Recession fears recede (Long Version)

Economists never die—they just get revised away. So do their recession forecasts. While predictions of a downturn in business activity during 2023 have been widely held since the end of last year, the U.S. economy has mostly surprised to the upside. Recession calls are now in the minority, with the latest plane analogy going from “hard landing” to “soft landing,” and even to “no landing.”

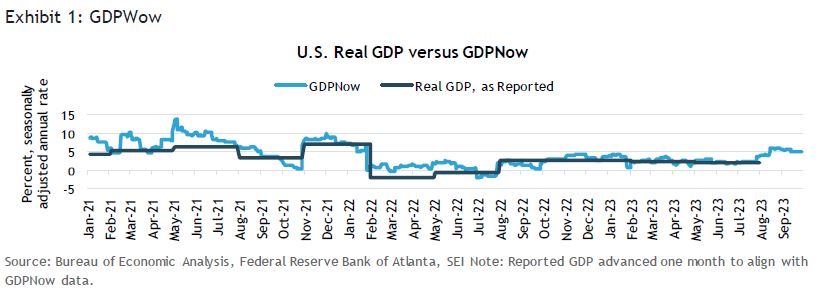

As shown in Exhibit 1, the Atlanta Federal Reserve’s running total of the quarterly change in inflation-adjusted gross domestic product (GDP) soared briefly to an annualized increase of 5.9% in August (the most recent Atlanta Fed reading remains a lofty 4.9%, with September data yet to be reported). Strong July results for retail sales, services consumption, industrial production and housing starts were the drivers behind the acceleration in growth. However, we believe the data overstate the underlying strength of the economy.

July’s retail sales, for example, were boosted by Amazon’s Prime Days event. Industrial production was skewed by a huge rise in utility output in July (a performance repeated in August) owing to the torrid heat in the southern and western regions of the U.S. Residential investment, meanwhile, held up remarkably well despite the highest mortgage rates since 2001; the lack of existing home inventory forced buyers to opt for newly constructed housing, which builders are downsizing in an effort to provide more affordable options. And, as far as services consumption is concerned, one can thank Taylor Swift, Beyoncé, and Barbie for measurably stoking ticket sales for concerts and movies, thereby contributing an estimated 0.7 and 0.5 percentage points to third quarter nominal consumption growth and GDP, respectively.

Nothing new

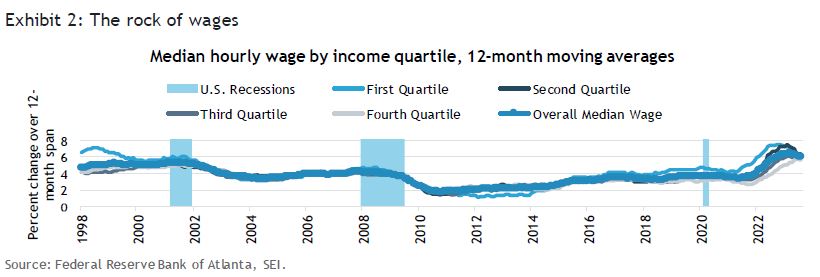

While others saw a recession just around the corner, it has been our view since the start of this year that the U.S. economy would display a fair degree of resiliency, led by robust consumer spending (high inflation and lagging inflation-adjusted incomes notwithstanding). We argued that the emergency-COVID payments to households, which led to a big build-up excess savings, were still being drawn down. To be sure, the remaining excess savings are now concentrated in households at the upper end of the income scale, with the bottom half pretty much tapped out. The latter cohort, however, still enjoys the benefit of a tight labor market. Wages at the lower end of the income spectrum actually kept pace with inflation during the early part of this year and now appear to be exceeding the rise in the cost of living. As illustrated in Exhibit 2, wage gains have faded for the lowest-paid employees (the first and second quartiles), but still were rising at a 12-month moving average in excess of 6% as of August.

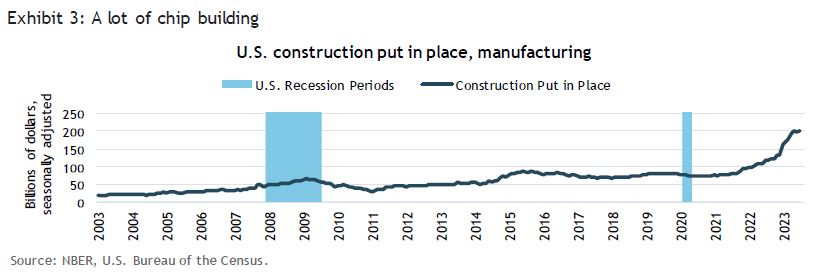

Companies also have benefitted from extraordinary federal government largesse. In addition to COVID-related support provided in 2020 and 2021, the administration of President Joe Biden and the U.S. Congress provided huge subsidies and incentives via the Infrastructure Investment and Jobs Act, passed in November 2021, as well as the Chips and Science Act and the Inflation Reduction Act, both of which were enacted in August 2022. Companies have responded to the incentives with gusto. Exhibit 3, for example, highlights the stunning 79% rise in manufacturing construction over the 12-month period ending in June. The uptrend began in earnest even before the latter two bills became law, perhaps reflecting the return of some manufacturing capacity to the U.S. in response to supply-chain disruptions abroad.

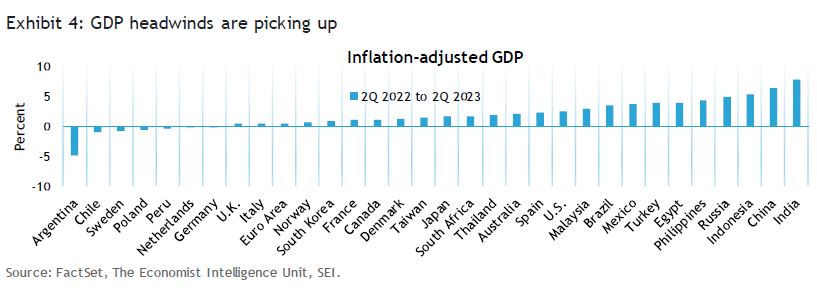

Outside the U.S., most other economies also continued to advance during the first half of 2023, although signs of stress and strain are now accumulating. One can see in Exhibit 4 that several countries have already recorded a contraction in GDP on a year-over-year basis through the second quarter of this year. This group includes Germany and the Netherlands; both economies have been dinged by the global slowdown in goods demand and the disruptions caused by the spike in energy prices through the summer of last year. The Euro area overall managed to eke out a 0.5% gain in real GDP in the four quarters through June. As is the case with the U.K., however, the outlook for Europe has turned distinctly gloomier. Both businesses and consumers are being pressured by still-rising interest rates and core inflation rates that remain quite sticky.

Some of the biggest declines in GDP can be found in the usual countries; Latin America. Argentina, Chile, and Peru all have recorded economic contractions during the past year. Political tumult, currency instability, and the decline in the price of metals and other commodities are to blame. By contrast, Mexico has been one of the better-performing Latin American countries thanks to its proximity to the U.S. and the free-trade agreement it shares with both the U.S and Canada.

The populous Asian economies, led by India and China, were among the best-performing economies during the third quarter of this year. The 6.3% jump in China’s GDP, however, is deceptively flattering because it reflects the move out of COVID lockdown at the start of the year. During the second quarter, the sequential gain from the first quarter totaled a very disappointing annualized rate of 3.2%. The third quarter will likely show an even slower pace of improvement. Indeed, as has been widely noted in the financial media, China’s youth unemployment rate is no longer being reported by the government following its rise to 21.3% in June.

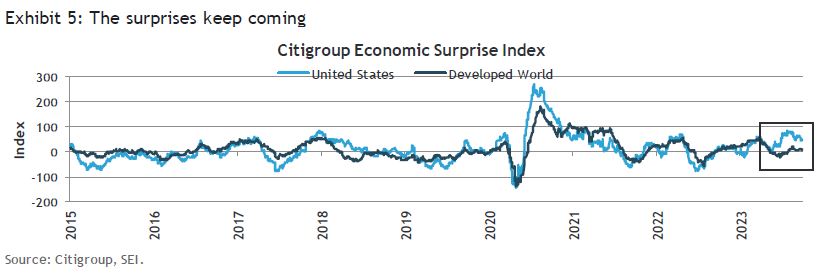

Among the advanced economies, the U.S. has separated itself from the pack over the past few months. Citigroup’s Economic Surprise Index (ESI), highlighted in Exhibit 5, shows a big jump for the U.S. since May. While other countries also have registered an uptick in positive data surprises, they have not been nearly as significant. Nonetheless, market participants historically have adjusted their expectations quickly. Even if the U.S. shows continued signs of economic buoyancy relative to other countries and regions, we believe that the extent of the surprises are likely to ebb. They could even turn negative as we approach the end of the year.

The squeeze is on

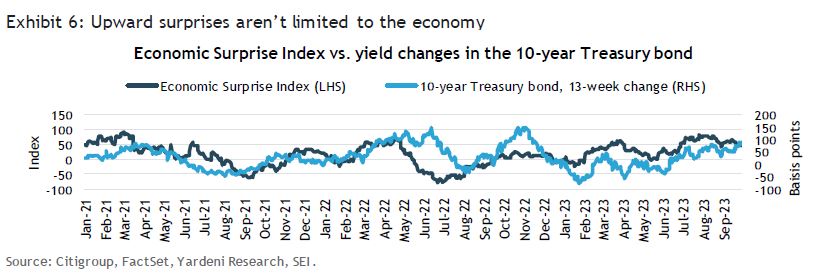

The biggest surprise of the past quarter, in our view, was the jump in bond yields in the U.S. and in other major countries, even as inflation rates across most geographies have turned lower. In the U.S., the upside economic surprises registered in recent months certainly have played a role. Exhibit 6 tracks the short-term (13-week) change in the U.S. 10-year Treasury bond versus the weekly movements in the Citigroup Economic Surprise Index. When the economic statistics show surprising strength, the yield on the 10-year Treasury bond tends to firm. Conversely, data that fall short of expectations often lead to declining yields. The logic is simple: U.S. Federal Reserve’s (Fed) policy decisions are heavily data dependent, especially under the tenure of Chairman Jerome Powell. Therefore, investors also are data dependent and can be expected to respond to every little twist and turn that deviates from expectations. Since hitting a closing low of 3.29% on April 5, the yield on the benchmark 10-year U.S. Treasury note has risen by more than 1.2 percentage points. The yield on the two-year Treasury note, which is even more sensitive to shifting market expectations, has jumped nearly 1.3 percentage points over the same span.

The correlation in Exhibit 6, however, is more directional than quantitative. It does not provide much information regarding how high or low yields will go in response to the flow of economic data, and provides little clue regarding where bond yields might be in a few months, much less over the course of the next five or ten years. More importantly, this relationship is very short-term in nature. As we previously noted, markets tend to adjust quickly to data surprises.

We still expect global economic growth to decelerate, leading to a mild recession in 2024, accompanied by a modest rise in unemployment in both the U.S. and other major developed countries. Although economists have mostly shifted away from their recession calls, we remain skeptical that the Fed can truly attain a soft landing. Inflation is proving to be tougher to tame than the central bankers had anticipated. This has forced the Fed and other central banks to keep increasing interest rates up to levels far higher than they themselves expected. Even as the current cycle of rising rates appears to be drawing to an end, traders and other market participants are now pricing in more fully a prolonged period of elevated interest rates that is much closer to our view.

In their most recent Summary of Economic Projections, released on September 20, the Federal Open Market Committee (FOMC) members revised their federal-funds rate forecast for 2024, eliminating two of the four interest rate cuts they had previously penciled in. The median forecast for the federal-funds rate at the end of next year is now 5.1%. To be sure, hope springs eternal at the Fed. Chairman Powell and his colleagues still expect core inflation to ease to 2.5% next year and 2% by 2026. As a result of this anticipated progress, the FOMC still sees the federal-funds rate falling to 2.9% by the end of 2026, from the today’s range of 5.25%-to-5.5%. Given their track record, we would view these projections as aspirational only.

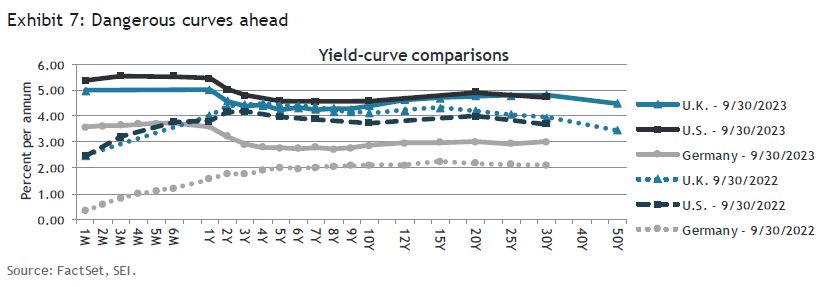

Exhibit 7 tracks the government yield curves of the U.S., the U.K., and Germany, highlighting how they have all shifted higher since the same period last year. Shorter maturities have risen dramatically in all three countries. The increase in yields in the center and at the longer end of the curves is less extraordinary, but significant nonetheless. Whereas the U.S. yield curve was already inverted from one year out this time last year, all three countries now are experiencing inverted curves.

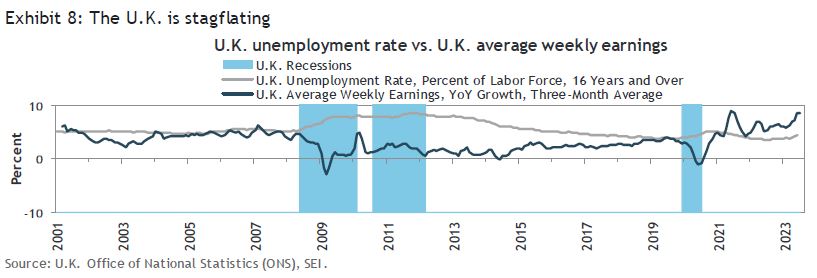

It has taken a while, but this extraordinary shift in the structure of interest rates is slowly squeezing the major economies. As we previously noted, Germany is already in recession. The U.K., meanwhile, is suffering a severe bout of stagflation, recording a decline in overall inflation-adjusted GDP in the month of July. Exhibit 8 reveals that the unemployment rate in the U.K. rose to 4.3% as of July, after hitting an all-time low of 3.5% in July 2022. Growth in average weekly wages, however, continues to run at an alarmingly high rate. The year-over-year change in average weekly wages totaled 8.5% as of July, which will likely keep inflation at elevated levels relative to other advanced countries in the months ahead.

Meanwhile, the latest purchasing managers’ index (PMI) reports for the major advanced countries were rather disappointing. Manufacturing industries have been weak for some time, but services–especially outside the U.S.–now appear to be weakening sharply, too.

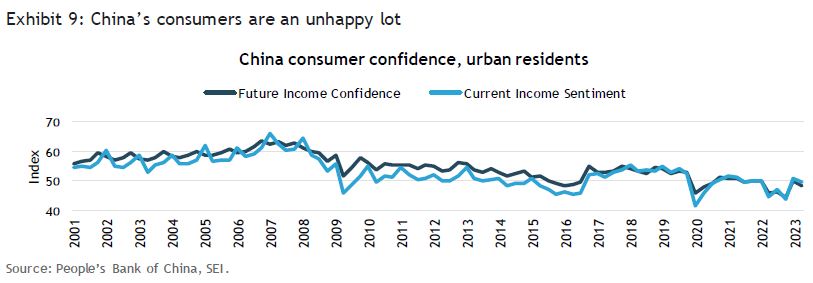

Hopes that a rebounding China, the second-largest economy in the world after the U.S. according to data from the World Bank, would offset slowing growth elsewhere have proved to be forlorn. Although domestic travel and services consumption in China has experienced a nice rebound from last year’s COVID lockdowns, the economic data still have been mostly disappointing. Economic surprises are still negative. Consumer sentiment also remains extremely depressed, as shown in Exhibit 9. The latest quarterly reading, as of June, partially reversed the jump spurred by the surprise easing of draconian COVID lockdown rules at the start of this year.

While consumer sentiment readings have been volatile, tracking the progression of COVID, Chinese urban households have become increasingly despondent since the Global Financial Crisis (GFC) of 2008. In the past two quarters, confidence regarding future income has been tracking below current income sentiment. This has rarely happened in the 22 years that these data have been published by the People’s Bank of China. Even in the years immediately following the GFC, consumers consistently believed that the future would be better than the present. The level of confidence expressed by Chinese consumers about the future has only been at lower levels during the COVID lockdown periods and in the first quarter of 2016 (there was a ferocious bear market in the Chinese equities in 2015 and a deep, two-year slide in the currency against the U.S. dollar).

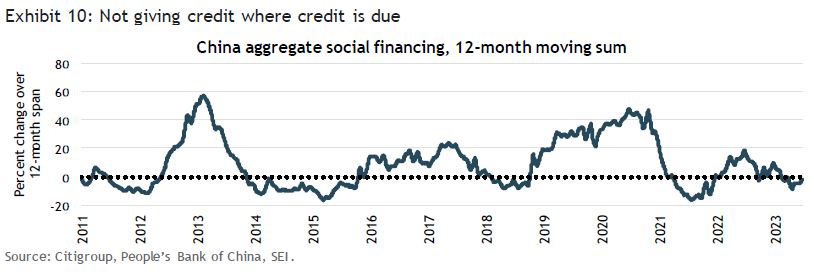

Neither Chinese consumers nor financial-market participants have been impressed by the government’s efforts to turn the economy around. There has been a variety of measures, both fiscal and monetary, initiated this year aimed at supporting the country’s property markets, real estate developers, and provincial governments. Banks are being encouraged to lend more and on easier terms, but loan demand is weak. Total aggregate social financing, highlighted in Exhibit 10, recently has fallen into negative territory.

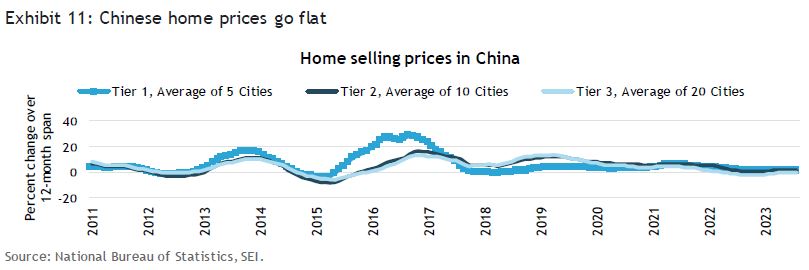

China could be facing several years of subpar economic growth. Property markets remain mostly moribund. Housing prices, highlighted in Exhibit 11, are quite subdued. Selling prices in the Tier 3 cities that are located in the country’s interior away from the most densely populated areas, have been registering an outright decline for more than two years. But even the five largest cities that make up the Tier 1 grouping are exhibiting little or no home price appreciation. This is a major issue because so much of the country’s household wealth is tied up in property. According to one study examining the level, distribution and composition of household wealth in China, nearly 70% of Chinese urban household wealth is invested in housing1. The percentage is even higher in big cities, like Beijing and Shanghai, reaching nearly 80% of total wealth.

China is enduring a balance-sheet recession. Although families are not losing their homes as occurred in the U.S. and elsewhere during the housing bust of 2008, spending by households will likely be constrained nonetheless. The social safety net in China is not as robust or accessible as those in many Western nations. Households must save a large portion of their income to prepare for retirement and for unexpected expenses. Property has been the primary investment vehicle used to generate wealth. As long as the housing market struggles, it is hard to see how the country’s economy can return to its former vibrancy without the central government coming to the rescue far more aggressively than it has to date. But the regime of President Xi Jinping shows no interest in engaging in a massive infrastructure expansion via debt. Correcting the imbalances in the Chinese economy by weaning the populace off its dependence on property speculation and “white-elephant” infrastructure projects may be the best course, but it will take time. Adding to the challenge will be China’s increasingly difficult demographic position and the additional impediments to trade brought on by the geopolitical tensions between the country and other nations, particularly the U.S.

Getting real

Even if the global economy slows and central banks begin to cut policy rates, as we expect sometime next year, longer-term bond yields could stay elevated at, or above, today’s levels. To understand why, we go through the exercise of decomposing the bond yield into its two component parts—a real (inflation-adjusted) rate and an inflation premium.

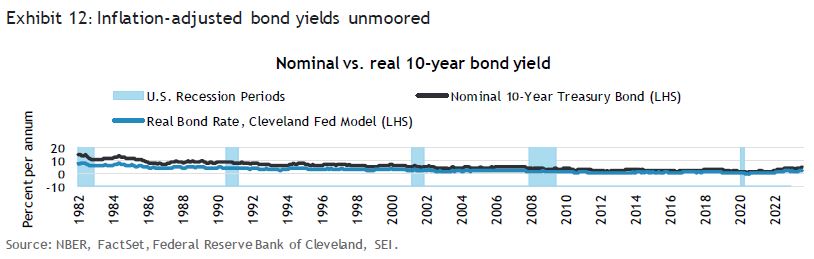

The increase in the yield on the U.S. Treasury’s benchmark 10-year note during the third quarter resulted mainly from a rising real interest rate. Exhibit 12 tracks the nominal 10-year note yield versus a version of the real bond yield that is published by the Federal Reserve Bank of Cleveland. The estimates of the real yield are calculated by the Cleveland Federal Reserve with a model that uses Treasury yields, inflation data, inflation swaps and survey-based measures of inflation expectations. This measure of real yields will differ from those derived solely by looking at the Treasury Inflation Protected Securities (TIPS) market, although those differences over the past year have been rather small (about 0.25 percentage point). In any event, the upward trend in real yields in the U.S. has been in place for roughly three years. Since July 2020, the Cleveland Fed’s calculation of the real yield has soared 2.4 percentage points, from -0.40% to a recent value estimated at 2.00%, while the nominal 10-year Treasury note yield has jumped more than 3.3 percentage points to 4.57% (expected inflation, the difference between the nominal and real bond yield, is therefore up 1.3 percentage points, to a current reading of 2.6%).

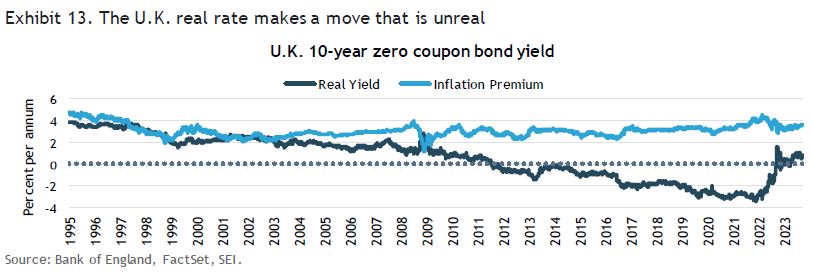

The U.K. also recorded a jump in real yields during the third quarter, as shown in Exhibit 13. But that quarterly rise represents only a small part of the cumulative increase in the real yield over the past three years. The nominal 10-year government zero-coupon bond yield was a mere 20 basis points (0.20%) in June 2020, versus 4.5% currently. The inflation premium was 3.1% three years ago, rising about 0.6 percentage-point since then, to 3.7%. By comparison, the real yield component in June 2020 was -2.9%. As of September 2023, it was in positive territory at 0.9%—a swing of 3.8 percentage points from the lows recorded during the COVID lockdown period.

There is a good reason why inflation-adjusted bond yields in the U.S. and the U.K. have jumped dramatically higher in recent years: Debt issuance has exploded relative to demand. Actually, this is not just a U.S. or U.K. problem. COVID-related assistance to businesses and households, energy subsidies to households struggling through last year’s price spike in Europe, the push for higher military spending, and the inexorable rise in entitlement programs have stressed the finances of many advanced countries.

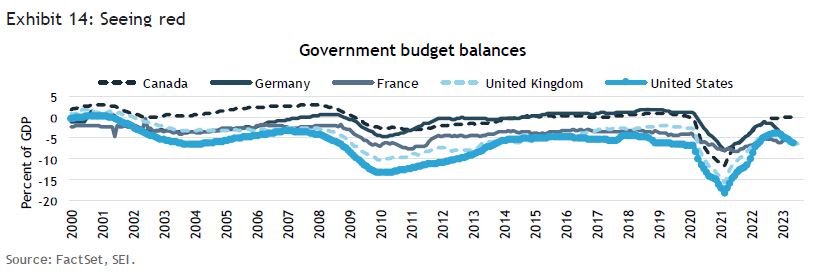

As illustrated in Exhibit 14, government deficits in the major economies deteriorated sharply in 2020 and 2021. Although the red ink was reduced as lockdowns ended, the gap between government revenues and spending is again widening. Of the five countries tracked in the exhibit, only Canada has reached fiscal balance. The other countries are sporting annual deficits that are a far deeper shade of red versus pre-COVID levels. As economies slow and/or slip into recession, automatic stabilizers will kick in, pushing spending up even more and causing revenues to lag on a cyclical basis.

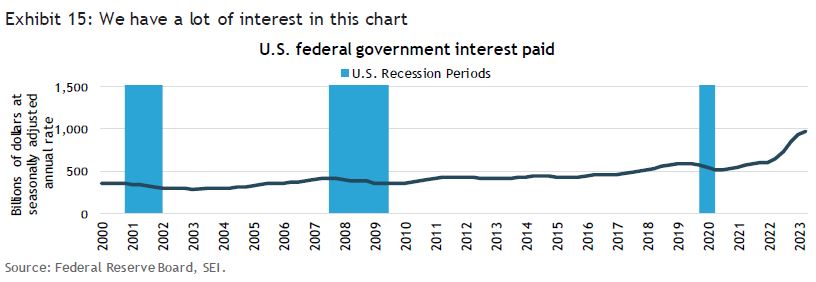

Net interest expense will also continue to increase as older, cheaper debt is refinanced at much higher interest rates. That line item is soaring now in the U.S., where the federal government’s debt is of relatively short duration versus other countries. As of the second calendar quarter, federal government interest paid reached $970 billion on a seasonally adjusted annual rate. That is a 76% increase since the first quarter of 2022. Exhibit 15 underscores how extreme this move really is.

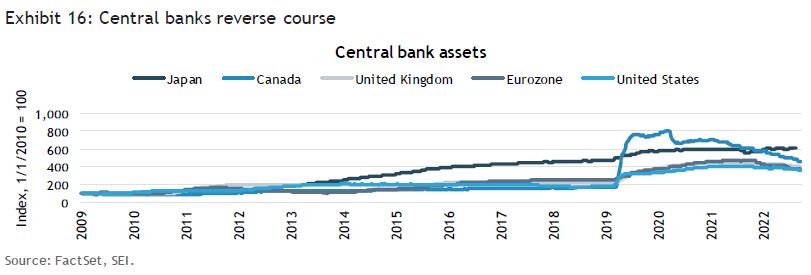

During the worst part of COVID in 2020, central banks globally eased the pressure on interest rates by stepping up their purchases of government securities and other assets. Now they are selling securities out of their portfolios, forcing private investors to shoulder the burden of financing the cascade of government debt issuance. Exhibit 16 highlights the transition from quantitative easing (central banks buying securities) to quantitative tightening (selling securities or simply letting securities run off the balance sheet as they mature). Only the Bank of Japan continues to expand its balance sheet; it is also the only country in the world with a negative policy rate (-0.10%) and a 10-year government bond yield below 1% (0.77% as of the end of September).

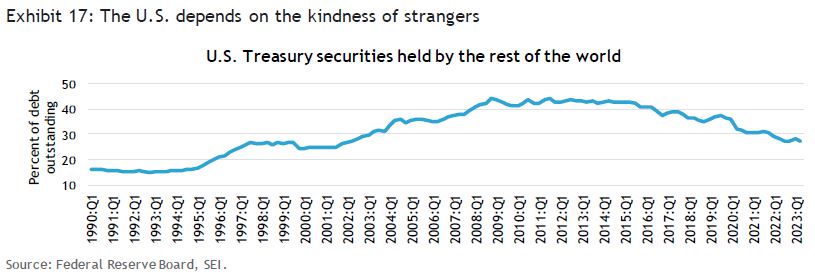

Investment flows, while difficult to track precisely, also point to a less favorable supply/demand backdrop for U.S. Treasury debt. Exhibit 17 highlights the declining percentage of Treasury debt held by the rest of the world. The share of Treasury securities owned by foreigners began to rise quickly in the mid-1990s during the currency and debt crises suffered by Mexico, Brazil, South Korea, Thailand and other developing economies. The ascendancy of China in the first decade of this century then turbocharged the demand for U.S. dollars and Treasury securities as global trade rapidly expanded.

The GFC brought this expansion to a halt, however, and foreign demand for Treasurys has lagged new Treasury issuance since 2015. As a percentage of the total amount of U.S. Treasurys outstanding, foreign ownership is almost back to levels last seen a quarter of a century ago. In absolute dollar terms, foreign holdings have declined modestly since the fourth quarter of 2021. Total Treasury securities outstanding, however, has jumped by nearly 10%. China’s holdings of securities have been on the decline since 2018. The single-largest holder of long-term U.S. government securities until 2019, China now holds fewer Treasurys than investors in the euro area or Japan.

Real interest rates have been forced to move higher in order to attract the necessary funding. For the first time in decades, governments appear to be crowding out other borrowers. We think the rise in government bond yields, whether in the U.S. or other advanced economies, is a structural shift. Recession may place temporary downward pressure on bond yields, but we expect them to stay appreciably above the levels that many observers have considered normal since the GFC 15 years ago.

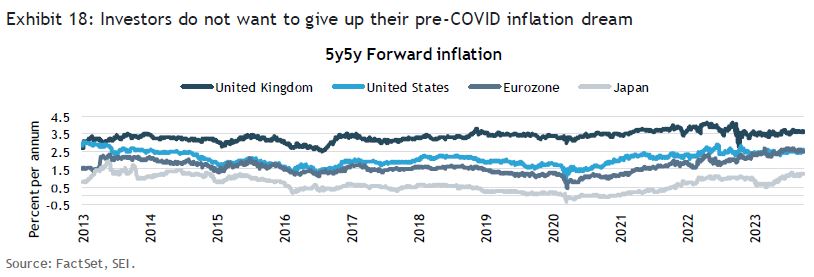

While real yields have moved back to pre-GFC levels, longer-term inflation expectations still appear to be on the low side, in our opinion. Exhibit 18 tracks the 5-year forward inflation rate beginning five years from now. Despite the very high inflation rate experienced over the past two years, market participants’ expectations for longer-term inflation have not moved up very much, either in the U.S. or in the U.K. versus the years leading up to the COVID disruptions. Inflation expectations for the eurozone, by contrast, have moved steadily upward; at 2.5%, the so-called 5-year, 5-year forward rate in the eurozone now nearly equals the U.S. rate. Even Japan’s forward rate has moved decisively higher, although it is still low compared to the other regions/countries.

The recent upward swing in energy prices, if sustained, could push inflation expectations to the upside in the near term. But it is longer-term inflation expectations that really count. For both the U.S. and the U.K., we think that underlying inflation will run at least one-half percentage point higher than what is built into prices.

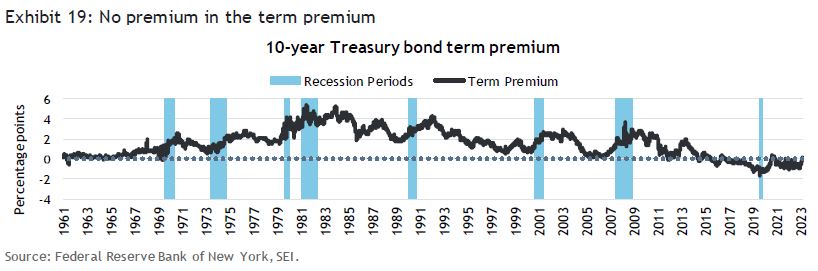

One component embedded in the real yield that we have not discussed is the so-called term premium. This is the amount of interest demanded by investors for holding longer-dated bonds. Exhibit 19 tracks the term premium on the 10-year Treasury note, as measured by the Federal Reserve Bank of New York. It appears to have been unduly depressed since at least 2015, reflecting investors’ complacency about the stability of future inflation and interest rates in general. If inflation runs hotter over time, as we anticipate, its volatility probably will increase, too, implying greater uncertainty. Investors logically should require additional compensation for that extra uncertainty. Importantly, central banks are no longer meddling in the bond market via quantitative easing. The so-called “Fed put” (in which the Fed will act to support financial markets if prices fall significantly) that lulled investors into thinking that central banks will keep the fixed-income markets safe and calm no longer appears to be operative.

The term premium also was quite low in the first half of the 1960s, another time when inflation over the previous decade was calm and quite predictable. It began to rise in the latter half of the 1960s, however, as inflation began to accelerate and government finances deteriorated sharply. It then soared during the very inflationary 1970s—to a peak of more than five percentage points in 1982 and again in 1984.

Cyclically, the term premium also tends to rise during recessionary periods, perhaps an indication of investors’ general nervousness, even though government bonds are viewed as a safe haven in times of stress. The bottom line: A negative term premium is an anomaly that won’t last much longer; in fact, it already has jumped from -75 basis points at the end of June to a positive 10 basis points by the end of September. Even if the Fed cuts policy rates sometime in 2024, as the economy weakens (thereby reducing the pressure on real rates) and inflation continues to moderate, the typical countercyclical rise in the term premium could partially offset those declines.

What it means for investors

Over the past two years, SEI has maintained its view that inflation and interest rates would be higher for longer. As early as the spring of 2021, we mocked the prevailing wisdom by referring to inflation as “persistently transitory.” The view that inflation would quickly return to the Fed’s 2% target resulted in both central banks and investors underestimating how high policy rates would need to go and how dramatically that move would affect yields across all maturities.

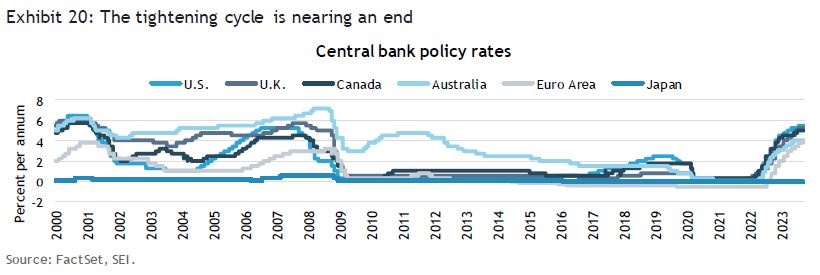

Exhibit 20 tracks policy rates across the major economies. Most central banks did not begin to raise interest rates in earnest until 2022. The U.S., U.K., and Canada kicked off what turned out to be the most aggressive rate-hiking cycle since the 1970s in March 2022, followed by the European Central Bank in July. All along the way, the consensus underestimated the magnitude of tightening that would occur in the face of an inflation problem that proved far less transitory than expected.

Although not quite at the end, the rising interest-rate cycle appears to be finally drawing to a close. Markets reflect the possibility for one or two additional rate hikes across the major economies. These increases may or may not materialize depending upon how quickly economic growth weakens. SEI remains less convinced, though, that markets are correctly anticipating central-bank actions in the second half of 2024. For example, the Fed is expected to cut its policy rate faster and deeper than other countries. We doubt this will happen, especially relative to the eurozone, where the economy appears far more fragile.

The U.K. and Japan are outliers. The Bank of England will probably be slower to cut its Bank Rate, in the absence of a recession. As we have noted here and in previous reports, the country is grappling with an apparent wage-price spiral that has been exacerbated by extreme labor unrest. Japan, meanwhile, hasn’t even embarked on its monetary policy tightening cycle despite a persistent acceleration in inflation that has pushed its year-on-year core inflation rate to 2.8% as of August.

It is our strong conviction that there has been a regime change when it comes to long-run, sustained inflation. Although inflation rates are moderating (painfully slowly in the U.K. and the eurozone, more significantly in the U.S. and Canada), we do not believe that it will get back to central banks’ 2% target over the course of the business cycle. Structurally tight labor markets (mainly the result of the exiting of the baby boomers from the labor force), the diversification of supply chains to reduce dependency on China, considerably higher financing costs, higher corporate taxes as governments seek to reign in their fiscal deficits, and the costly transition to a carbon-neutral world will weigh on corporate profit margins and force companies to pass along those higher costs onto their customers.

Those with a more optimistic outlook assume that productivity growth will accelerate sharply in the years ahead, helping to offset the laundry list of the previously cited negative factors. It certainly is an argument that deserves respect, especially at a time when technologies such as generative artificial intelligence hold such promising possibilities, much like the expansion of the internet did 25 years ago. The Biden administration’s deep push into an industrial policy that incentivizes companies to build advanced semiconductor and electrical vehicle manufacturing plants could lead to the kind of productivity surge registered around the turn of the millennium with the expansion of the internet.

As much as we would like to believe that narrative, Exhibit 21 nevertheless gives us pause. Both productivity and the growth in the capital stock (the total value of the plants, property and equipment to produce goods) do not appear to be on the cusp of a near-term boom. Granted, the five-year annual trend in productivity has been improving, but from an exceedingly low starting point in 2015. While the economic gyrations caused by the COVID lockdown in 2020 and the subsequent rebound make it hard to interpret the more recent trend, the U.S. stock of invested capital has been trending lower over time. The five-year average amounts to only 1.75%, below the mid-1990s trough of 2.1%.

Higher rates, lower equities

The upward shift in interest rates in the third quarter has caused the equity rally to finally stall. The price correction probably has more to go, but we don’t expect it to deteriorate into a bear market. The big tech stocks still appear more vulnerable than the market, however. As we pointed out last quarter, a small number of very large and profitable companies now comprises a big percentage of the market capitalization of the U.S. large-cap universe. Exhibit 22 tracks the combined market capitalizations of Apple, Microsoft, Alphabet, Amazon, Meta, Netflix, Nvidia, and Tesla as a percentage of the overall capitalization of the U.S. large-cap universe, as measured by Ned Davis Research (NDR). That percentage hit a high of 31% in early August, but has eased during the recent market correction. Nevertheless, the decline relative to the overall market has been minimal, especially compared against the prior rebound off the early-January lows. The market-cap share of this “Elite Eight” (NDR refers to them as the “Tech Titans”) is still close to the peak attained in 2020 and above the 2000 tech bubble high-water mark.

Although most of these eight companies have high returns on equity and abundant cash flows, trailing 12-month earnings before extraordinary items have declined to 17.6% of overall S&P 500 Index earnings as of August; that is down from a high of nearly 25% at the end of 2020. At more than 10 percentage points, the difference between the Elite Eight’s share of market cap versus their share of earnings is well above the peaks of 2018, 2020 and 2021. All three of those peaks came before significant price corrections. Investors’ expectations for future growth seem unduly high, perhaps influenced by the hoopla surrounding generative artificial intelligence (AI) and the money being lavished by the Biden administration on the semiconductor companies and providers of green technology.

Exhibit 23 analyzes the total-return performance of the S&P 500 Index by style relative to the overall S&P 500 (total return) since 2016.2 Led by the mega-cap technology stocks, the growth style performed relatively well leading up to COVID, but then enjoyed an extraordinary appreciation in 2020. The investment style’s relative-strength peaked versus the overall S&P 500 towards the end of 2021. It was at that time that SEI warned that these sectors and companies were not only trading at very high valuations to the rest of the market, but were also highly correlated to the bond market. We expected bond yields to rise further in 2022, and argued that, consequently, the big growth stocks would be hurt. As it turned out, bonds logged a historic price decline and long-duration growth stocks were dragged down as well, with the latter surrendering all the relative returns versus the overall S&P 500 Index that they had garnered over the previous two years.

Of course, growth stocks have staged a strong price recovery this year. This is more the result of an increase in valuation rather than an improvement in analysts’ forward earnings estimates. At a forward price-to-earnings ratio of 20, the valuation of the S&P 500 Growth Index is considerably lower than the 30-times earnings logged in 2020 and 2021. The Elite Eight, by comparison, currently sport a forward PE of 27 versus a peak of 38 times in 2020 and a still-high 35 times at the end of 2021. Despite this multiple contraction, valuations on the S&P 500 Growth Index are still at the high end of the range versus the past 20 years when one excludes the super-high readings of the 2020-2021 period.

The S&P 500 as a whole also remains highly valued, our opinion. Equities have moved lower over the past two months, but there may be further price declines ahead. We think analysts’ earnings estimates in the year ahead may prove to be too high, especially if economic growth stalls and a recession develops. We do not believe that U.S. large-cap equities reflect the risk of a significant slowdown.

Exhibit 24 takes a longer-term view highlighting the one-year forward price-to-earnings ratio divided by the five-year consensus expected growth rate of earnings (known as the price/earnings to growth (PEG) ratio). The PEG ratio is still quite elevated, even though the five-year forward earnings growth rate has climbed back to an optimistic 13.1%. As we have argued consistently over the past two years, large multinational companies will face a number of challenges that will make it difficult to maintain the record-high profit margins they have enjoyed. Companies have thus far managed to raise prices sufficiently to keep margins at acceptably high levels. That will probably be more difficult to achieve in the future now that households and businesses will no longer benefit from dollops of fiscal stimulus.

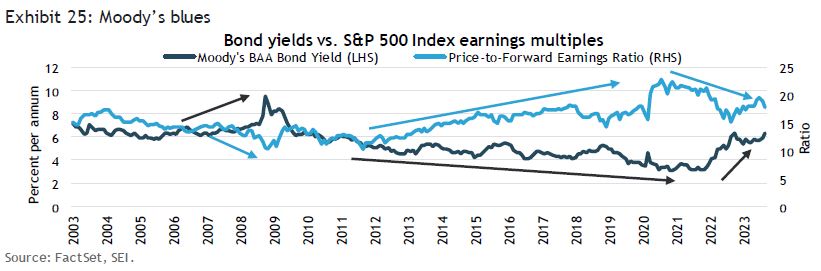

Exhibit 25 highlights another concern: We expect the sharp rise in bond yields to place downward pressure on earnings multiples, just as they did in 2022. For much of the past two decades, earnings multiples have climbed as bond yields declined. This makes sense. If the discount rate at which a future earnings stream and cash flows is falling, that stream of future returns becomes more valuable to an investor. Likewise, when longer-term bond yields rise, the further in the future those returns are (that is, the longer their duration), the lower the value investors should place on them. Note that corporate bond yields are almost back to pre-GFC levels. Price-to-forward earnings multiples were about 15 times then, with a high of 17 (2004) and a low of 10 (2008). That compares to a current reading of 18.

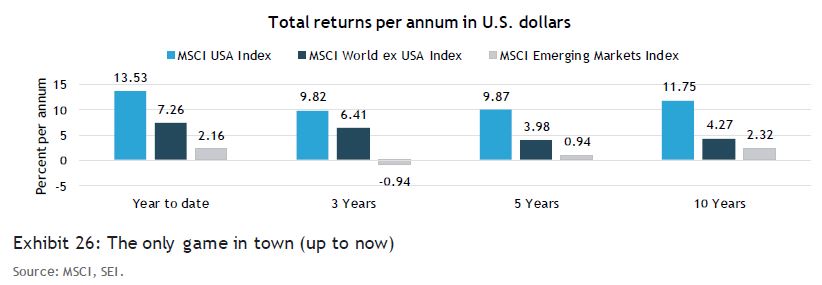

Earnings estimates that are perhaps too high and valuations that do not align with the sharp rise in bond yields over the past two years are a worrisome combination for U.S. large-cap stocks. Diversification across asset classes and across geographies is, in our, opinion a much better strategy than focusing on the Elite Eight or the market capitalization-weighted S&P 500 more generally. We realize that U.S. large-cap stocks have consistently outperformed large caps in other global markets for a long time. Exhibit 26 underscores the persistency of that outperformance for the year-to-date, and the past three-, five-, and ten-year periods.

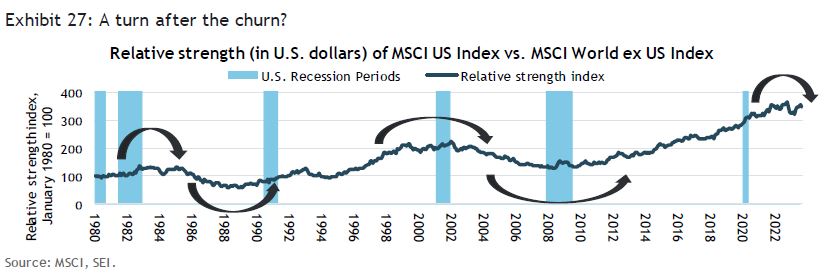

Nonetheless, cycles do eventually turn—even if it takes a long time to materialize. Exhibit 27 tracks the relative strength of the MSCI USA Index (net) versus the MSCI World ex-U.S. Index (net) since 1980. There is no denying the superior performance of the U.S. stock market versus other developed-economy stock markets. There have been two multi-year periods, however, when international stocks have outperformed in U.S. dollar terms: from 1985 to 1989, and from 2002 to 2008. Both of those periods were highlighted by a prolonged weakening of the dollar’s currency value. Major market bottoms and tops, however, take time to develop. There is quite a bit of churn before a new trend decisively takes hold. Perhaps the action of the past two years is a harbinger of another change in trend. Only time will tell.

To summarize:

- The U.S. economy has exhibited surprising strength, but we don’t believe it is sustainable. A mild recession in 2024 still seems to be a reasonable expectation, although the consensus has swung away from that view.

- Other major economies are showing more notable weakness. Germany is already in recession, and the U.K. might be experiencing a recession, too. China’s post-COVID rebound has been extremely disappointing; the troubles of the property sector could lead to a prolonged period of subpar economic growth.

- Inflation is falling as supply-chain disruptions end. However, we still believe that U.S. inflation will run at a sustainably higher rate than the Fed’s 2% target. Structurally tight labor markets, the shift of global supply chains away from China, higher financing costs, the disruptions cause by the transition to a carbon-neutral regime, and a likely boost in corporate tax rates in the years ahead suggest to us that a 3%-plus inflation rate is more likely than a sub-2% rate.

- Fed policy-rate increases are coming to an end. There could be one more rate hike, but it looks a bit more unlikely now that the worst labor-market pressures are easing. However, we don’t see the central bank cutting rates until the second half of 2024. The latest FOMC projections for the federal funds rate clearly indicate an intention to keep the policy rate higher for longer.

- Other major central banks are in similar positions. Europe has a somewhat greater potential to raise its policy rates one or two more times given its stubborn inflation problem and the fact that the level of rates is still appreciably lower than the U.S. federal funds rate. The U.K. is closest to a wage-price spiral and will be forced to lean against it with a monetary policy that is tighter than the Bank of England would prefer to implement; the Bank Rate will decline only with the onset of recession. The Bank of Japan is under increasing pressure to start raising its policy rate in order to firm up the yen.

- Bond yields have risen despite lower inflation rates, implying a big jump in real yields. We think markets are responding to the increase in government debt issuance at a time when central banks are adding to supply pressures via quantitative tightening (i.e. reducing their bond holdings).

- We expect bond yields to remain elevated as market participants adjust their expectations regarding central bank policy (i.e., higher for longer) and also build back into bond yields a positive term premium (reflecting higher uncertainty about future interest-rate risk).

- Equity markets have entered a corrective phase. U.S. large-cap equities are expected to trade in a broad range, with the S&P 500 Index currently remaining closer to the upper end of that range. High-growth companies are vulnerable to rising bond yields, and more cyclical and economically sensitive companies could face pressure from declining profit margins.

Index definitions

The Citigroup Economic Surprise Index measures the degree to which a core set of economic data series has been coming in under expectations, at expectations, or over expectations.

The MSCI USA Index tracks the performance of the large- and mid-cap segments of the U.S. equity market. The index’s 624 constituents comprise approximately 85% of the free float-adjusted (i.e., including only shares that are available for public trading) market capitalization in the U.S.

The MSCI World ex USA Index tracks the performance of the large- and mid-cap segments of equity markets across 22 of 23 developed- market countries--excluding the U.S. The index’s 887 constituents comprise approximately 85% of the free float-adjusted (i.e., including only shares that are available for public trading) market capitalization in each country.

The price-to-earnings ratio is calculated by dividing the current market price of a stock by the earnings per share. Price/earnings multiples often are used to compare companies in the same industry, or to assess the historical performance of an individual company.

A purchasing managers’ index (PMI) tracks the prevailing direction of economic trends in the manufacturing and service sectors.

The S&P 500 Index is a market-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

The S&P 500 Growth Index is a market-weighted index that tracks the performance of the fastest-growing stocks within the 500 Index. The index employs three factors: sales growth, the ratio of earnings change to price, and momentum.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs, or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

The opinions and views in this commentary are of SIEL only unless stated and are subject to change. They should not be construed as investment advice.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 57551995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This email and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.