Rising Rates and Bond Markets: Keep Calm and Clip On

Pent-up demand from households and businesses, bolstered by historic levels of fiscal and monetary accommodation, should make for a historically robust economic recovery in the coming quarters as the global economy continues to recover from COVID-19. This could push global bond yields meaningfully higher. Because bond prices move inversely to yields, some fixed-income investors are understandably concerned about the possibility of falling bond prices. While seeing a price decline can be disconcerting, we believe investment-grade bonds should continue to provide important diversification benefits for investment portfolios and positive returns over both intermediate and longer time horizons (even in the unlikely case of a longstanding move to significantly higher bond yields).

Why Own Bonds?

With interest rates so low, some investors are asking whether there is still a role for core, investment-grade bonds in a diversified portfolio. We believe there is. First, bonds can provide meaningful income generation. While the current income received from bonds is quite low compared to history, we believe the relationship to cash and implied returns on riskier assets are within reason as compared to those of the last 25 years. In other words, we think that the current level of core bond yields are justified given everything else in the current state of financial markets.

Second, bonds still provide valuable diversification benefits. Because the returns on high-quality bonds tend to behave differently than the returns on riskier, growth-oriented assets like stocks, they can help lower the volatility of an overall portfolio. In other words, in an optimal investment portfolio, some assets should rise when other assets fall—which is often what happens in the relationship between stock and investment-grade bonds . Bonds can reduce portfolio volatility and serve a role as a deflationary hedge when stocks might suffer to a larger extent than the corresponding “rise” in purchasing power.

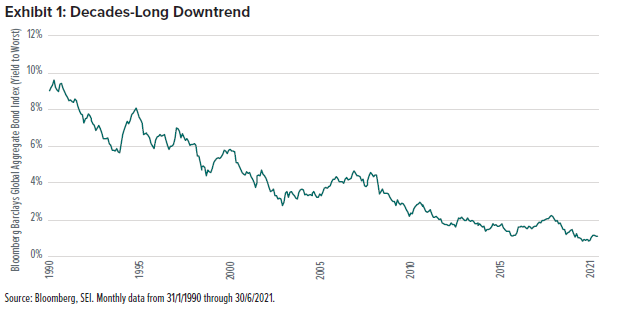

A Multi-Decade Tailwind

A nearly four-decade-long downtrend in global interest rates, as shown in Exhibit 1, has provided a longstanding boost to bond returns. Thus, the more interesting (and perhaps pressing) question is how serious the risk of higher interest rates is to future returns on investors’ bond holdings.

The broad downtrend in global rates continued into mid-2020, falling to record lows in many countries as the global pandemic took hold. Interest rates have since moved higher, thanks to the stronger growth and inflation outlooks fostered by forceful policy measures and the arrival of effective vaccines. Interest rates have modestly fallen as of late, but there are significant expectations of rising rates in the future.

Prices Matter, But Cash Flows Matter More

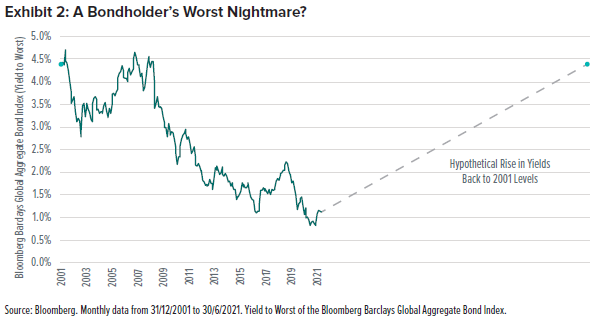

To help investors observe this risk, we examined the components of global bond returns over the last 20 years. We then analysed what returns might look like if we saw the last two decades of falling interest rates reverse course over the next 20 years (Exhibit 2). Interestingly, the additional boost to core bond returns from rising bond prices (falling interest rates) was just over one-tenth of the total annualized return on the Bloomberg Barclays Global Aggregate Bond Index. While that’s not insignificant, it does highlight that scheduled interest payments are a far more important factor in bond returns.

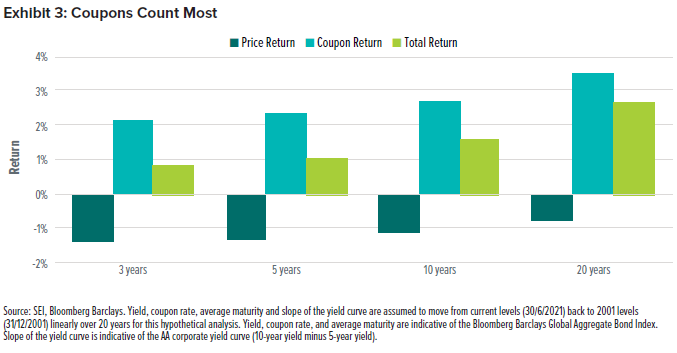

Courtesy of those recurring interest payments, simulated bond returns on the same index would still likely be positive even if interest rates reversed course in a straight line for the next 20 years. As shown in Exhibit 3, the impact of rising interest rates on bond prices would impose a small drag on overall returns, but the benefits of reinvesting cash flows into higher-yielding bonds over time could easily overcome this.

Active portfolio management helps automate the reinvestment of principal from maturing bonds into new bonds at higher coupons during rising-rate environments. So while investors might need to “reinvest” the coupons to achieve the total return in this example, the bond fund they own or the laddered-bond strategy they employ will still reinvest principal and may be able to offer higher coupon rates (higher income generation potential) during a rising-rate environment.

The Takeaway: Hold onto Your Bonds

To reiterate, SEI does not expect bond yields to retrace the decline of the last 20+ years. However, we hope the foregoing analysis will help investors keep their cool next time the risk of higher interest rates comes into focus. Investment-grade bonds should not only be able to produce positive returns in a multiyear period of rising interest rates, but they should continue to provide valuable diversification and income benefits as well.

Glossary

Active portfolio management is an investment strategy that attempts to outperform an investment benchmark index or target return.

Fiscal policy refers to the use of government spending and tax policies to influence economic conditions.

Hedge is a financial instrument or investment strategy that attempts to offset to risk of adverse price movements in a portfolio.

Monetary policy refers to the actions undertaken by a country’s central bank to control money supply and promote economic growth.

Yield is the amount that a bond pays each year in interest as a percent of its current price.

Yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating.

Index Definitions

Bloomberg Barclays Global Aggregate Bond Index measures the return of the global, investment-grade debt market.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.