SEI UK Strategic Portfolios - Quarterly Investment Review Q1 2020

Summary

Market Review

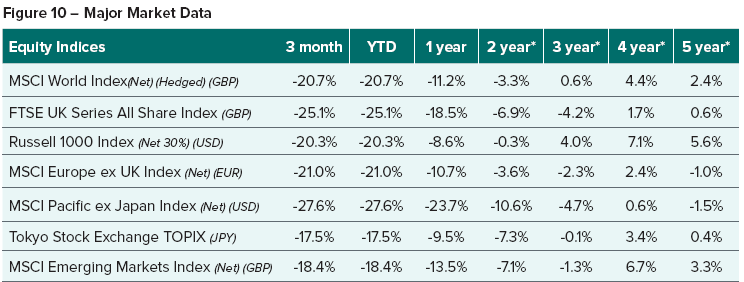

- The speed and magnitude of the Coronavirus (“COVID-19”) outbreak and the actions necessary to contain its spread have dramatically changed the daily lives of billions of people worldwide, and consequently impacted all global financial markets. The MSCI World Index, in GBP terms, was down -15.7% for the quarter while the FTSE All Share Index end the period -25.1% lower.

- Central Banks and Governments have reacted aggressively and innovatively to help mitigate the impact of the economic shutdown. Base rates have been cut to near zero in both the US and UK, quantitative easing programmes have been restarted and expanded considerably to help improve liquidity in financial markets and substantial fiscal programmes have been established to aid individuals and businesses.

- Initially it was energy and commodity stocks and companies within the travel industry that fell most sharply. As the crisis has unfolded and whole countries have gone into lock down, selling became indiscriminate, with stocks falling across the board, leaving no place for investors to hide. From its peak on the 19th February, the US stock market declined by over 30% in a month, outpacing the bursting of the internet bubble in 2000 and the subprime crisis in 2007/8 (source: Bloomberg).

Market Outlook

- There are early signs that the spread of the virus is being brought under control in key areas within Europe and the US, however, uncertainty remains high with respect to the full extent of the virus’s economic impact and the timetable for an exit strategy from stay-at-home guidelines.

- China was the first country to be impacted by the virus, and it was also the first to begin to recover from it; a strong bounce back should help other economies.

- This current crisis and the fiscal stimulus that it has prompted may well prove to be the catalyst for a rotation in market leadership that will create a more favourable environment for active managers, as stock returns diverge and market indices become less top-heavy and concentrated. This should bode well for active managers following a proven, long-term approach, and we expect market conditions to remain challenging, and active management, in our view, is key given idiosyncratic vulnerabilities.

- SEI’s Economic Outlook Q1 2020 is available at the following link: seic.com/Q1Outlook2020

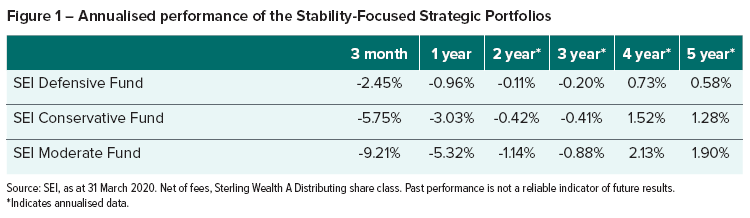

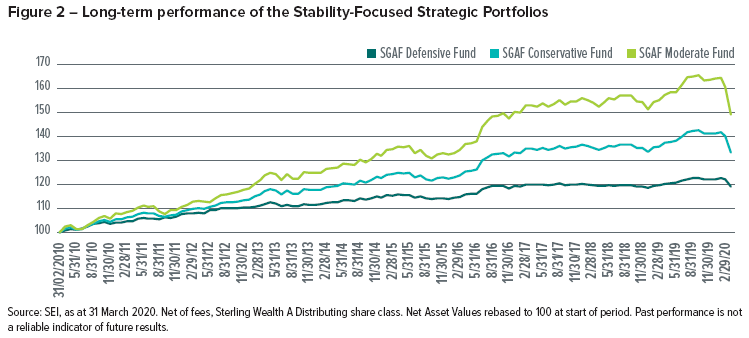

Stability Focused Funds

Performance

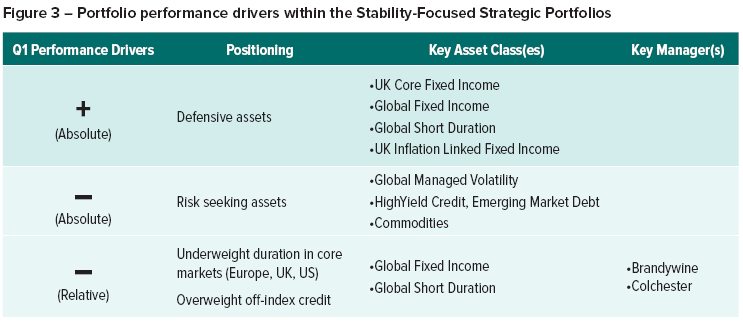

Portfolio Contributions

Portfolio Commentary

These SEI Stability Focused Strategic Portfolios are designed for investors who are trying to protect against losses while working towards a comfortable level of growth. They are managed specifically to mitigate the risk significant peak-to-trough drawdowns.

Our asset allocation and portfolio construction process incorporates metrics such as peak-to-trough decline in a poor market environment into the overall assessment of the risk inherent in a particular asset class, with the intention of emphasising those asset classes and strategies that present attractive growth potential relative to their risk of absolute loss.

Two asset classes that play an important role in delivering the expected outcomes, particularly relative to peers, are short duration bonds and low volatility equities.

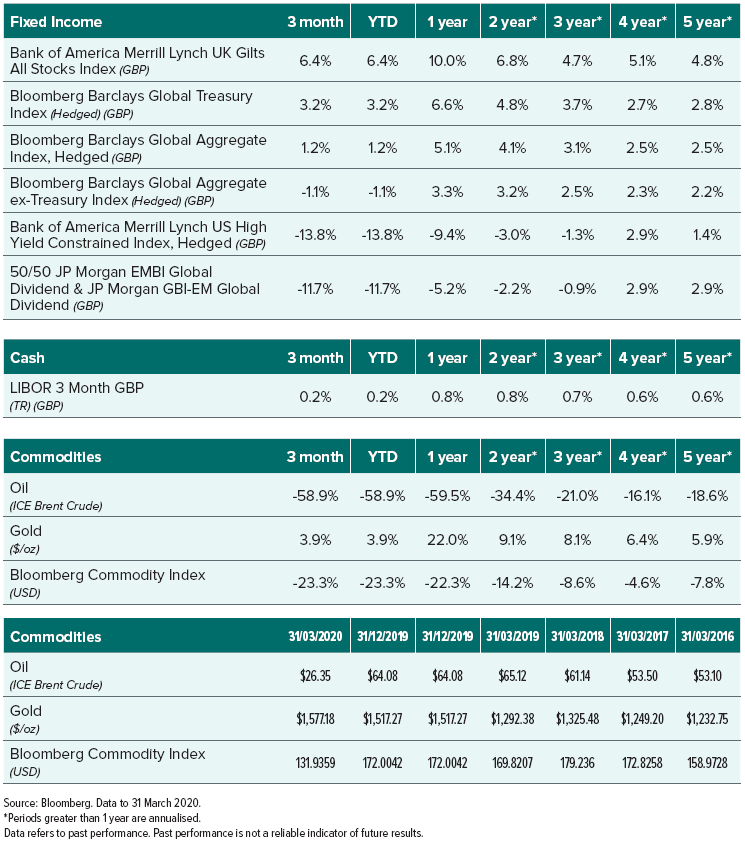

The quarter saw central banks cut their respective short term rates to near zero, while yields fell across the curve on concerns over long-term growth and the risk of deflation. As a consequence, developed market government bonds, led by the UK and US, were our best performing asset class (source: SEI).

By design, and given our focused on absolute loss, our portfolios have meaningful allocations to shorter duration fixed income securities that sit alongside longer duration assets. While this shorter duration exposure provided performance in line with expectations over the period, being less sensitive to falls in interest rates than some peers would have been a relative headwind for the strategies.

For the stability focused portfolios, the bulk, if not all, of their equity exposure is in the form of lower volatility equities. We believe that allocating to manage (lower) volatility equities allows our investors to experience similar returns but meaningfully lower risk than broad equity markets. The cost associated with this advantage is that, in order to harvest the benefits of managed volatility, the equity component of the stability focused funds can behave quite differently to that of market capitalisation-weighted benchmarks, including the potential for periods of large outperformance and underperformance.

Given the low beta nature of managed volatility, in general, we expect it to outperform in sharp equity market downturns – and this expectation has been met quite consistently throughout the funds’ lives.

In Q1 2020, however, managed volatility equities declined more than would be expected in such a sell-off. This was particularly evident during the most extreme down days, when defensive utilities dropped in-line with cyclical industrials and consumer discretionary sectors, indicating indiscriminate liquidation.

Unusually, but not uniquely, the market behaviour did not resemble a typical recessionary period. Sector performance was not split by defensives vs. cyclicals, but rather by stocks affected and unaffected by the lockdown measures (with supermarkets, communications, health-care associated products and technology being viewed as the relative beneficiaries).

This performance is also partly explained by the dramatic underperformance of mid and small cap stocks; managed volatility is diversified across the size spectrum, whereas a typical broad equity market index is concentrated in larger names. Markets can be risky and every crisis is different.

While we know that we can never guarantee that managed volatility will outperform in every downturn, we remain confident in its ability to deliver competitive long-term returns with lower risk than the overall market.

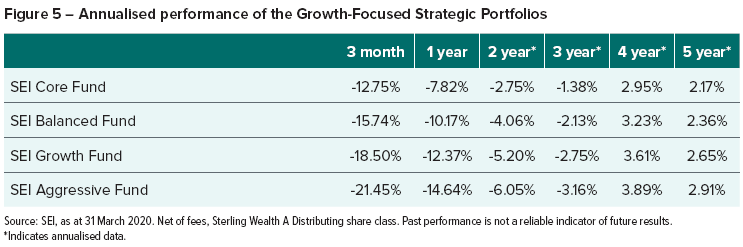

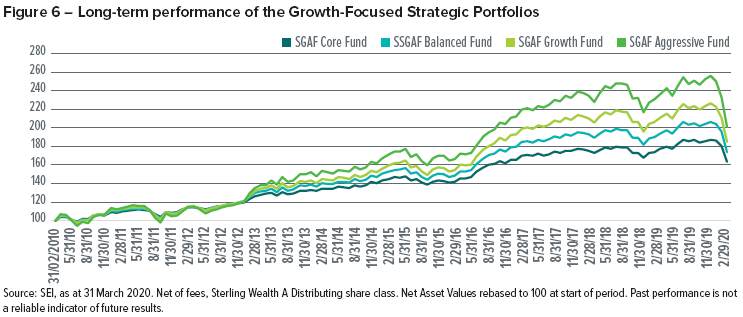

Growth Focused Funds

Performance

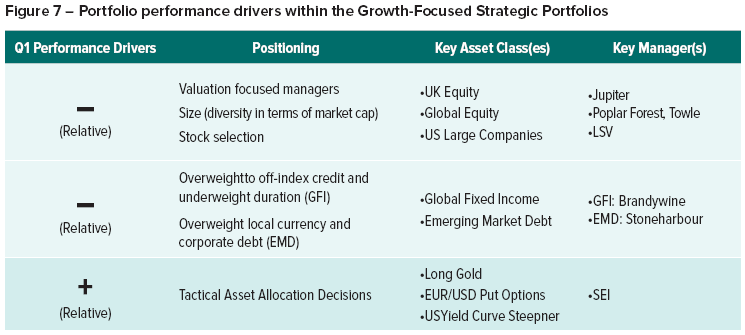

Portfolio Contributions

Portfolio Commentary

Despite an abrupt change in market direction this quarter, the drivers within equity markets remained broadly the same as the previous quarter. Investors continued to favour the largest stocks.

Diversity, the tendency for active managers to hold a more diversified portfolio than the market from a capitalisation point of view (and therefore underweight the mega cap stocks), was a strong negative theme for the quarter.

Looked at through a factor or alpha source lens, the more cyclical and economically sensitive stocks that underpin our Value alpha source underperformed, as banks and commodity stocks struggled. This was due to suddenly worsening economic conditions, interest rate cuts in the case of financials, and a surprise oil price war between Saudi Arabia and Russia that negatively impacted energy producers.

The lower risk, higher quality stocks that underpin our Stability alpha source outperformed. An increased appreciation for profitable cash-generative companies saw Quality companies outperform, helped by the overweight to healthcare and information technology companies which remain at the forefront of investor’s minds as we either work from home, shop online or are rightly concerned about health issues.

Finally, the relative performance of Momentum was mixed. Some areas of the market that were trending positively have fallen abruptly due to the crisis but, overall, a continuing trend of technology stocks and higher quality stocks outperforming, which had been captured by many managers, was supportive. In general though, extreme market volatility tends to be disruptive for trend following approaches.

Overall, the equity component of the Portfolios underperformed the market over the quarter. Our active managers’ tendency to underweight the largest capitalisation stocks was a key driver of this, as were an overweight to Value and subpar security selection by some of our underlying managers.

For the lower risk Core and Balanced portfolios, there is greater diversity in terms of the asset classes and strategies held. It was a difficult environment for both High yield and Emerging Market Debt which, on the back of substantial spread widening and highly illiquid market conditions.

On the alternatives front, the portfolios’ allocation to commodities serves to provide exposure to many of the main drivers of price increases and thereby offers a potentially valuable hedge against unexpected future inflation. The dramatic falls in global demand and inflation expectations, amplified by the oil price war between Saudi Arabia and Russia, saw steep falls across the commodity complex, further compounding results.

Defensive asset classes served our strategies well. The lower risk portfolios have a meaningful allocation to both UK and other developed government sovereign bond markets, which provided protection against the aggressive market falls over the quarter.

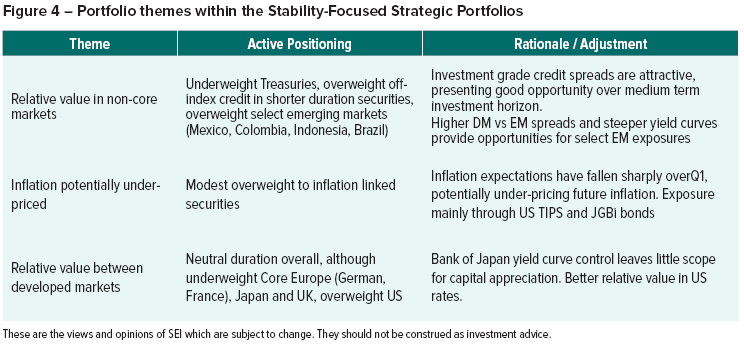

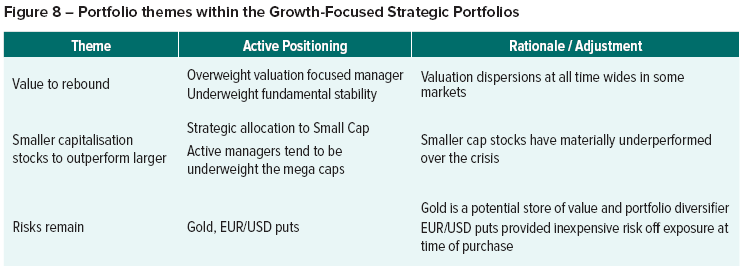

Asset allocation and Portfolio Positioning

From a strategic asset-allocation perspective, we continue to build portfolios that we believe are optimal for a wide range of market conditions and outcomes, including periods like the current one. Our portfolio construction focuses on diversification, aiming to deliver as diversified as possible a portfolio to all of our investors. We account for the inherent risks in capital markets, but also uncertainty or unknowns come with financial risk taking. Our aim is to build portfolios that are robust to a wide range of environments, and we are always on the lookout for ways in which diversification can be further improved.

From a tactical asset allocation perspective, we initiated two positions during the quarter within the Growth Focused Portfolios. Before the crisis took hold in global financial markets, we were able to take advantage of attractively priced EUR/USD put options, giving the portfolios protection against a fall in the euro against the US dollar for a historically low price.

And during March we added gold to the portfolios. In a world of coordinated, ever-increasing debt loads, we believe that gold will be viewed as a store of value. In addition, we feel this position has the potential to be an especially diversifying exposure for our clients in this environment of low-to-negative interest rates, increasing government debt loads and renewed economic stress.

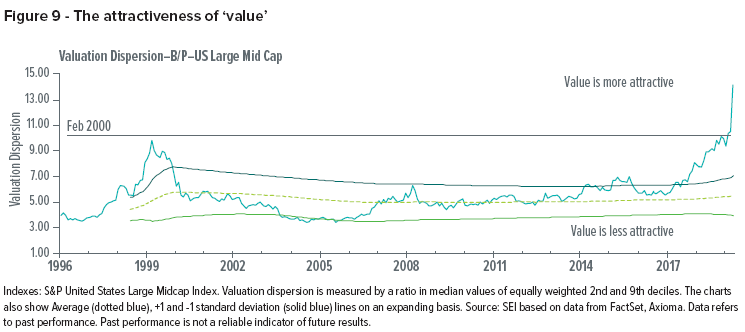

In fact, the gap between the most and least expensive areas of equity markets has become especially dramatic, and in some areas, it has surpassed the levels last seen during the tech bubble 20 years ago, a period that was followed by meaningful outperformance of value (especially small-cap value) stocks.

We also have a positive outlook for smaller capitalisation stocks and believe that active management will serve our portfolios well as the global economy eventually navigates its way through the current pandemic. While it’s impossible to predict when a turn will occur, the myriad emergency policy measures put into place by a large number of governments could prove quite stimulative once economies begin to reopen, and we would expect cheaper stocks and smaller companies to do well in such an environment.

Finally, our alpha source approach is implemented through active managers, whose stock selection is expected to deliver additional alpha over the long-term. Forced liquidation opens up opportunities for selection, which we expect our managers to capitalise on. Steep discounts are available in some areas due to some well-documented investor biases, such as avoidance of fundamentally healthy companies in troubled sectors like energy and airlines, or avoiding well-capitalised banks stocks as a result of anchoring to the 2008 global financial crisis.

Our managers constantly monitor and frequently review their holdings, and many have made what they believe are prudent changes to ensure they hold portfolios of likely survivors at attractive discounts to the overall market.

Global Market Performance

Representative market indices

IMPORTANT INFORMATION

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

SEI Investments (Europe) Limited acts as distributor of collective investment schemes which are authorised in Ireland pursuant to the UCITS regulations and which are collectively referred to as the “SEI Funds” in these materials. These umbrella funds are incorporated in Ireland as limited liability investment companies and are managed by SEI Investments Global Limited, an affiliate of the distributor. SEI Investments (Europe) Limited utilises the SEI funds in its asset management programme to create asset allocation strategies for its clients. Any reference in this document to any SEI funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI fund are reminded that any such application must be made solely on the basis of the information contained in the prospectus (which includes a schedule of fees and charges and maximum commission available).

The SEI Strategic Portfolios are a series of the SEI Funds and may invest in a combination of other SEI and Third-Party Funds as well as in additional manager pools based on asset classes. These manager pools are pools of assets from the respective Strategic Portfolio separately managed by Portfolio Managers, which are monitored by SEI. One cannot directly invest in these manager pools.

Past performance is not a reliable indicator of future results. Standardised performance is available upon request. All data is as at 31 March 2020.

Investments in SEI funds are generally medium to long-term investments. The value of an investment and any income from it can go down as well as up. Fluctuations or movements in exchange rates may cause the value of underlying international investments to go up or down. Investors may get back less than the original amount invested.

Asset class performance discussed is based on the majority SEI fund underlying the asset class. This does not include analysis of the manager pools, hedged share class investments within SEI Funds, additional SEI funds or any third-party funds within the Strategic Portfolios.

As a result, performance for the total asset class allocation may vary. Not all asset classes discussed are included in all Strategic Portfolios.

All asset class comparative performance is relative to the benchmark of the specific SEI fund representing the majority of the asset class investment. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the Funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

- The investment risks described below are not exhaustive and potential investors should carefully review the Prospectus prior to investing. The risks described below may apply to the underlying assets of the products into which the Strategic Portfolios invest.

- Investment in equity securities in general are subject to market risks that may cause their prices to fluctuate over time.

- Fixed Income securities are subject to credit risk and may also be subject to price volatility and may be sensitive to interest rate fluctuations.

- Absolute return investments utilise aggressive investment techniques which may increase the volatility of returns. If the correlation between absolute return investments and other asset classes within the fund increases, absolute return investments’ expected diversification benefits may be decreased.

In addition to the normal risks associated with investing, international investments may involve risk of capital loss from differences in generally accepted accounting principles or from economic or political instability in other nations. The Funds are denominated in one currency but may hold assets which are priced in other currencies. The performance of the Fund may therefore rise and fall as a result of exchange rate fluctuations. The Fund or some of its underlying assets may hold derivatives or borrow to invest. This can make the Fund more volatile and investors should expect above-average price increases or decreases.

The views and opinions shown in this brochure are of SEI only and are subject to change. They should not be construed as investment advice.

This information is approved, issued and distributed by SEI Investments (Europe) Limited, 1st Floor, Alphabeta 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. This document and its contents are directed only at advisers of regulated intermediaries in accordance with all applicable laws and regulations. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Simplified Prospectus and latest Annual or Interim Short Reports for more information. This information can be obtained by contacting your Financial Adviser or using the contact details shown.