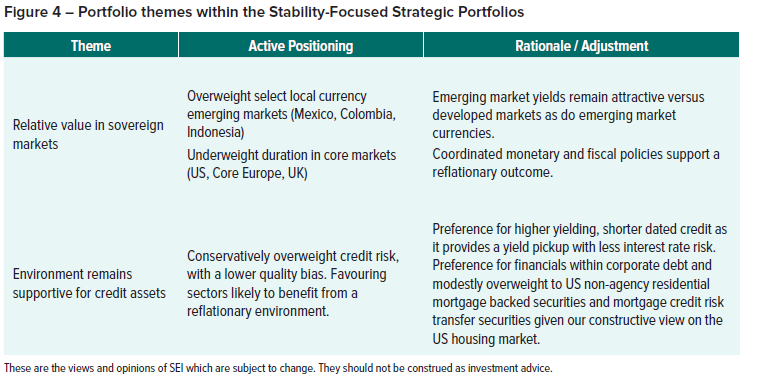

Outlook and Positioning

It remains our contention that the global recovery and expansion have a long way to go, sustained by the continued progress on the vaccine front as well as supportive fiscal and monetary policies. With economies around the world slowly opening up and interest rates hovering at extraordinary low levels, the dominant trend signals further gains over the next year or two.

Across the Portfolios’ fixed income exposures, positioning remains largely unchanged. The low spread, low volatility and low dispersion environment we currently face can be a challenging environment, and in the pursuit of excess returns it would be tempting to increase exposure to credit and/or migrate down in credit quality. However, we are also price-conscious and believe that current valuations warrant caution, notwithstanding the improving fundamental backdrop. We are therefore running fairly conservative credit overweights as abundant supply and full valuations mean that further spread compression will be a much slower grind from here.

Within equities, we maintain our strategic focus on Value, Momentum and Stability (Profitability) as our key alpha source pillars, implemented by active managers. After two strong quarters for Value, a correction was inevitable. Although it is impossible to tell how long it would last, we believe that the fundamental drivers for a multi-year value rally remain in place, namely higher inflation, accelerating real economy and challenging valuation multiples for many fashionable growth stocks.

Manager Changes

Principal Global Investors, LLC was removed from the Asia Pacific (ex-Japan) Equity building block during the quarter. We decided to remove the strategy due to organizational changes that have occurred at Principal, which caused turnover in the strategy’s senior portfolio management team. Additionally, Principal’s staffing resources have been reduced over time. The assets in Principal’s strategy have been transferred to the newly-added Sophus Capital’s Asia Pacific ex-Japan strategy.

Sophus Capital was added to the Asia Pacific (Ex-Japan) Equity building block during the quarter. The strategy has a bias towards momentum-oriented stocks, or those whose prices are expected to keep moving in the same direction (either up or down) and are not likely to change direction in the short term. We believe the combination of quantitative and fundamental inputs results in a resilient and repeatable process, enabling the team to identify opportunities quickly, while adapting and avoiding potential risks.

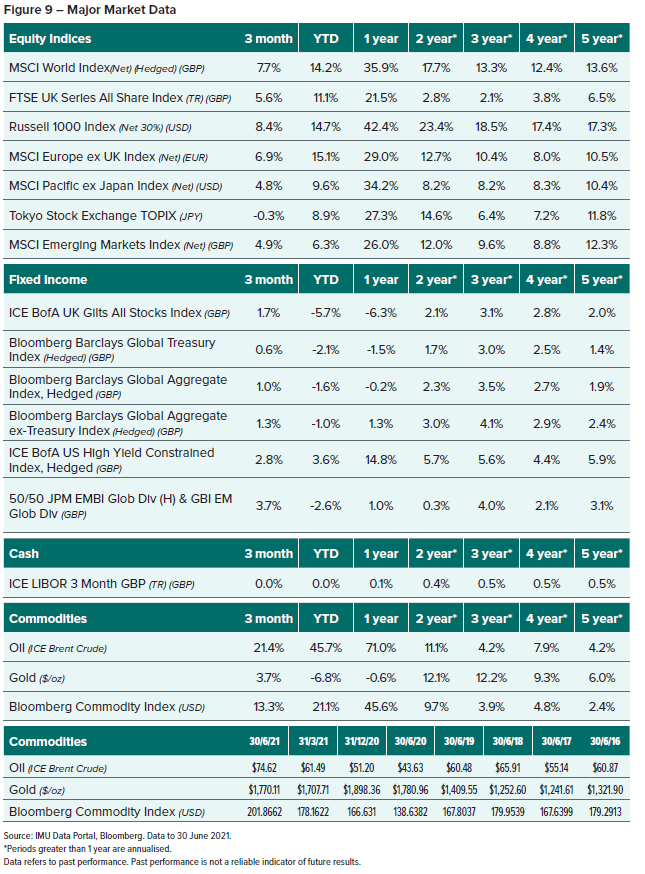

Global Market Performance

Representative market indices

IMPORTANT INFORMATION

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

SEI Investments (Europe) Limited acts as distributor of collective investment schemes which are authorised in Ireland pursuant to the UCITS regulations and which are collectively referred to as the “SEI Funds” in these materials. These umbrella funds are incorporated in Ireland as limited liability investment companies and are managed by SEI Investments Global Limited, an affiliate of the distributor. SEI Investments (Europe) Limited utilises the SEI funds in its asset management programme to create asset allocation strategies for its clients. Any reference in this document to any SEI funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI fund are reminded that any such application must be made solely on the basis of the information contained in the prospectus (which includes a schedule of fees and charges and maximum commission available).

The SEI Strategic Portfolios are a series of the SEI Funds and may invest in a combination of other SEI and Third-Party Funds as well as in additional manager pools based on asset classes. These manager pools are pools of assets from the respective Strategic Portfolio separately managed by Portfolio Managers, which are monitored by SEI. One cannot directly invest in these manager pools.

Past performance is not a reliable indicator of future results. Standardised performance is available upon request. All data is as at 30 June 2021.

Investments in SEI funds are generally medium to long-term investments. The value of an investment and any income from it can go down as well as up. Fluctuations or movements in exchange rates may cause the value of underlying international investments to go up or down. Investors may get back less than the original amount invested.

Asset class performance discussed is based on the majority SEI fund underlying the asset class. This does not include analysis of the manager pools, hedged share class investments within SEI Funds, additional SEI funds or any third-party funds within the Strategic Portfolios.

As a result, performance for the total asset class allocation may vary. Not all asset classes discussed are included in all Strategic Portfolios.

All asset class comparative performance is relative to the benchmark of the specific SEI fund representing the majority of the asset class investment. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the Funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

- The investment risks described below are not exhaustive and potential investors should carefully review the Prospectus prior to investing. The risks described below may apply to the underlying assets of the products into which the Strategic Portfolios invest.

- Investment in equity securities in general are subject to market risks that may cause their prices to fluctuate over time.

- Fixed Income securities are subject to credit risk and may also be subject to price volatility and may be sensitive to interest rate fluctuations.

- Absolute return investments utilise aggressive investment techniques which may increase the volatility of returns. If the correlation between absolute return investments and other asset classes within the fund increases, absolute return investments’ expected diversification benefits may be decreased.

In addition to the normal risks associated with investing, international investments may involve risk of capital loss from differences in generally accepted accounting principles or from economic or political instability in other nations. The Funds are denominated in one currency but may hold assets which are priced in other currencies. The performance of the Fund may therefore rise and fall as a result of exchange rate fluctuations. The Fund or some of its underlying assets may hold derivatives or borrow to invest. This can make the Fund more volatile and investors should expect above-average price increases or decreases.

The views and opinions shown in this brochure are of SEI only and are subject to change. They should not be construed as investment advice.

This information is approved, issued and distributed by SEI Investments (Europe) Limited, 1st Floor, Alphabeta 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. This document and its contents are directed only at advisers of regulated intermediaries in accordance with all applicable laws and regulations. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Simplified Prospectus and latest Annual or Interim Short Reports for more information. This information can be obtained by contacting your Financial Adviser or using the contact details shown.