Risk Management: Asset Allocation

- Asset allocation can help investors reduce portfolio risk without sacrificing potential returns, or increase potential returns without introducing additional portfolio risk.

- Risks that are not diversifiable at the individual asset class level can be partially mitigated at the portfolio level through intelligent asset allocation.

- SEI is a pioneer of goals-based investing, which means that our portfolio construction philosophy and process extends beyond risk appetite and return targets to consider how a broad range of investors actually plan to use their portfolios.

What can Enlightenment-era cargo shipping conditions tell us about investing? Seafarers were the only game in town at the time for moving large volumes of cargo over long distances. But shipbuilding technology was not yet sufficient to prevent high incidences of shipwrecks, so losses at sea were a regular cost of business for suppliers.

Daniel Bernoulli, an 18th century mathematician, calculated that by splitting a large cargo shipment into smaller loads and sending them on separate ships, one could reduce the severity of potential losses.The greater the segmentation, the more effective the approach proved at minimizing losses, down to a quantifiable floor. Bernoulli even recognised his novel findings were applicable to “those who invest their fortunes in foreign bills of exchange and other hazardous enterprises.”

A Less-Hazardous Enterprise

Indeed, allocating capital in a diversified manner can reduce the potential severity of losses. The more optimal the diversification, the greater the potential risk-reduction benefit.

But diversification and asset allocation are invoked so frequently by investment managers that they can begin to sound hollow. Despite that, these powerful concepts should not be taken for granted, since they are the key to understanding risk management at the portfolio level.

We can think of diversification as a quality — an investor can attain various degrees of it. Revisiting our seaborne analogy, a supplier with a large cargo shipment split between two ships would be less diversified than a competitor whose similar-sized shipment was divided among a fleet of ten ships. Although the design and condition of the ships also needs to be considered, and not just in isolation; what challenges will the journey impose?

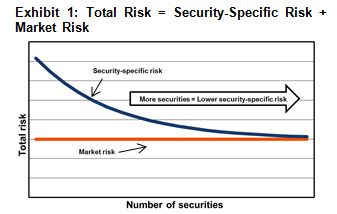

Diversification can be achieved within an individual asset class and across asset classes, although the risk management concerns differ somewhat at each level. For example, by allocating assets among a multitude of large U.S. company stocks as opposed to just a few, an investor can minimise the potential negative impact of company-specific risks on their U.S. large-cap allocation (and, by extension, the whole portfolio). Exhibit 1 depicts risk composition at the asset class level.

Diversification within individual asset classes can only go so far, however. An investor will still experience the overall volatility associated with a given asset class. Recessions, broad-based interest-rate changes, corporate-tax increases and other issues would affect most or all investments in an asset class.

At the portfolio level, diversification can be achieved by allocating among various asset classes. For example, rather than just investing in a 60/40 combination of U.S. stocks and bonds, an investor might also own international developed-market stocks, emerging-market stocks, investment-grade corporate bonds, high-yield bonds, and other asset classes.

What benefit can be derived from a broadened asset allocation?

Risks that are not diversifiable at the individual asset class level can be partially mitigated at the portfolio level, as long as asset classes respond in different ways to those risks. Different asset classes may exhibit different degrees or directions of sensitivity to certain risks. For example, bonds tend to be more sensitive to interest-rate changes than stocks, and the sensitivity is typically negative (bond prices tend to fall as interest rates rise). Asset allocation tries to diversify among a portfolio’s various sources of risk.

Ultimately asset allocation can help investors reduce portfolio risk without sacrificing potential returns, or increase potential returns without introducing additional portfolio risk.

Making Assumptions

There are two distinct steps in the development of our portfolio strategies, both of which are undertaken by SEI’s aptly named Portfolio Strategies Group (PSG).

We first establish capital market assumptions (CMAs) — asset-class-level projections for returns, risk (i.e. volatility of returns) and correlation. The inputs that PSG employs to generate these expectations will inevitably change over time, so our CMAs are subject to periodic reviews and updates.

The development of CMAs provides meaningful insight on the sensitivities of each asset class by demonstrating how we expect them to interact. Correlations tell us how one asset class might be expected to perform alongside another asset class, which is critical to portfolio construction.

Our correlation assumptions are purposefully conservative, as correlations between many asset classes will tend to rise during periods of market distress, causing a portfolio to be less diversified than expected when it counts the most.

And while asset-class return expectations are a necessary prerequisite to portfolio strategy development, we believe the investment portfolio deserves equal scrutiny under a risk-weighted lens.

Recall our 60/40 portfolio from earlier, with 60% of its capital committed to U.S. stocks and the remaining 40% to bonds. Rather than considering this portfolio in capital-weighting terms, let’s look at its risk-weighting.

Given that bonds are generally considered lower-risk investments relative to stocks, a dollar invested in bonds generally contributes far less risk to a total portfolio than a dollar invested in riskier assets such as stocks. The equity market risk associated with the 60% allocation to U.S. stocks would represent far more than 60% of the portfolio’s total risk.

Portfolio Optimization and More:

A Question of Balance

CMAs serve as the construction materials with which we build our portfolio strategies. PSG begins with a target return or risk level, and then seeks to create a portfolio with the optimal combination of asset classes to attain that target.

The traditional industry approach is to either maximise expected return for a given risk tolerance, or minimise expected risk for a desired rate of return. While we certainly incorporate this approach in portfolio construction efforts, we are also a pioneer of, and longstanding adherent to, goals-based investing. The next paper in this series will address the subject in detail, but with goals-based investing we essentially take a more nuanced view of risk and human behaviour.

We believe it is also important to strike a better balance among a portfolio’s overall sources of risk than traditional approaches to asset allocation tend to do, as plain vanilla stock and bond portfolios tend to be overexposed to certain risks and underexposed to others.

In short, if asset allocation is a balancing act, then our CMAs and optimization approach enable us to measure and target a suitable balance. Read Allocation the SEI Way for a more extensive look into our asset allocation philosophy and process.

Risk Management: Goals-based Investing

Our series on SEI’s approach to risk management will continue with a paper that explores the risk considerations inherent in developing goal-based investment strategies. We also plan to conclude this series over the coming months with a look at how SEI’s enterprise-level risk management capabilities

support our investment and portfolio management operations.

Glossary

Asset allocation: Asset allocation is the precise division of a portfolio between multiple asset classes, such as equities, fixed interest, liquidity and property.

Important Information

Past performance is not a guarantee of future performance.

Investments in SEI Funds are generally medium to long term investments. The value of an investment and any income from it can go down as well as up. Investors may not get back the original amount invested. Additionally, this investment may not be suitable for everyone. If you should have any

doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited (“SIEL”), 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Advisor or using the contact details shown above.

SIEL is the distributor of the SEI UCITS Funds and provides the distribution and placing agency services to the Funds by appointment from the manager of the Funds, namely SEI Investments Global, Limited, a company incorporated in Ireland (“SIGL”). SIGL has in turn appointed SEI Investments Management Corporation ("SIMC"), a US corporation organised under the laws of Delaware and overseen by the US federal securities regulator, as investment adviser to the Funds. SIMC provides investment management and advisory services to the Funds. SIEL, SIGL and SIMC are wholly owned subsidiaries of SEI Investments Company.