Revisiting Value Investing: A Behavioural Finance Perspective

It’s easy to overlook long-term benefits when faced with shorter-term drawbacks. In fact, we’re all cognitively hardwired to think this way. There’s a direct relationship between the behaviours that arise from this line of thinking and value investing opportunities.

The market factors that drive factor investment strategies are all rooted in behavioural biases. At the overall market level, biased behaviour accumulates into inefficiencies that persist over time. Factors can go through periods in and out of favour, but their payoffs are clearly visible with a long-term perspective.

Value: A Well-Known Quantity

The logic underlying the value factor has a high profile and impressive academic pedigree. Benjamin Graham and David Dodd—widely considered the fathers of this approach—published a book in 1934 (well before the invention of big data) that documented the benefits of investing in the value asset class1.

Years later, armed with computing power, academics Eugene Fama and Kenneth French (in 1992)2, as well as Josef Lakonishok, Andrei Shleifer and Robert Vishny (in 1994)3 documented strong long-term returns for value securities in the US and many other countries around the world.

Still, this wealth of academic evidence did little to deter most investors in the late 1990s from piling into internet stocks with no earnings and zero book values.

1Graham, Benjamin, and David L. Dodd. Security Analysis: Principles and Technique. McGraw-Hill Book Company, Inc., New York and London, 1934.

2Fama, Eugene, and Kenneth R. French. The Cross-Section of Expected Stock Returns. 1992.

3Lakonishok, J., Shleifer, A., & Vishny, R. Contrarian Investment, Extrapolation, and Risk. 1994.

Behavioural biases can punish investors

Based on behavioural finance—a field of study that SEI helped pioneer, which continues to influence our thinking today—we believe that emotion-based investing can ultimately lead to weakened performance. In our view, exposure to the value asset class can help investors avoid mistakes driven by behavioural biases that include (but are not limited to):

Recency bias: Investors’ tendency to remember items that appear at the end of a long list of complex data rather than recalling those that appeared earlier. Of the many examples demonstrated throughout the history of financial markets, the last prominent episode of recency bias took place in early 2000. After four years of US equities reaching new highs on a raging bull market in technology, media and telecommunications stocks, investors (professional and amateur alike) continued to invest as if the stocks that soared during the tech bubble of the 1990s would continue to rise unabated despite the experiences of past boom-and-bust cycles. As we know now, this was not the case.

Loss aversion: Investors’ tendency to overreact to stressful market events with excessive caution—putting a higher priority on avoiding losses than on seeking gains (or avoiding losses altogether)—thereby giving up on the opportunity to benefit from an eventual market rebound. During the COVID-19 pandemic, for example, investors who fled the plummeting retail or transportation sectors out of loss aversion also abandoned potential earnings once these deeply discounted securities ultimately recover.

Over-extrapolation: Investors’ tendency to arrive at a long-term conclusion based on limited or select data points. Historical examples include some investors presuming in the 1980s that dominant oil producers would remain among the world’s biggest companies forever, and believing in the 2000s that large banks would remain strong for the foreseeable future. More recently, mega-cap technology stocks have appeared to expand without competition, regulation, or the need to deliver earnings.

Behavioural science tells us that these biases are generally amplified in times of greater market uncertainty, and particularly for stocks that might be hard to value. When the outlook is uncertain, as in the COVID-19 pandemic environment, investors can be more likely to act on emotion and lock into those behavioural mistakes.

A time-tested strategy

Value investing is a time-tested, viable strategy that history has shown can help investors avoid some of these behavioural biases, using an objective approach. Value investors don’t have to rely on unique, unknown or unrecognisable metrics and can intuitively understand why buying cheap can be better than buying expensive. The methodology can be verified with conviction that is not overly influenced by behavioural bias.

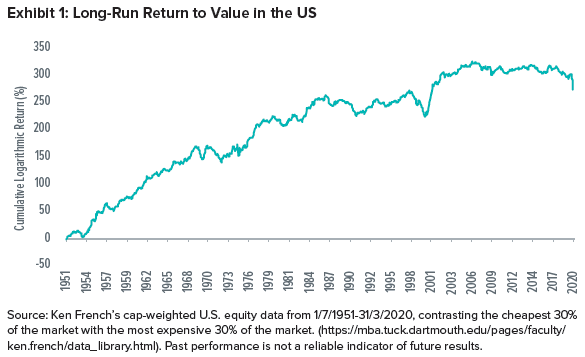

Exhibit 1 illustrates the long-term benefit of value investing. The blue line represents the relative performance of a portfolio that holds the cheapest one-third of US equities compared to a portfolio of the most expensive one-third of US equities. Over a period of nearly 70 years, the value investor’s portfolio of least-expensive stocks was the clear winner.

This is not to say the value portfolio outperformed every year, or even every three or five years. Its drawdowns are quite obvious when looking at the chart, particularly the more dramatic dips of the 1986-to-1987 period and the 1999-to-2000 tech bubble. Thus far, 2020 has also been a clear standout from what has been a long-term benefit of buying cheap and selling expensive.

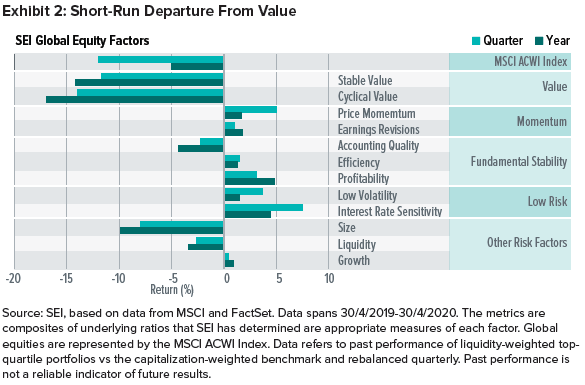

In Exhibit 2, we take a closer look at performance in the current environment, zeroing in on alpha sources and factors that are typically associated with long-term positive returns. It’s clear that value has significantly underperformed each of them as well as the overall market over the past year.

Of course, there are biases at play as pandemic-related uncertainty mounts and questions multiply: What if airlines or small businesses do not get bailed out or receive enough stimulus funding from the government? What if the lockdown continues for longer than expected? Even the possibility of such events creates enormous opportunity in the long run; in the short term, though, price declines in these sectors are self-fulfilling.

Just as fear drove consumers to stockpile certain goods like toilet paper and flour, stripping the supermarket shelves bare, we have seen investors rapidly run from risk and toward the comfort of securities that have outperformed over the last year—over-extrapolating—causing cheaper names with lower price-to-earnings to lag.

Such a pullback in value stocks does not mean that investors should abandon the asset class. Imagine an apple orchard that just had a fruitless season brought by frost or drought; the orchard would not be thereby deemed useless for future seasons. Similarly, we think it’s important to remain invested in value stocks even as they experience a fruitless period amid unstable market conditions. Economic life, like the life of an apple orchard, is measured in decades rather than months or even years. As value investors, we see periods of decline as rife with opportunity to invest in the steeply discounted stocks that were discarded by fearful investors, and then harvest them for years to come.

How cheap is cheap?

While value investing represents a solid long-term approach, we also believe the current environment presents a short-term opportunity to purchase historically cheap securities.

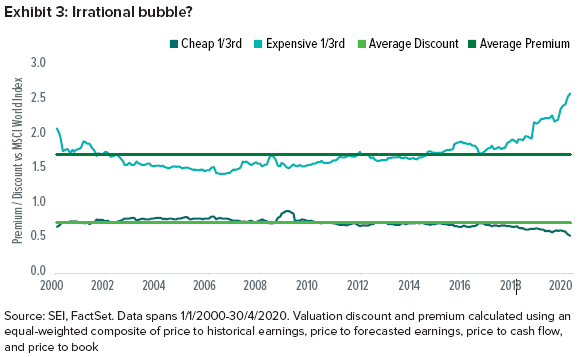

As illustrated in Exhibit 3, the most expensive third of the MSCI World Index is about 2.6 times more expensive than the rest of the market as at 30 April 2020; however, this group is also trading at about a 90% premium to its historical expensiveness.

On the other hand, value stocks—represented here by the cheapest third of the market—are trading at about a 20% discount to historical cheapness and a 46% discount to the rest of the market as at 30 April 2020. In our view, this is an example of short-term uncertainty amplifying behavioural biases.

We believe that investors can fight behavioural biases by remembering that long-term relationships usually hold up for good reason. For example, the relationship between a firm’s cash flow and stock price should not vary by large degrees for long periods of time. Eventually, history shows it will more likely revert toward the mean. It’s up to investors to decide whether the market turmoil we face today is truly different this time. We don’t believe that is the case.

Important Information

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.