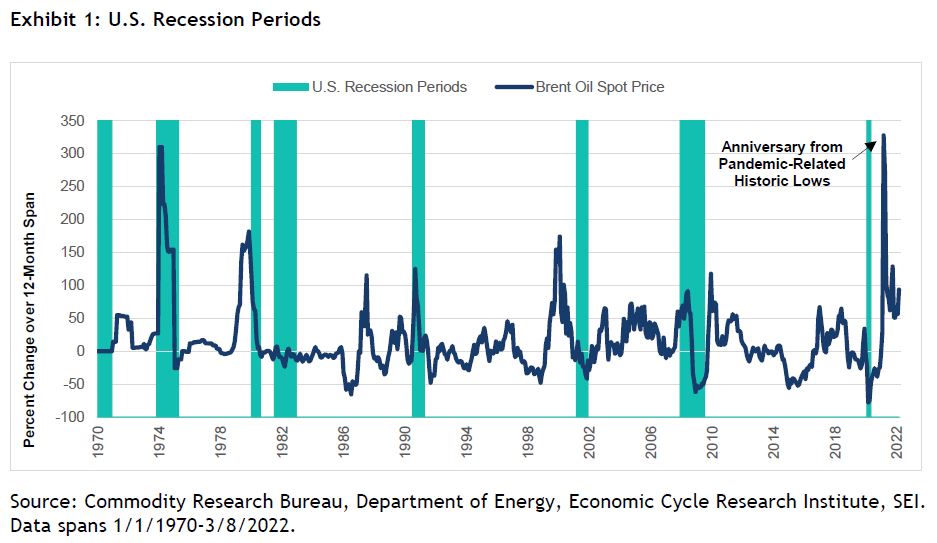

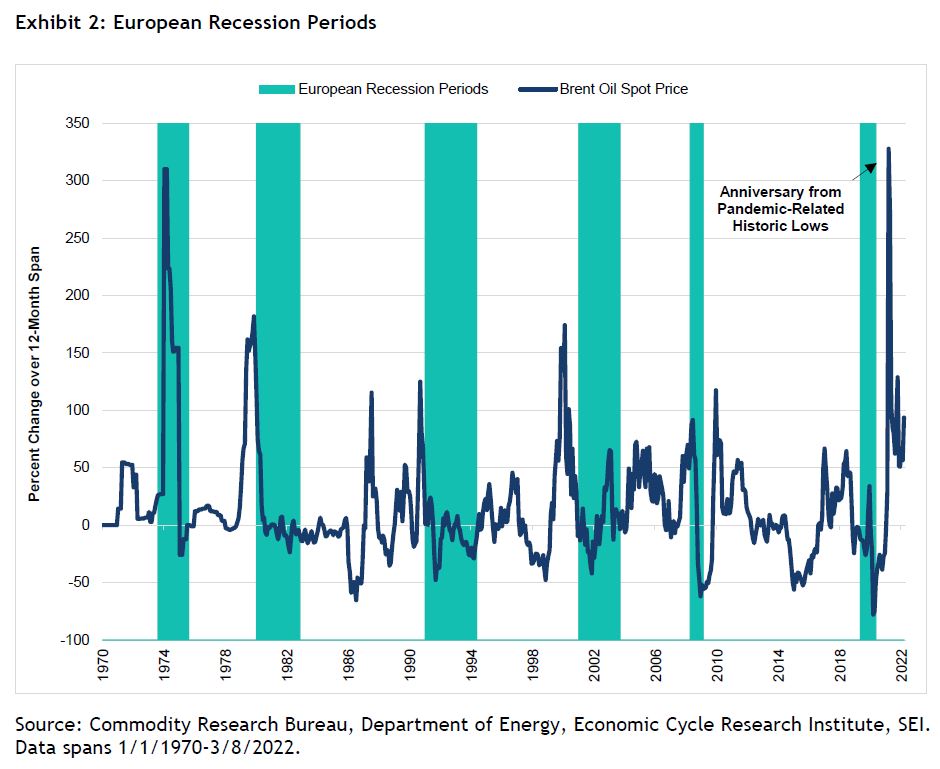

Risk of recession as oil prices rise?

Russia is the world’s largest oil exporter and the second-largest crude oil exporter1, and Ukraine is a key transit country for Russian exports to Europe2. For both countries, mineral fuels (coal, petroleum, and natural gas) are the largest export category. Despite a relatively small percent of Russian oil ex/supports reaching the U.S., the commodity is a global product. A lower global supply drives prices higher everywhere as countries that depend on the Russian supply chain look elsewhere to import. A large percent of the European Union’s total energy imports comes from Russia—close to 40% of its coal and refined petroleum, and around 25% of its crude oil and natural gas.

From the start of the invasion on February 24 through March 8, the price of crude oil rose over 30%—a gain of almost 100% for the previous 12 months according to Bloomberg. Despite retreating some over the last few days, an extended period of lower Russian supply could intensify the concern for higher prices.

We have also seen European natural gas prices return to their January 2022 highs, and pressures are likely to continue as hostilities in Ukraine persist. Natural gas prices in Europe were already soaring before the invasion. We saw a huge spike at the beginning of 2022 as alternative sources of energy failed to provide enough electricity to meet demand. Prices in the U.K. rose close to 10x from where they were in 2021, while prices in Europe were 7x higher.

Since Russia invaded Ukraine, areas that already faced high energy costs are now facing even more pressures as global sanctions against Russia—including a U.S. ban on Russian oil shipments—have resulted in one of the largest oil-supply disruptions since World War II.

This has happened before

The first major oil crisis was the Arab oil embargo that began in 1973. It was followed in 1979 when the Iranian Revolution triggered interruptions in oil exports from the Middle East. Those supply disruptions drove surges in oil prices that led to a global energy crisis. However, it’s hard to compare today’s price spikes to those that occurred in the 1970s. Energy intensity is now much lower than it was 50 years ago, while energy efficiency is much greater. There are also a larger number of alternative energy sources available today.

Recession is not a foregone conclusion

As Exhibits 1 and 2 show, while rising oil prices do not necessarily foreshadow recessions in the U.S. or Europe, oil price surges that happen over a relatively short period can shock an economy and cause a recession due to both the direct and indirect impacts of higher energy costs on households and businesses.

Direct impacts of higher energy costs:

- Households that have higher gas bills are left with less money in their budget to spend on other goods and services.

- Businesses that rely on fuel to operate (such as airlines, or those that must ship goods) face higher production expenses.

Indirect impacts:

- Businesses that want to reallocate capital and labor (for instance, auto manufacturers seeking to decrease production of sport utility vehicles in favor of fuel-efficient vehicles) may face costs and time delays—which, in aggregate, could result in lower overall demand and output in the short run.

- Uncertainty caused by surging oil prices may result in consumers pausing purchases of durable goods and firms delaying irreversible investments—the combination of which could lead to an economic slowdown.

- Despite growing inflation concerns, consumer spending appeared strong in the U.S. last year. However, the surge in energy prices from the invasion could force individuals to reduce discretionary spending as a result.

The world economy was showing solid momentum in growth before the recent price spike. Europe was coming out of pandemic lockdowns, while the U.S. economy had been recovering since the second half of 2020 and was expected to post above-average gains in the first quarter (although that estimate will likely come down given current energy and food spikes).

Even with oil prices climbing in the wake of Russia’s attack, households and businesses are generally still in good shape. This is especially true in the U.S., where there remains ample excess savings at the higher end of the income scale. Although gross domestic product growth is expected to slow, we maintain a relatively solid outlook for the world’s major economies.

Glossary

Recession refers to a period of economic decline and is generally defined by a drop in GDP over two successive quarters.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Diversification may not protect against market risk.

Bonds and bond funds will decrease in value as interest rates rise. High-yield bonds involve greater risks of default or downgrade and are more volatile than investment-grade securities, due to the speculative nature of their investments. Treasury Inflation Protected Securities can provide investors a hedge against inflation, as the inflation adjustment feature helps preserve the purchasing power of the investment. Because of this inflation adjustment feature, inflation protected bonds typically have lower yields than conventional fixed rate bonds. Commodity investments and derivatives may be more volatile and less liquid than direct investments in the underlying commodities themselves. Commodity-related equity returns can also be affected by the issuer’s financial structure or the performance of unrelated businesses.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to "institutional investors" pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to "relevant persons" pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission ("SFC")

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio

Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This commentary and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.