SEI—A Global Pioneer in Managed-Volatility Investing

Managed-volatility approaches to investing, which are based on a long history of empirical evidence, offer investors a compelling way to pursue stock-market-like returns with less volatility. We launched our implementation of this investment style in the US more than 15 years ago in 2004, and have since continued to innovate as managed volatility has evolved.

Brief history of an anomaly

The foundations of modern portfolio theory were first laid in the 1950s and 1960s. One of the core ideas in those early days was that the expected return on an investment should be commensurate with its risk, typically measured in terms of volatility. The idea was intuitive and straightforward: Investors should demand a greater return for holding an asset that has a more volatile (less predictable) pattern of returns.

However, in the ensuing decades, this assumption was subjected to intense scrutiny. Our proprietary analysis of real-world market data found that investorsgenerally appeared to systematically overpay for higher-volatility securities and underpay for lower-volatility ones. Said another way, returns on high-volatility stocks were notably lower than prevailing finance theories predicted, while returns on low-volatility stocks unexpectedly higher. This was a significant and surprising finding—seemingly an anomaly, in financial parlance—that weconfirmed in subsequent studies using data from other time periods and othermarkets as actually being quite typical. At SEI, we also saw a compelling upshot:An investor might be able to earn better-than-expected returns for a given level of risk.

SEI’s innovative, pioneering approach

As empirical evidence of this so-called anomaly continued to accumulate, the potential investment opportunity became apparent. In our view at SEI, by investing in a portfolio of lower-volatility stocks and avoiding those that are higher volatility, a portfolio manager should be able to improve the balance between risk and return. We seized upon this opportunity by launching the US version of our managed-volatility strategy on 28 October 2004.

In addition to being an early implementer, we also brought our manager-of-managers framework to the space. Among other things, this framework provides us with access to some of the best-in-class investment managers. It also allows us to diversify manager-specific risk and to tilt manager allocations in response to economic or market conditions. It additionally provides multiple levels of portfolio monitoring, from individual management firms to SEI’s portfolio managers and SEI’s Risk Management team. Our manager-of-managers expertise has enabled us to work closely with leading investment managers to test, build, implement and further develop our managed-volatility approach—and we have been pleased with the results.

In November 2006, we expanded our suite of managed-volatility solutions by launching the SGMF Global Managed Volatility Fund. SEI also offers tax-managed versions of both its US and international offerings. In a very real sense, SEI has helped pioneer the managed-volatility revolution.

The managed-volatility revolution

Our initial embrace of a managed-volatility approach required an interesting change of mindset. Traditional investment management focuses on a portfolio’s expected return relative to a benchmark; at the same time, it tries to limit the portfolio’s divergence from that benchmark. By doing so, a manager accepts that its portfolio will probably experience benchmark-like volatility. In contrast, when developing our managed-volatility approach, we focused directly on risk. Each of our managed-volatility offerings has a volatility-reduction target compared to its benchmark.

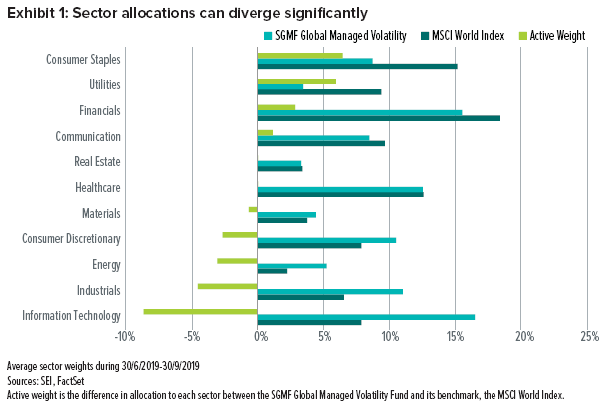

We determined that in order to achieve this objective, our managed-volatility strategies should be sector and industry agnostic. As a result, our sector allocations tend to differ significantly from the broader market. We often dramatically overweight less-volatile sectors and heavily underweight those that are more volatile. As Exhibit 1 shows, the average weights of certain sectors in the SGMF Global Managed Volatility Fund diverged substantially from their weights in the MSCI World Index during the third quarter of 2019. The Fund was overweight consumer staples, utilities and financials stocks, and underweight the information technology, industrials, energy and consumer discretionarysectors.

Over short periods of time, our sector-agnostic philosophy can lead to significant return disparities between a managed-volatility portfolio and its benchmark. However, over long periods, we expect returns to be similar to those of the broader stock market (of course, there is no guarantee this will be the case). It is important to note that shifts in sector and industry behaviour do occur. When we or one of our managers see this happening, we will adjust our portfolio accordingly. Our process is empirical and data-driven; we are neither wed to nor averse to certain sectors simply because they behaved a certain way in the past.

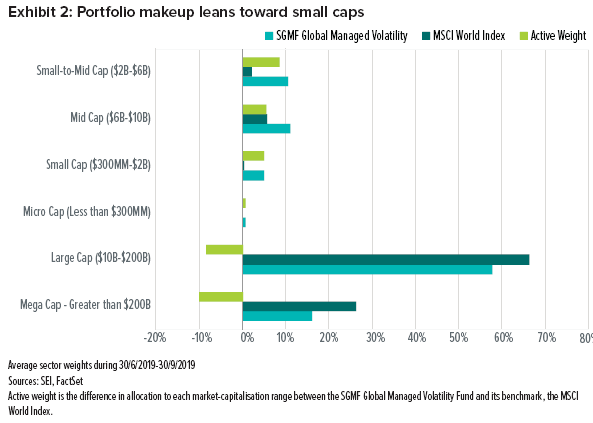

Differences between Fund and benchmark characteristics are further apparent in their distinct market-cap exposures, as one can be vastly different from the other. Over the quarter ending at 30 September 2019, the Fund was generally overweight smaller-cap stocks, while it maintained an underweight to mega-cap and large-cap names compared to its benchmark (Exhibit 2).

Solid performance with downside protection

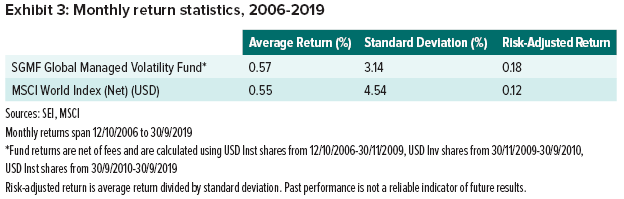

We have found that one of the historical benefits of a well-designed managed-volatility strategy is an improvement in risk-adjusted returns. Risk-adjusted returns, which can be calculated in different ways, are meant to show the return an investor receives per unit of risk assumed. (Risk is typically measured as the standard deviation, or average dispersion, of a portfolio’s returns.) All else equal, a higher risk-adjusted return indicates that a portfolio has struck a better balance between risk and reward.

As shown in Exhibit 3, the SGMF Global Managed Volatility Fund has done just that. Since the Fund’s inception on 12 October 2006, its average monthly return has been 0.57%—very similar to the average monthly returns on its benchmark, the MSCI World Index (Net) (USD). Our strategic focus is on the next two columns, however. The standard deviation of those returns was 3.14% for the Fund, which is about 31% lower than the standard deviation of its benchmark. This lower volatility also enhanced the Fund’s risk-adjusted returns. As shown in the last column of Exhibit 3, the return per unit of standard deviation was 0.18 for the Global Managed Volatility Fund. This is significantly higher than the 0.12 generated by the benchmark.

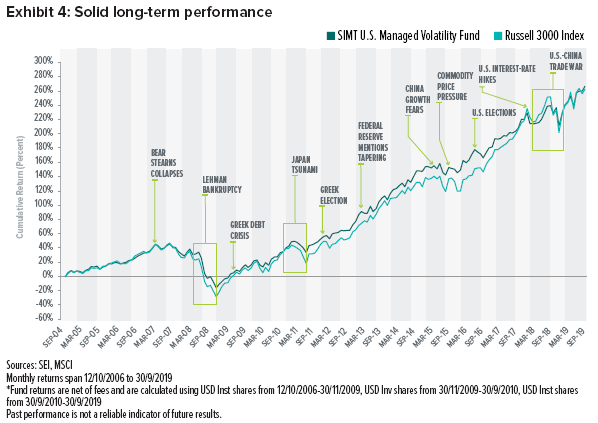

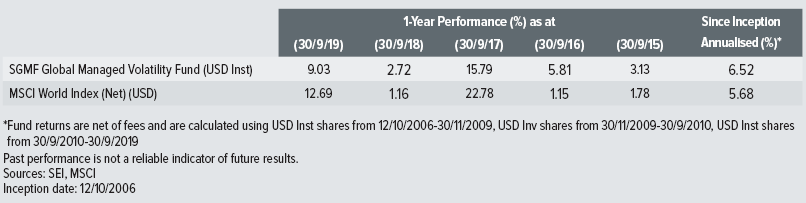

As implied by these return statistics, long-term performance has been solid, and this is shown in Exhibit 4. In fact, although a managed-volatility investor should not expect this to be the norm, the Global Managed Volatility Fund has managed to outpace its benchmark since its inception on a cumulative basis. This cumulative performance edge can be attributed, at least in part, to the fact that the Fund did not suffer as badly as its benchmark during the September 2007 to February 2009 bear market, the sharp mid-2011 correction, or the abrupt market decline in the fourth quarter of 2018. Since inception, in negative months for the MSCI World Index, the Fund and the benchmark have averaged -2.15% and -3.74%, respectively.

This potential downside protection is another appealing feature of a managed-volatility approach. Intuitively, if a portfolio is less volatile than the overall market, then it should typically lose less value during a steep market decline. This cannot be guaranteed, of course. But in the 2007-2009 bear market and the 2011 correction, the Fund’s maximum drawdowns were 16% and 12% less, respectively, than the MSCI World Index. More recently, during the fourth-quarter selloff in 2018 that saw many global indexes near bear-market territory, the Fund’s maximum drawdown was approximately 4% less than its benchmark.

We believe our low-volatility approach can serve investors well, helping to lessen the impact of market uncertainty. As always, we think it’s important that investors carefully consider all investment options and select investments based on their individual needs and goals.

Important Information

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The Global Managed Volatility fund is structured as an open-ended collective investment scheme and is authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The fund is managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, to provide general distribution services in relation to the fund. The Global Managed Volatility Fund may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

Past performance is not a reliable indicator of future results.

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.