SEI Forward.

Tales of the tape (second quarter): U.S. equity +8.74%, Global ex-U.S. equity +2.44%, Global treasuries -2.44%, U.S. 10-year U.S. Treasury yield 3.82%,

Commodities -2.56% Notables (second quarter): U.S. technology sector +17.20%, Equal-weight S&P +3.99%, China Equity -9.79%, Bitcoin +7.01%, Japanese yen/U.S. Dollar -7.9%

Despite a mixed bag of surprises, disappointments and capitulations, risk assets managed to rally further during the quarter as ChatGPT and the potential of an artificial intelligence (AI) revolution took hold of investors’ imaginations. This rising tide did not lift all boats equally—the newly minted “Magnificent 7” (Apple, Microsoft, Amazon, Nividia, Google, Tesla, and Meta) dominated market performance once again. The rest of the capital markets faced some headwinds, including yet another significant bank failure in the U.S., sticky global inflation, stubbornly hawkish Central Banks, further disappointment in the China rebound, and the complete and total capitulation on U.S. rate cut expectations this year. This laundry list left broader equity market returns more modest, boosted yields, and kept commodities under pressure.

Outlook

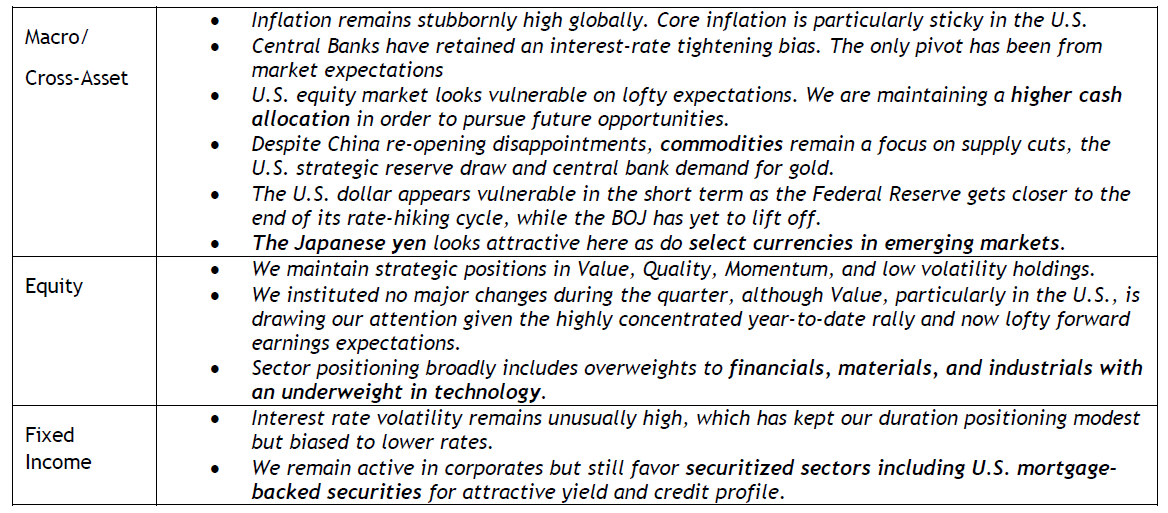

As we move forward into the second half of 2023 we remain broadly cautious. We see risks in elevated and concentrated equity market valuations, resolute central banks and the yet-to-be-fully-felt effects of interest rate normalization on economies, markets, corporations, and consumers. The AI boom for mega-cap technology stocks in the quarter certainly feels frothy as the forward price-to-earnings bar has now been set extremely high. We also expect yields to grind higher and eventually put additional pressure on growth stocks despite the second quarter rally coinciding with several central banks outside of the U.S. unexpectedly pivoting back to further rate hikes.

In addition, while we expect inflation to continue to moderate, we believe the path to normalization will still take longer than the market expects prompting central banks to maintain tighter policy for a longer period than is currently priced in. From a top down perspective, we maintain elevated cash levels relative to U.S. equities as we believe the second half of the year will be particularly challenging given current valuations and perhaps still too optimistic earnings expectations given our view of the macroeconomic backdrop.

Within equities, a diversified posture focused on Quality, Momentum, and Value remains our core approach. We see the significantly narrow leadership thus far in the equity markets as unsustainable and caution against performance chasing at these levels. Valuation spreads, representing the dispersion between “cheap” and “expensive” stocks, have given back some ground taken during 2022 yet our positioning remains broadly unchanged. From a sector perspective, we find value in financials and materials, remain focused on earnings momentum within industrials and continue to seek out quality exposure in health care.

Regarding fixed income, interest rate volatility remains historically high; therefore, our directional interest rate positioning remains modest with a slight bias for lower rates into year-end. Securitized sectors such as mortgage-backed securities remain a favorite in our investment-grade portfolios given attractive yields and high-quality credit profiles. Credit markets have participated in the recent risk rallies with investment-grade and high-yield spreads at the tightest levels of the year, thus we continue to take a more defensive posture. Broadly, the rise in absolute yields provides little incentive to stretch for extra basis

points in credit spreads.

Commodities remain a focus given shorter term catalysts such as potential China stimulus (despite significant disappointment this far), aggressive oil supply cuts from OPEC+ (the Organization of the Petroleum Exporting Countries and a group of other oil producers that includes Russia), and U.S. strategic petroleum reserve levels that have reached 40-year lows. Longer-term chronic underinvestment also remains a tailwind in this space. Lastly, we are biased for shorter term weakness in the U.S. dollar as global central bank hiking cycles begin to deviate. The Japanese yen (and Japanese short-term interest rates) look particularly interesting as the Bank of Japan (BOJ) has remained on the sidelines despite sharply higher inflation levels. We expect to see the beginning of the end of Japan’s extraordinarily easy monetary policy toward the end of 2023.

In closing, while 2023 has been a challenging year for our portfolios thus far, we believe our portfolios are well positioned going forward.

Summary Views

Indexes

U.S. equity=S&P 500 Index, Global ex-U.S. equity=MSCI ACWI ex-U.S. Index, Global treasuries=Bloomberg Global Treasury Index, 10-year Treasurys=ICE BofA Current 10-year U.S. Treasury Index, Commodities=Bloomberg Commodity Index, U.S. technology sector=S&P Information Technology Sector Index, Equal-weight S&P=S&P 500 Equal Weighted Index, China equity=MSCI China Index, Bitcoin and Japanese yet/U.S. dollar sourced from Bloomberg.

.

Important information

Index returns are for illustrative purposes only and do not represent actual investment performance. Index performance returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged, and one cannot invest directly in an index. Past performance does not guarantee future results.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorized and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.