SEI Forward

Tales of the tape (third quarter): U.S. equity -3.27%, Global ex-U.S. equity -3.77%, Global treasuries -4.17%, 10-year U.S.

Treasury yield +0.74% to 4.57%, Commodities +4.71%

Notables (third quarter): U.S. crude oil +28% to $90, U.S. Energy sector +12.22%, U.S. Technology sector -5.54%

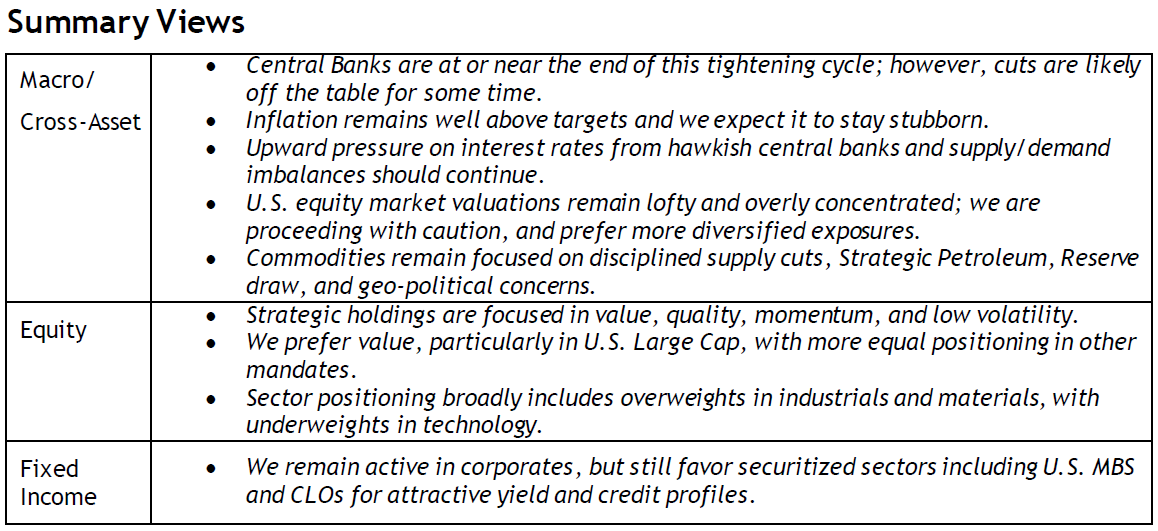

The story of the quarter was far and away the global rout in rates markets . We have been saying for some time now that we expect central bankers to remain hawkish keeping interest rates higher for longer—lingering supply and demand imbalances, combined with mixed, but positive leaning, economic news continue to support our view. Investors have seemingly come around to our way of thinking as Bloomberg data shows that bond yields reached multi-year highs this quarter. Further, policy makers—particularly in the U.S.—have successfully bullied markets into pushing out the potential timeline for any future rate cuts even as the tightening cycle approaches the finish line.

The 10-Year U.S. Treasury finished the quarter with the highest yield since 2007 (Bloomberg data). Looking more globally, the 10- Year German Bund reached a peak last seen in 2011, and even the 10-year Japanese Government Bond increased 0.37% to the highest level since 2013 (Bloomberg data). Despite the significant rise in interest rates and sentiment suggested that interest rates will continue to rise, inflation continues to run hot supported by crude oil prices. Saudi Arabia and Russia renewed commitments to production cuts leading to the biggest quarterly surge in oil prices since the start to the Russian/Ukraine conflict. Unsurprisingly, equity markets struggled with the potential reality of higher costs of capital and higher discounts rates for longer than anticipated challenged valuations.

In a word, our view is cautious.

Broadly, we expect that this unprecedented interest-rate hiking cycle will not be contained to the most interest-rate sensitive parts of the economy or the capital markets. We remain extremely skeptical that the 2% inflation targets of the past will be easily achieved in the future and, therefore, question the ability of central banks to quickly pivot towards more relaxed monetary policies. While we agree the global tightening cycle is nearing an end, we wouldn’t be surprised with another rate hike from the U.S. Federal Reserve and some movement towards tighter monetary policy out of the Bank of Japan. That said, the bond investors did central bankers a huge favor by tightening financial conditions by forcing lenders to pay higher yields on bonds, making additional interest rate hikes from policy makers essentially a coin flip at this point. Regardless, we do expect yields to stay at the higher end of the recent range as inflation proves perhaps a bit more stubborn than markets anticipate and the supply of new debt remains extremely high.

Looking beyond interest rates and inflation, the employment situation remains a bit of a double-edged sword—a strong jobs market should help consumption, but tightness adds wage pressures into the mix. The artificial intelligence boom—or perhaps bubble—has valuations at still lofty levels, particularly in the U.S. and specifically amongst the “Magnificent 7” technology stocks (Amazon, Apple, Google (Alphabet), Meta, Microsoft, Nvidia and Tesla) that have driven so much of the market’s gains recently . Meanwhile, credit spreads remain tight across the spectrum of investment-grade issues, reflecting a market trading a full valuations. The shocking expansion of armed conflict in the Middle East has further added to a growing list of concerns. Within equities, we remain positioned for weaker markets into year-end. Rather than chasing returns in the highly concentrated the U.S. large-cap market, we prefer a much more diversified posture and remain focused on our favored Quality, Momentum and Value alpha sources. More broadly, our positioning leaves us typically preferring Industrials across regions and capitalizations, while in the U.S. we are leaning into materials and financials, but spurning mega-cap technology, consumer discretionary and communication services. This also leaves our typical equity positioning with lower interest-rate sensitivity than the broader market, which was clearly on display in September.

Regarding fixed income, our portfolios have maintained a yield advantage without sacrificing credit quality. This was achieved primarily with overweights in the securitized sectors, such as mortgage-backed securities (MBS) and collateralized loan obligations (CLOs). Interest-rate positioning remains modest, but slightly long in the near term given the back up in yields.

Commodities rebounded during the quarter and remain a preferred position. While China stimulus continues to disappoint, the steadfast stance of OPEC+ regarding production cuts and the resurgence in geo-political tensions keeps us overweight this asset class into year end.

With our macro views broadly becoming more accepted by the market, we remain confident in our positioning to close out 2023.

Indexes

U.S. equity=S&P 500 Index, Global ex-U.S. equity=MSCI ACWI ex-U.S. Index, Global treasuries=Bloomberg Global Treasury Index, 10-year Treasurys=ICE BofA Current 10-year U.S. Treasury Index, Commodities=Bloomberg Commodity Index, U.S. crude oil=Brent Index, U.S. energy sector=S&P 500 Energy Sector Index, U.S. technology sector=S&P 500 Information Technology Sector Index

Important information

Index returns are for illustrative purposes only and do not represent actual investment performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorized and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.