Quarterly Market Commentary: Stocks Surge into Summer

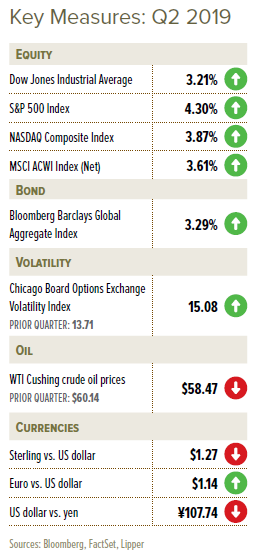

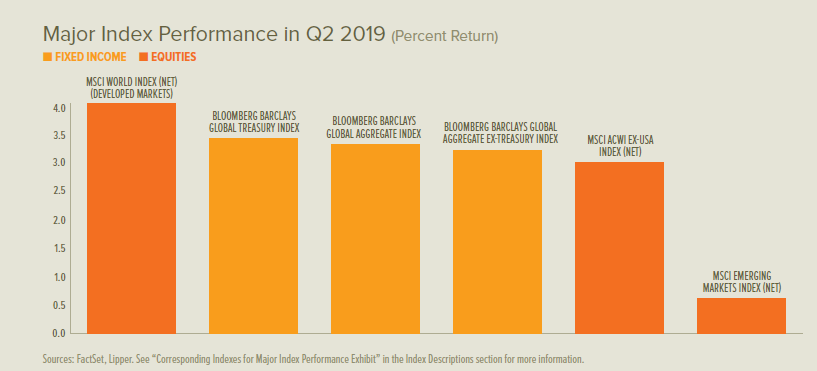

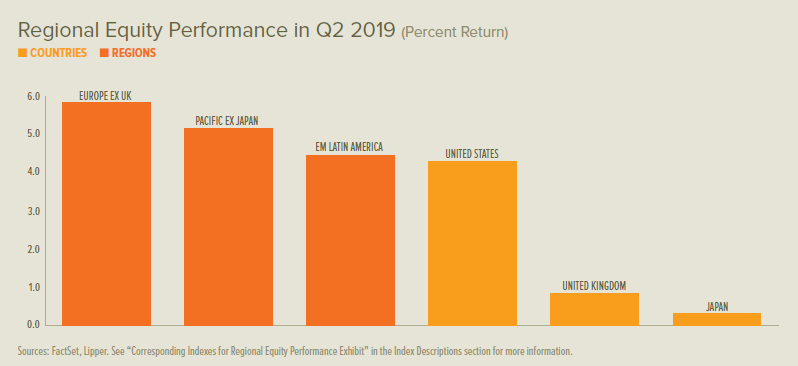

Stocks around most of the world continued their early-year rally before tumbling throughout May and then recovering to varying degrees in June. UK and European equities rallied, but fell short of reaching their late-April highs. Similarly, Japanese stocks jumped sharply at the end of the quarter without hitting their late-April peak. Mainland Chinese stocks also bounced back convincingly, more so than those in Hong Kong, but failed to recover fully. US and Brazilian stocks were the only regions to record all-time highs, both surpassing their prior peaks in June.

Government-bond rates increased in the UK, Europe and US during April, but ultimately moved lower over the quarter as a whole. As for US Treasurys, after briefly inverting in March, the 3-month-to-10-year spread once again turned negative in May—where it remained throughout the second quarter. This triggered concerns about the US economy, as an inverted yield curve is commonly considered a reliable recession indicator.

After Theresa May announced her resignation in late May, a race opened for her role as UK Prime Minister and leader of the Conservative Party. The crowded candidate field quickly narrowed—pitting former Foreign Secretary Boris Johnson as widely favoured over his successor Jeremy Hunt. Johnson has campaigned on an explicit willingness to depart the EU without a deal upon the 31 October deadline, but has made conflicting comments on the likelihood of this outcome. Jean-Claude Juncker, president of the European Commission, stated in June that the divorce deal established during May’s tenure is not open for renegotiation despite the British leadership contest.

Trade negotiations between the US and China had promising momentum at the start of the quarter, but soon deteriorated in early May. The US announced an escalation of existing tariffs on $200 billion of Chinese imports from 10% to 25%, and proposed expanding the scope of the 25% tariffs to an additional $300 billion of imports—prompting smaller retaliatory tariffs from China. However, the US stalled the proposed tariffs in late June to entice Chinese President Xi Jinping to meet with President Donald Trump on the side-lines of a Group of 20 summit (an international forum for governments and central bank governors from 19 countries and the EU); the meeting produced a temporary truce as both sides agreed to return to the negotiating table.

Central Banks

- The Bank of England’s Monetary Policy Committee made no changes at its May or June meetings. It maintained a preference for tighter monetary policy with the caveat that this stance could be upended by Brexit uncertainty, which it noted has increased.

- The European Central Bank (ECB) extended its commitment to retain low European benchmark rates (for refinance, deposit and marginal lending) through the first half of 2020, and said it will continue to reinvest the principal proceeds from its asset-purchase programme for at least as long. ECB projections for overall economic growth and inflation were revised marginally higher for 2019, but lower for future years.

- The US Federal Open Market Committee (FOMC) made no changes at its May or June meetings. However, its statement following the latter did not include its prior commitment to patience, and indicated increased uncertainty along with a less-positive assessment of economic fundamentals. The decision in June to hold rates provoked one dissenting vote—the first of Jerome Powell’s tenure as Federal Reserve Chairman—in favour of cutting the federal funds rate.

- The Bank of Japan made no changes at its April or June meetings, staying accommodative by maintaining a negative short-term policy rate and a rate of approximately zero on 10-year Japanese government bonds.

- The People’s Bank of China undertook various efforts to balance the country’s cooling economic growth and support the yuan’s exchange rate—including providing liquidity to the financial system by renewing lending facilities, issuing reverse repurchase agreements, and conducting bill swaps. The China Banking and Insurance Regulatory Commission took control of the failing Baoshang Bank in late May, representing the first Chinese bank rescue in almost two decades; as a consequence, smaller banks were confronted with funding roadblocks and higher borrowing costs.

Economic Data

- The UK services sector accelerated out of a contraction early in the second quarter and with increased speed in May. Manufacturing conditions moved in the opposite direction, starting the period moderately expanding before deteriorating to a standstill in May and ultimately contracting in June. The UK claimant count, which measures the number of people claiming unemployment, edged upward to 3.1% in May after holding firm at 3.0% in the prior month. Overall, UK economic growth accelerated in the first quarter to a rate of 0.5% from 0.2% in the prior quarter; the year-over-year pace also increased during the first quarter, to 1.8% from 1.4% in the final three-month period of 2018.

- Eurozone manufacturing activity contracted throughout the second quarter as output steadily declined and new orders continued to drop. Meanwhile, services growth remained moderate for the duration of the second quarter. The European unemployment rate moved lower through the first two months of the period, settling at 7.5% in May. The eurozone economy expanded by 0.4% during the first quarter, doubling the rate of growth in the prior quarter; year-over-year growth increased to 1.2%.

- Growth in the US manufacturing and services sectors slowed sharply in the beginning of the second quarter before maintaining a modest expansion later in the period. Personal income growth outpaced consumer spending through April and May; the US unemployment rate declined to 3.6% in April and held steady in May. Overall economic growth registered an annualised 3.1% rate during the first quarter.

SEI’s View

July marks the tenth anniversary of the US economic expansion. The bull market in US equities (as measured by the S&P 500 Index) reached its tenth birthday in March. The S&P 500 Index seemed to celebrate these achievements just a few weeks ago by moving into new-high territory. But there now seems to be anxiety that the bull market in equities is on its lastlegs, the victim of a slowing global economy, the lagged impact of last year’s US interest-rate increases and, perhaps most importantly, a worsening tradewar between the US and China.

To be sure, the US economy is hardly firing on all cylinders. There’s a good chance that capital spending will continue to ease in the months ahead, but we’re not forecasting a major downturn. Corporate cash generation continues to run slightly ahead of capital expenditures. The main point to remember: It’s not unusual for capital expenditures to run well in excess of cash flow, especially toward the end of the economic up-cycle. And that’s not happening yet.

We need to see a severe deterioration in financial and leading economic indicators before climbing onto the recession train. Even after the past two years of multiple Fed rate increases, there are still few signs of a build-up in financial stress.

The big unknown, of course, is how the evolving tariff war between China and the US will affect US economic growth and global trade in the months ahead. Tariff tensions and worries about global growth have put only a modest dent in the confidence of American businesses. But it certainly looks as if the US-China trade relationship is frosty at best, even though the countries’ leaders declared a tariff truce in order to continue negotiations.

It is our view at SEI that the US economy should be able to weather this storm. An all-out tariff war between the two largest economies in the world will certainly disrupt supply chains and likely lead to higher prices for a broad range of consumer goods. Still, we think it helps to keep the problem in perspective. Even if the US imposes a 25% tariff on all Chinese imports, total duties will amount to roughly 0.5% of US gross domestic product, according to our calculations of data provided by the United States International Trade Commission.

It is not our intention to minimise the importance of the shift in US trade policy toward protectionism. The speed and ease with which supply chains can be relocated to other countries will be a critical factor, either exacerbating or tempering the tariff impact on consumers and companies in both the US and China. An escalation of the trade wars by the US against other countries would prove far more dangerous for the near-term growth prospects in the US than if trade were disrupted only with China.

We have been thinking that the US would avoid waging multiple tariff wars as it has concentrated its firepower on China. But our persistent optimism may not hold. Tariffs on German and Japanese autos are still a possibility later this year.

In all, we think the US economy will show resiliency in the face of what is admittedly a stiff headwind. Household income growth has continued to advance at a good pace. The decline in US interest rates that began late last year should certainly help consumers.

The market-implied rate (based on federal-funds futures contracts) projects a federal-funds rate of 1.7% by the close of 2019, according to the Chicago Board of Trade, consistent with three 25 basis-point cuts. Although the forecasts of FOMC members have been more cautious, they are moving in the direction of the markets. The recent decline in bond yields to levels last seen in 2016 ranks as one of the biggest surprises of the year. We find it hard to justify these moves. In our view, recession is not likely without a severe policy mistake, such as fighting a tariff war on multiple fronts.

When one considers all the headwinds facing emerging economies—a significant slowdown in Chinese economic growth, on-going trade tensions between the US and China, weak commodity pricing, and a still-resilient US dollar—it’s surprising that emerging stock markets have appreciated at all this year. But as long as a tariff truce remains in place with the US, we expect China’s economy to improve in the months ahead. Scores of measures, both monetary and fiscal, have been put in place over the past year.

Europe currently faces a variety of idiosyncratic challenges, both economic and political, that makes it hard for even contrarian investors to get terribly enthusiastic about the near term. Economically, the downward trajectory is similar to that of the 2011-to-2012 period amid the region’s periphery debt crisis. This time, however, Germany’s industrial economy is fully participating in the slowdown.

It’s not just the region’s heavy exposure to manufacturing and international trade that makes German industrialists glum. There is also a worrisome vacuum of political leadership. Chancellor Angela Merkel is on her way out, and a politically distracted Germany is a concerning issue given the country’s central importance in the eurozone and EU.

At the supra-national level, Germany’s Ursula von der Leyen was nominated to serve as president of the European Commission (the executive arm of the EU), and Christine Lagarde of France (the current president of the International Monetary Fund) will succeed Mario Draghi as president of the ECB at the end of October. Lagarde is expected to maintain her predecessor’s dovish policies. Perhaps before Draghi leaves office, we will see another interest-rate cut that brings policy rates deeper into negative territory. And we can’t rule out a new round of quantitative easing, just as the current one is set to end.

President Draghi has reason to be concerned. But unconventional monetary policy in the form of negative European interest rates, quantitative easing and term lending facilities do not carry a lot of punch nowadays. An aggressive easing of fiscal policy makes sense, but that strategy is a non-starter in the eurozone. Once again, the structural flaws of the eurozone are coming to the fore.

And then there’s the looming cloud of Brexit. Although it has been delayed until 31 October, there is little sign that the breathing space will be put to good use. It appears likely that Boris Johnson will win the Conservative Party’s search for a new Prime Minister. It’s hard to see how that improves the chances of an orderly exit.

Although economic growth is sluggish, the UK economy is not exactly cratering as the deadline approaches. In fact, the UK unemployment rate fell to a multi-decade low. The eurozone also recorded steady labour-market improvement; however, the jobless rate itself remained far higher, owing to structural factors.

That being said, we can’t help but think Brexit (if it indeed occurs) will prove to be a highly disruptive event for the UK and the EU. Roughly half of the UK’s trade in goods, both imports and exports, is with the EU.

We think there is still life in the economic expansion, both in the US and globally. If we’re right, that means corporate profits should continue to expand and push global stock markets to higher levels in the months ahead. This may seem like a bold statement at a time when the world seems increasingly unpredictable and the economic data point to slowing growth. Yet we simply do not yet see the economic imbalances or nosebleed equitymarket valuations that normally bring on recessions and an associated contraction in earnings and stock prices. It is also clear that central banks have investors’ backs as monetary policymakers are making promises about (or already are) cutting interest rates in various parts of the world and providing additional liquidity to their banking systems in both developed and emerging countries.

Glossary of Financial Terms

Dovish: Dovish refers to the views of a policy advisor (for example, at the Bank of England) that are positive on inflation and its economic impact, and thus tends to favour lower interest rates.

Federal-funds rate: The federal-funds rate is the interest rate at which a depository institution lends immediately-available funds (balances at the US Federal Reserve) to another depository institution overnight in the US.

Price-to-earnings ratio: The price-to-earnings ratio is the ratio of a company’s share price to its earnings over the past 12 months; it can be is used to help determine whether a stock is undervalued or overvalued.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publiclytraded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.