SEI Forward

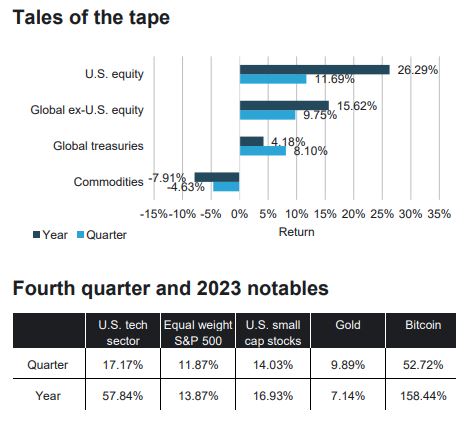

2023 went out on a high note as the global central bank interest-rate-tightening cycle was seemingly brought to a close with a dovish pivot from the U.S. Federal Reserve (Fed) and interest-rate-hike pauses from the European Central Bank and the Bank of England. The market was quick to celebrate as risk assets rallied, yields fell, and financial conditions eased substantially. This latest move higher is a fitting end to a wild year that witnessed aggressive monetary policy tightening through mid-year, a legitimate banking crisis, continued weakness in China, conflict in the Middle East, and, most recently, the rerouting of global shipping lanes and heightened tension in the Red Sea. Despite that laundry list of headwinds, global equities delivered solid returns, with the U.S. as a clear standout. A fever pitch of excitement over artificial intelligence and high expectations for interest rate cuts in 2024 were the key drivers of market performance.

Outlook: A healthy dose of skepticism

In many ways, we begin 2024 the same way we began 2023…with skepticism. Oh, let us count the ways! We remain skeptical that:

- Inflation will return to target levels, or below, in a sustainable way.

- Central banks will meaningfully cut interest rates in 2024—and even more skeptical that they will start cutting in March.

- Earnings will support lofty valuations, particularly with the largest of the large-capitalization stocks.

Much of our skepticism is a reaction to what appears to be the extreme confidence of the market itself:

- Equities are not just expected to deliver earnings growth in 2024 but double digit earnings growth.

- The Fed is expected to not just cut interest rates but to double the level of cuts projected by the policy makers themselves.

- Even more interesting is that these two scenarios are priced in simultaneously, which suggests the central bank will carry out multiple “normalization cuts” in reaction to falling inflation as opposed to “stimulus cuts” in reaction to a slowing economy.

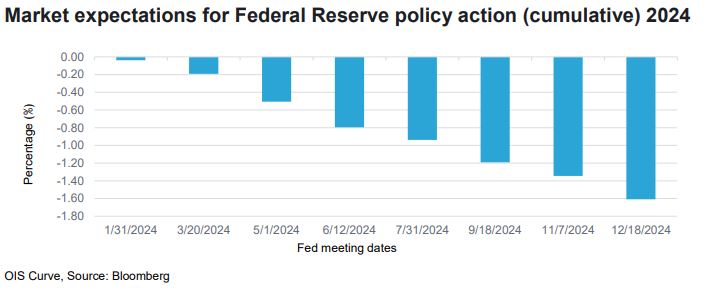

Unrealistic expectations

The U.S. Fed is projecting three 25-basis point reductions. Traders in the futures market are pricing in six cuts (1.50%) in the federal funds rate by the end of 2024, as shown below.

Somehow the “soft landing” label doesn’t quite capture the market’s expectations for 2024, which appears closer to perfection. Essentially, we are taking the other side of the perfection trade. We expect to see rate cuts more in line with the Fed’s projection than the market’s expectations.

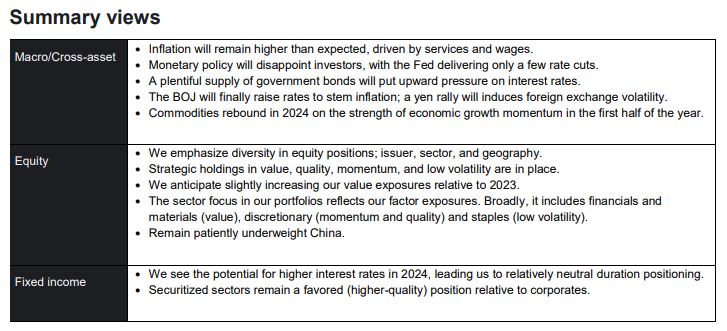

The equity rally into year-end may have legs into early 2024; however, we are more focused on diversity than directionality. The well documented outperformance of the “Magnificent 7” tech stocks relative to the broader market in 2023 failed to reappear in the fourth quarter even as interest rates declined. We see that trend continuing in 2024, as tech stock multiples look rich and vulnerable. Accordingly, we prefer a more diversified posture across equity exposure, including individual stocks, sectors and geographies.

The factor view: Quality, momentum, and value

Our core approach of favoring high quality companies with positive earnings momentum at reasonable values remains intact. We expect to emphasize value a bit more in 2024 based on historically wide spreads (the relative attractiveness of stocks representing high and low measures of value) and what we see as a supportive macro environment for the coming year. This includes our expectations for a market-disappointing number of developed market Central Bank rate cuts and elevated stock valuations, which can cause even strong earnings to disappoint market participants. Our factor exposures and manager stock selection currently leaves our portfolios leaning into financials and materials (given our preference for value), consumer discretionary (given our momentum and quality exposures), and consumer staples (from our low-volatility positioning).

What we’re watching

Outside of North America and Europe, one of the potentially big events of 2024 may be policy reversal from the Bank of Japan and the strengthening of the Japanese yen. Japanese policy makers have thus far resisted the pull of high inflation, refusing to abandon the zero bound (the policy interest rate has been below 0 for six years). We believe that will change early in 2024. This should result in a stronger currency, which may serve to increase volatility in the New Year as the cheap Japanese financing and carry trades start to unwind.

China was a disappointment throughout 2023, as the economy struggled under the weight of a bursting property bubble, equities continued to underperform, and stimulus measures failed to materialize. Despite relatively attractive valuations, we remain patiently underweight.

Regarding fixed income, interest rate volatility remains extremely high as developed market 10-year yields fell roughly 100 basis points from their October highs on perceived dovish turns from policy makers (particularly in the U.S.) Our top-down view has us shunning duration risk as we see the rally in yields as overdone based on our expectation that inflation will not settle below target for long and central bankers will not deliver on the expected number of rate cuts. In addition, we see basic supply and demand as being an underappreciated negative for the coming year. In short, deficits are rising despite the broadly positive economic performance of 2023 and debt issuance in 2024 will be heavy. We see more sellers than buyers as central bank are diversifying their holdings and the fourth-quarter rate rally (prices rose and interest rates fell) may have dampened investor’s appetites. From a bottom-up perspective, the interest-rate positioning in our portfolios remains modest and mixed around at index-like levels.

Credit markets look somewhat vulnerable in 2024 as yield spreads remain tight and early warning signs are appearing in the form of rising default levels. Our investment-grade portfolios remain defensively positioned by favoring the securitized sectors over corporate exposures. Our high-yield portfolios also maintain a somewhat defensive posture and continued to shed CCC rated issuers into the year-end rally.

Lastly, we maintain our favorable view of commodities on heightened geo-political risks, OPEC cuts and positive economic growth in the short term along with higher average inflation and the effects of structural underinvestment over the longer term.

In closing, we would like to wish everyone a healthy and happy 2024.

Indexes

U.S. equity=S&P 500 Index, Global ex-U.S. equity=MSCI ACWI ex-U.S. Index, Global treasuries=Bloomberg Global Treasury Index, Commodities=Bloomberg Commodity Index, U.S. tech sector=S&P 500 Information Technology Sector Index, Equal weight S&P 500=S&P 500 Equal Weight Index, U.S. small cap stocks=Russell 2000 Index, Gold=Bloomberg Gold Index, Bitcoin=Coinbase Bitcoin.

Important information

Index returns are for illustrative purposes only and do not represent actual investment performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

The opinions and views in this commentary are of SIEL only and are subject to change. They should not be construed as investment advice.

This information is issued by SEI Investments (Europe) Limited (SIEL) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority (FRN 191713).

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

SEI sources data directly from FactSet, Lipper, and BlackRock unless otherwise stated.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This document has not been registered by the Registrar of Companies in Hong Kong. In addition, this document may not be issued or possessed for the purposes of issue, whether in Hong Kong or elsewhere, and the Shares may not be disposed of to any person unless such person is outside Hong Kong, such person is a “professional investor” as defined in the Ordinance and any rules made under the Ordinance or as otherwise may be permitted by the Ordinance.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755- 1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This email and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.