The Return of Reflation: Time to Move?

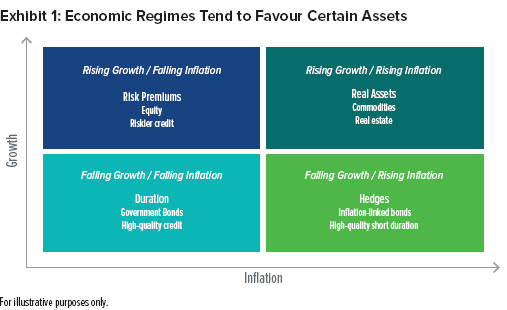

Recent chatter about “reflation” may have some investors wondering just what reflation means. In economic terms, reflation refers to inflation rising from a below-average level back toward its long-term trend. At SEI, we typically view reflationary periods as economic regimes where both growth and inflation are accelerating. Exhibit 1 provides a model framework that highlights asset performance during various environments, with a reflationary environment shown in the top right quadrant. In such as environment, we would expect real assets like commodities and real estate to perform well. There are some important nuances to consider, however.

About those nuances…

The framework is stylised, a term that describes a simplified model of reality. This has some important implications. First, it is rare than any given investment environment lands squarely in just one quadrant, as economic growth and price inflation trends are naturally volatile. Second, many factors beyond growth and inflation—such as valuations, regulatory changes, investment product innovations and investor behaviours—can impact relative asset class performance.

As a result, individual asset or sub-asset classes might be better thought of as “orbiting” one or more economic regimes. Gold, for example, has not fit neatly into the real assets quadrant in recent months, as the precious metal has exhibited real asset, hedge and duration characteristics at different times since mid-summer. Similarly, while value stocks typically fall into the risk premiums quadrant, we believe they are likely to do well if stronger growth is accompanied by higher (not runaway) inflation.

Most importantly, we do not believe investors should try to broadly tailor a long-term (strategic) portfolio to any specific growth/inflation environment. Rather, we use this framework to help design strategic portfolios that incorporate a variety of diverse asset class exposures in order to help investors manage/mitigate the downside effects of different market environments on their portfolios.

A smart approach to active asset allocation

There are times it might be prudent to tilt a portfolio’s strategic allocations toward assets that are expected to do well given a compelling view of the economic outlook; of course, this should be done within the constraints of an investor’s risk budget, which defines how much performance divergence one is willing to accept from the expected behaviour of the strategic portfolio allocation. In other words, you may wish to consider deviating from your long-term plan if you are uncomfortable with short-term risk.

For investors in model portfolios that offer active asset allocation, SEI believes we may be now at a point where such a tilt makes sense, given our view that the US is likely to see stronger growth and higher inflation (accompanied by a weaker US dollar) once the world economy is able to move beyond the COVID-19 pandemic. We understand that the outlook is still challenging in the near term, with worsening infection rates, vaccine distribution challenges, new variants of the virus, political uncertainties, and below-trend economic activity. Despite the near-term challenges, we believe the markets will mostly continue to look ahead to better times in the latter part of 2021.

Supporting evidence

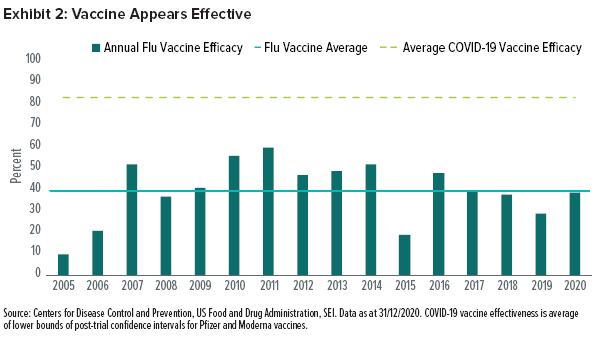

We believe the evidence for this view is compelling on several fronts, including the COVID-19 pandemic, economic policies, and recent market behaviour. On the pandemic front, in addition to more effective therapeutic regimens, we have seen the development of multiple vaccines that appear to be quite effective. As Exhibit 2 shows, reported efficacy rates for multiple coronavirus vaccines are higher than the historic effectiveness of annual influenza vaccines in the US (although it should be noted that the real-world effectiveness of vaccines tends to be somewhat lower than efficacy estimates from clinical trials).

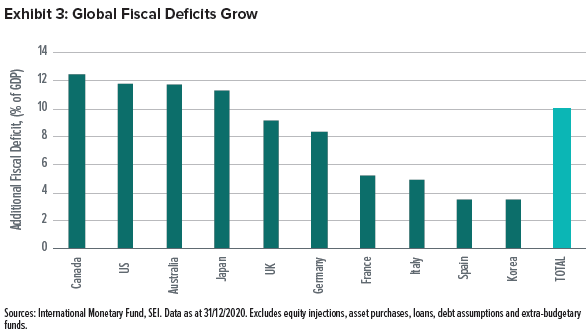

We have also seen policymakers respond to the pandemic with levels of fiscal and monetary support that are unprecedented in the last 60 years (Exhibit 3).

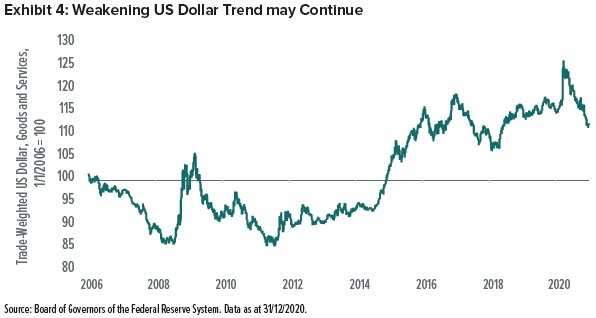

Additional fiscal support has been provided or is forthcoming in multiple countries, and central bankers in advanced economies have clearly signalled their intentions to allow inflation to run a bit higher than average to support a return to full employment. We believe the US dollar’s current weakening trend (Exhibit 4) could still have a ways to go (these cycles have historically unfolded over 6-to-10 years), which should also support faster global growth and stronger inflation.

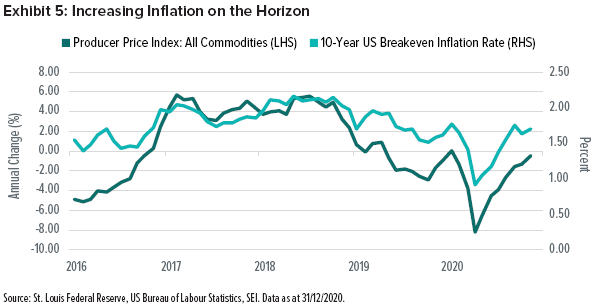

Finally, financial markets seem to be largely in agreement with this view, judging not only by US dollar performance but also by a historically strong small-cap equity market in recent months, as well as a steady rise in inflation breakevens and firming commodity prices (Exhibit 5).

Relevant positioning

In the SGMF Dynamic Asset Allocation Fund, we have expressed this view by implementing long positions in an equally-weighted S&P 500 Index, non-US developed market equities (MSCI EAFE Index), commodities (Bloomberg Commodity Index), and 10-year US inflation breakevens. Two options positions—on a steeper US Treasury yield curve and on a higher US 30-year Treasury yield—should benefit if our reflationary view unfolds as we expect. While the Fund’s existing long position in gold would often be considered a reflationary asset, it has behaved somewhat differently in recent months, perhaps because markets have had to gradually digest the new highs in gold prices that were set in late July and early August.

Risks to the reflation view

The main risks to our broad reflationary view and active allocation positioning include negative surprises on the vaccine front, an unexpectedly severe worsening (or lengthening) of the pandemic, tighter-than-expected fiscal or monetary policies, and a significantly stronger US dollar. The certain uncertainty created by unanticipated events is one of the reasons we believe so strongly in the principles of diversification. The COVID-19 pandemic, which would have been almost impossible to expect just over a year ago, is a powerful reminder of the uncertainties that can sometimes wreak havoc on economies, financial markets and investment portfolios.

Glossary

Duration is a measure of a security’s price sensitivity to changes in interest rates. Specifically, duration measures the potential change in value of a bond that would result from a 1% change in interest rates. Short duration bonds are less price-sensitive to changes in interest rates.

US Treasury yield curve represents differences in yields across a range of maturities of US Treasury bonds. A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the yields are closer together.

Index Definitions

Bloomberg Commodity Index tracks prices of futures contracts on physical commodities on the commodity markets. The index is designed to minimize concentration in any one commodity or sector.

MSCI EAFE Index is an unmanaged, market-capitalization-weighted equity index that represents developed markets outside North America.

S&P 500 Index is a market-capitalization-weighted index that consists of approximately 500 publicly-traded large US companies. The index is considered representative of the broad US stock market.

S&P 500 Equal Weight Index is the equal-weight version of the S&P 500 Index. It includes the same stocks as the S&P 500 Index, but each company is allocated a fixed weight of 0.2% of the index total (instead of a weighting based on market capitalization) at each quarterly rebalance.

Important Information

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

For full details of all of the risks applicable to our funds, please refer to the fund’s Prospectus. Please contact your fund adviser (South Africa contact details provided above) for this information.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.