SEI Manager Research: Solving the Fixed-Income Peer Group Problem

Performance is the most ubiquitous and common piece of information used to assess the success of an investment strategy. It is the litmus test for ascertaining skill and is the basis upon which most investors make decisions about whether to hire or fire a manager. In our view, however, it can also be deceptive, especially when there are thousands of investment products from which to choose.

One popular method of simplifying these decisions is to designate a peer group or universe to compare manager performance.

The problem

Off-the-shelf peer universes may seem to be the most convenient solution for comparing investment managers. However, in our view, they are not usually the most accurate way to assess relative performance. Assigning strategies to peer groups is not as simple as it sounds. Classifying a manager in the wrong peer group may lead to false conclusions about the manager’s skill—or even expectations of when the manager may perform well or struggle, which may lead to poorly-timed manager allocation decisions.

We see three main issues with using off-the-shelf peer groups.

First, most are often overly broad; a given group may have hundreds of managers who really are not very similar. We have observed significant deviations in key performance drivers between fixed-income managers’ durations, credit risks and sector exposures within the same peer group. Similar strategies from the same manager often populate a particular peer group, resulting in a double counting of the manager’s contribution to the universe. Another issue is that different vehicles (such as institutional composites, mutual funds, exchange-traded funds, closed-end funds, socially responsible funds and UCITs) often inhabit the same universe—but really should not, as each type has its own investment considerations.

Second, peer-group classifications may be based on return patterns or, in some cases, the manager’s own judgment or preferences, which leads to inconsistency.

Finally, a significant number of managers do not fit nicely or easily into traditional categories. Compounding this issue among fixed-income managers is the sheer number of available types of fixed-income securities, which may result in significant dispersions among a group of managers’ portfolios. Thus, managers may be categorized inappropriately in off-the-shelf databases, forcing comparisons that do not make sense.

How we solved it

We created custom peer universes with more rigorous parameters than off-the-shelf products from third-party providers to supply meaningful insights into a manager’s relative performance.

We began by including managers that have similar investment vehicles and performance reporting structures and eliminated similar products managed by the same firm. We then established tighter limits for each manager’s duration, credit beta and foreign exchange risk than those used in off-the-shelf peer universes by removing managers that we considered outliers relative to the existing peer group. This reduced the magnitude that these effects have on performance, while still providing enough latitude to account for managers that are more active in adjusting their risk profiles as fundamentals and valuations change.

This approach emphasizes managers with similar risk tolerances and characteristics. In our view, this is the soundest way to create peer groups because it reflects the decisions that are within a manager’s control, rather than relying on grouping managers with similar returns, which does not yield empirical consistency due to a lack of a common framework.

How our solution benefits our clients

Using our own peer groups—rather than the broader off-the-shelf peer groups—allows us to view the investment manager universe through a consistent risk lens, instead of a less-defined generic lens. As a result, our peer universes tend to be much narrower than off-the-shelf alternatives. The investment managers in each universe typically share similar risk attributes even if they have different investment styles. The result is a more robust universe of managers that, in our view, more accurately reflects the opportunities available to investors within each asset class.

Most of our custom peer universes contain a significant number of constituents; however, refining certain unconventional fixed-income universes led us to limit the number of similar managers. Still, we believe that a consistently defined universe should lead to more accurate performance comparisons than larger, more loosely defined or generic universes, as it is less influenced by market conditions that managers can’t always control.

Our custom peer groups aim to mitigate some of the inherent challenges within fixed-income benchmarks. For example, some sub-sectors of securitized fixed income—such as non-agency mortgage-backed securities, commercial mortgage-backed securities and asset-backed securities—that have evolved following the global financial crisis in 2008, have been widely adopted by fixed-income investment managers; however, traditional fixed-income benchmarks exclude significant portions of such instruments. Carefully constructed peer groups of similarly positioned managers can help overcome this limitation imposed by benchmarks. Municipal fixed-income benchmarks are also imperfect representations of a manager’s investable universe, and include bonds that are often unavailable for purchase (or that are overrepresented by select large issuers whose weightings can be quite volatile). Our peer groups aim to help level the playing field for municipal debt managers whose portfolio construction tends to differ greatly from commonly referenced benchmarks.

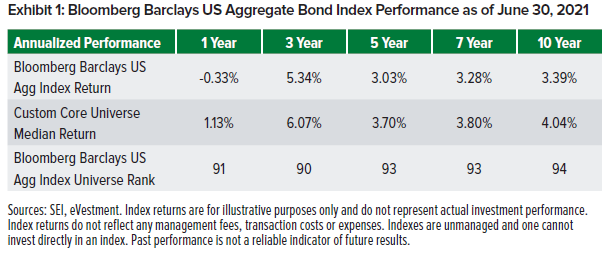

Investment managers within certain universes (such as U.S. core fixed income) tend to underweight U.S. government debt (both Treasurys and agencies) in favor of spread assets in order to generate a yield advantage without necessarily incurring significant additional credit risk. Over the long term, most active U.S. core fixed-income managers have outperformed the Bloomberg Barclays US Aggregate Bond Index (Exhibit 1). Thus, we believe conducting benchmark-relative analysis and using a carefully constructed peer group provides a solid basis for determining a manager’s true skill.

This approach also assists in distinguishing beta from alpha, which can be helpful in assessing appropriate fees to pay investment managers. Further, our peer-group work allows us to refine our due-diligence efforts, gaining efficiency in focusing on key aspects that matter most to the manager’s investment philosophy and process.

Finally, we believe our peer-universe framework enhances our understanding of the opportunity set available within each asset class. This not only furthers our ongoing analysis of current managers in our program, but also provides additional inputs for vetting new managers. Collectively, these insights can aid portfolio construction decisions.

Important Information

Information provided in the U.S. by SEI Investments Management Corporation, a federally registered investment adviser and wholly owned subsidiary of SEI Investments Company.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results. Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assume any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. Information provided in the U.S by SEI Investments Managements Corporation, a federally registered investment adviser and wholly owned subsidiary of SEI Investments Company. Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”). This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.