Russian debt: Default drawing near?

The Russian government’s willingness to pay on its debt obligations is now explicitly in question following comments by the Putin regime, despite economic buffers put in place before the events of recent weeks.

Russia sits with a large current account surplus (meaning that the country is a net lender to the rest of the world) and deep international reserves suggested to be as large as $650 billion. 50% of these reserves are based in U.S. dollars, euros, or sterling and are held with western institutions, and with recently imposed sanctions, are now inaccessible.

Approximately 12% of the country’s reserves are in gold, which, while accessible, are not liquid. The remaining assets are either in rubles (which have devalued significantly) or Asian currencies (Chinese yuan being the largest holding). This accessibility problem changes the fundamental picture for “Fortress Russia” (the notion that Russia’s reserves would allow it to withstand Western sanctions) considerably.

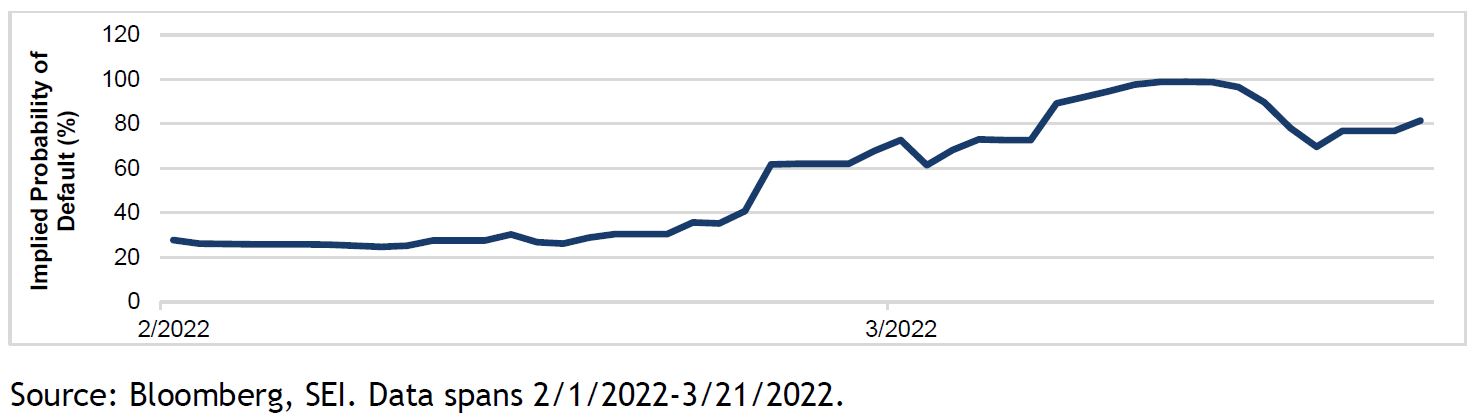

Possible Default

Market expectations (based on the pricing of credit default swaps) suggested an increasing probability of sovereign default of Russia’s hard-currency (generally U.S. dollar, euro, sterling, Japanese yen, and Swiss franc) obligations following the country’s invasion of Ukraine on February 24.

A coupon on a key Russian corporate (Gazprom) delivered a hard-currency coupon payment March 7, and the Russian oil corporate, Rosneft, delivered a principal payment on March 9. At the sovereign level, the next significant event occurred on March 16, when a hard-currency sovereign coupon was due. This payment was delivered on March 18 and was within the 30-day grace period given on most securities to deliver coupons. Russian President Putin previously signed a decree saying that creditors from “countries that engage in hostile activities” can only be paid interest and principal payments in Russian rubles. While there are Russian bonds that can deliver payment in both rubles and hard currency, an attempt to deliver the expected hard-currency payment in local currency would be deemed a default for this particular bond. It remains unclear whether Russia will attempt to deliver payment in rubles for future coupons.

The Asian Crises

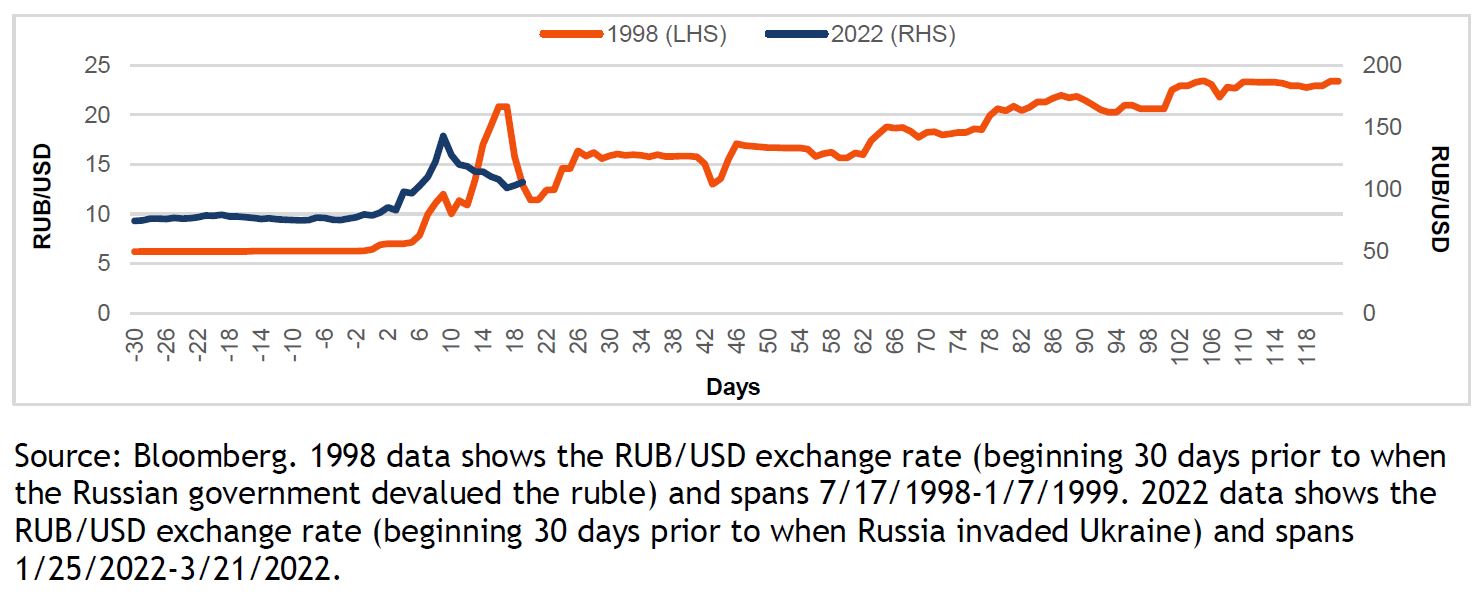

Russia’s previous debt default in 1998 followed the Asian crises in 1997, which contributed to lower energy consumption, a decline in oil prices, and a fall in the region’s trade with Russia. At the time, the ruble was a floating-peg currency (managed within an artificial range). In quick succession and unable to prop up its currency and meet debt obligations, Russia defaulted on its domestic debt and moved to a free-floating ruble.

A $20 billion financial package approved by the International Monetary Fund helped stabilize the Russian market at the time. Additionally, improving relations with the Paris Club (a group of officials from major creditor countries whose role is to find solutions to payment difficulties experienced by debtor countries) helped negotiate a rescheduling of old Soviet debt.

The interest payments remained burdensome, though they arguably would have been manageable were it not for externalities such as the Asia crises and decline in oil prices. It is unlikely the country would see similar support for its debt this time around.

Rating agencies often use the country of primary residence for corporations as a floor for rating corporate debt. This is particularly true when firm revenues are intertwined with the trade of that country for either domestic demand or its composition of exports. Several Russian state-owned and corporate entities have been sanctioned due to the nature of their business or ownership structure. These entities are most at-risk of receiving rating downgrades.

Glossary

Credit default swaps are financial agreements that insure the buyer of the swap against a debt default by the bond issuer.

Free-floating exchange rate refers to a currency exchange rate that is determined solely by supply and demand in the market.

Floating-peg exchange rate refers to a currency exchange rate that is fixed to a particular value but is allowed small fluctuations around that value.

Hard currency refers to currency issued by countries that are generally viewed as politically and economically stable.

International Monetary Fund refers a group of 190 countries with a primary purpose to foster stability within the system of exchange rates and international payments.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.