Quarterly Market Commentary: Stocks Splash Higher Despite Waves of Uncertainty

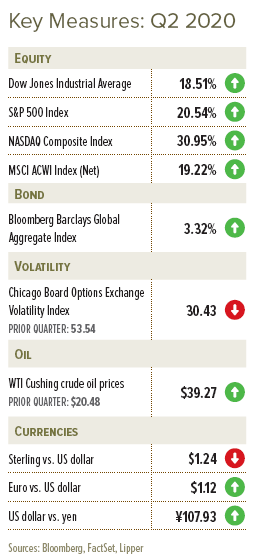

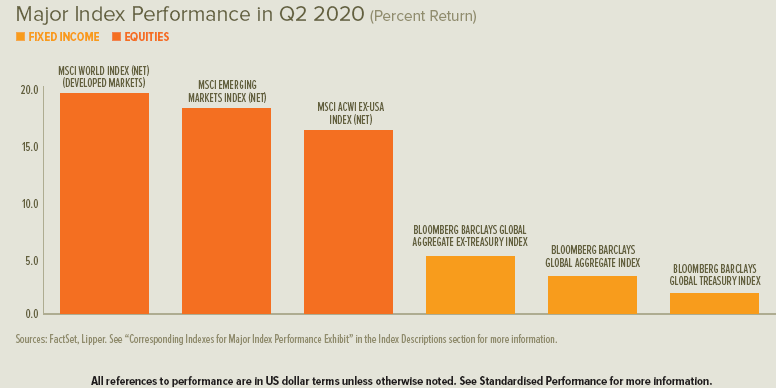

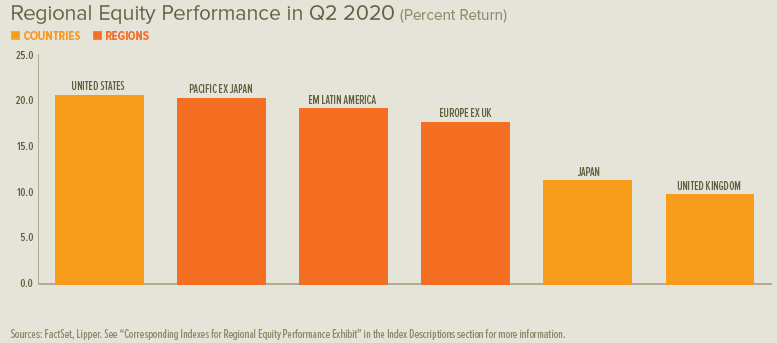

Equities around the world spent much of the second quarter embracing the sharp rebound that began at the end of March. Shares were universally higher for the full quarter; although every major market besides China peaked in early June and failed to make new highs thereafter. Recoveries varied in size, and some markets had their best quarter in several years. US shares had the highest quarterly performance since 1998.

Gilt rates were lower across all maturities for the full three-month period. Short-to-intermediate-term rates ended near their lowest-ever levels, while long-term rates climbed throughout the quarter after bottoming in April (albeit returning only partway to their first-quarter finish). European government-bond rates nearly completed a round trip during the second quarter—falling in April, climbing in May, and falling back at the end of June to almost exactly where they concluded the first-quarter. US Treasury rates with the shortest and longest maturities increased during the full quarter, while the rates of those with maturities of 1-to-10 years declined. Across maturities, Treasury rates at the end of June were almost identical to those at the end of May, as the entire yield curve moved higher through early June before reversing.

The West-Texas Intermediate (WTI) oil price plummeted below zero US dollars per barrel in April for the first time in history as its contract for May delivery neared expiration2. Subsequent contracts traded higher in light of a 23-nation agreement led by the US, Saudi Arabia and Russia to cut production by 10 million barrels per day—and the WTI oil price finished June at $39.27 per barrel. The gold spot price climbed throughout the second quarter to its highest level since 2012 amid unprecedented government spending and deep uncertainty about the economic outlook.

The EU re-opened its internal borders in mid-June and prepared to open for external travellers on 1 July, yet with restrictions still applied to citizens of some outside countries (including the US). Several US states reported an early-June surge in their respective COVID-19 infection rates after pushing to reverse their lockdowns earlier than other states. Texas also noted a string of record-high COVID-19-related hospitalisations at the time, prompting state officials to backpedal its re-opening plans; many other states saw a rising share of positive COVID-19 test results amid expanded overall testing. As a result, several Northeastern states that served as the country’s original outbreak epicentre announced 14-day quarantines for visitors from US states that were experiencing recent spikes. The first dedicated COVID-19 treatment—Remdesiver—came to market in late June.

The UK and EU struggled to establish their regulatory equivalence in a combined effort to grant mutual access to their financial markets after the Brexit transition period concludes at the end of 2020. The two sides failed to reach an agreement by the proposed 30 June deadline; while the UK said it is prepared to grant the EU access to UK financial markets, the EU stated that the UK has not provided sufficient information to complete its evaluation.

The Office of the US Trade Representative issued a notice in late June that it was considering imposing tariffs on about $3 billion in imports from the UK, Germany, France and Spain. The World Trade Organization approved $7.5 billion in US tariffs on European products in late 2019, and may also approve retaliatory European tariffs on US products.

US borders were set to remain closed to Canada and Mexico until at least 21 July as part of the Trump administration’s latest one-month extension, which began on 20 March. The United States–Mexico–Canada Agreement (USMCA) took effect on 1 July, officially replacing the North American Free Trade Agreement (NAFTA).

China passed a new national security law for Hong Kong in June, categorising an array of subversive activities as criminal behaviour and carrying sentences as steep as life imprisonment. The ruling also enables Beijing to supervise and intervene in the policing of these activities, as well as the final word on interpreting the law.

Several governments around the world condemned this development. UK Prime Minister Boris Johnson said Britain was considering a path to citizenship and relocation for British Nationals (Overseas) (a class of British nationality extended to Hong Kong residents prior to the 1997 handover). The US imposed visa bans on several Chinese central government officials, to which Beijing responded with visa restrictions on Americans “who behave badly in Hong Kong affairs.”

On a positive note, the head of China’s Securities Regulatory Commission expressed willingness to cooperate on joint company inspections after the US raised the prospect of barring Chinese companies from its financial market if they continued to block transparent audits. China also announced plans to accelerate purchases of US agricultural goods to uphold its commitments to the phase-one trade deal.

In mid-June, Chinese and Indian soldiers skirmished (without firearms) along a disputed border ridge in the Himalayas. India reported at least 20 of its soldiers were killed in the fight, while China did not release information about casualties. At the end of the month, India retaliated by banning scores of mobile apps originating in China (several of which have been widely downloaded around the world).

Economic Data

UK manufacturing activity continued apace in June—neither contracting nor expanding—representing an improvement on the prior month’s slowing contraction following an extraordinary drop in April. UK services activity nearly stopped contracting in June after a similarly dramatic dive in April and a modest improvement in May. The UK claimant count unemployment rate spiked from 3.5% in March to 6.3% in April, and then to 7.8% in May. The overall UK economy contracted by 2.2% in the first quarter and 1.7% year over year.

The eurozone’s contraction in manufacturing activity continued to ease through May and June after an unprecedented slowdown in April. Eurozone services activity also plummeted in April, but improved somewhat in May before nearly coming out of contraction in June. Loans to non-financial European corporations accelerated for the fourth consecutive month, increasing by 7.3% in May after gaining 3.0% in February, 5.4% in March, and 6.6% April. The overall eurozone economy contracted by 3.6% during the first quarter and 3.1% year over year.

US manufacturing activity nearly returned to growth in June after contracting sharply in April (albeit not as deeply as in the UK or eurozone) and improving in May. Activity in the US services sector plummeted more dramatically in April compared to the US manufacturing sector, and did not rebound to as great a degree as US manufacturing through June. American workers submitted more than one million unemployment claims for 14 consecutive weeks through late June (a level of joblessness previously never breached in the data series’ 50-plus years), peaking in late March and early April above 6 million claims, but drastically slowing its rate of improvement in June3. The overall US economy contracted by a 5.0% annualised rate during the first quarter, and the National Bureau of Economic Research confirmed the country entered recession in February.

Central Banks

- The Bank of England’s (BoE) Monetary Policy Committee held the Bank Rate at 0.1%, during the second quarter; following its mid-June meeting, the central bank announced that it would expand its stock of asset purchases (from an initial £200 billion increase announced in March) by another £100 billion to £745 billion.

- The European Central Bank (ECB) held its benchmark rates unchanged during the second quarter. It unveiled the pandemic emergency longer-term refinancing operations (PELTROs) in April to help facilitate proper functioning of money markets; in early June, it also announced the expansion of its Pandemic Emergency Purchase Programme (PEPP), which is designed to facilitate asset purchases, by €600 billion to a total of €1.35 trillion.

- The US Federal Open Market Committee (FOMC) maintained its monetary-policy path throughout the second quarter—providing assurances in early June that it would not raise the federal funds rate for the foreseeable future and that it would maintain quantitative easing via purchases of Treasurys and mortgage-backed securities (MBS). The FOMC began purchasing corporate bonds during the second quarter via programs that it established as part of its pandemic response.The Federal Reserve (Fed) ordered banks to cut dividends and halt stock buybacks following stress tests on the prospect of an extended economic downturn resulting in a higher rate of loan defaults.

- The Bank of Japan (BOJ) held course following its mid-June meeting, maintaining its short-term rate and its target rate for the 10-year Japanese government bond. However, it did share an expectation to inject ¥110 trillion into the Japanese economy to offset the COVID-19 health crisis.

SEI’s View

Despite mounting infections, hospitalisations and deaths from the pandemic—as well as the unprecedented stoppage of global economic activity—stock markets around the world managed to mount a resounding comeback.

Our working assumption is that there will likely be another significant wave of infections going into the fall-to-winter flu season. The question is, how disruptive will it be to the global economy?

Investors seem to be ignoring the possibility that, even if a sustainable recovery gets under way, it may be a long time before most companies achieve previous levels of profitability. The after-tax profit margins of US domestic businesses were already on a declining trend before the onset of the virus and shelter-in-place orders.

Margins will likely remain well below their previous peaks around the globe as long as COVID-19 is a severe health threat. Most businesses, to one degree or another, are expected to endure lower sales, higher costs and a decline in productivity. There also will probably be a deadweight loss for industries needing extra inventory on hand in order to guard against future shortages and supply-chain disruptions caused by periodic flare-ups of the virus. “Just-in-time” inventory management will turn into “just-in-case” inventory management, tying up cash. Supply chains will likely be diversified over time, a process that was already under way as a result of the trade war between China and the US.

The extraordinary March-to-April lockdown in the US necessitated fiscal measures unparalleled in scope and speed of implementation. The result has been a tsunami of red ink. The Congressional Budget Office projected the deficit will reach nearly 18% of US gross domestic product (GDP) in 2020 and improve to only 10% of GDP in 2021. US debt relative to GDP is forecast to rise to 108% by the end of fiscal year 2021 versus 79% at the end of fiscal year 2019.

These are unsettling numbers. Many investors wonder whether such a surge in government debt will provoke an economic crisis even after the pandemic runs its course. We don’t think that it will. The US has a large, dynamic economy and deep capital markets. If investors were truly concerned about the long-run fiscal viability of the US, the value of its currency would have been falling more convincingly and long-term US interest rates would have been going up (not down).

The policies pursued by the Fed have also served to keep interest rates low. Its balance sheet has ballooned this year, far exceeding the increases logged by the ECB or the BOJ.

The US certainly is not alone in engaging in a huge fiscal response that is then monetised by the central bank. In our opinion, governments are treating the fight against COVID-19 like they would a war. As many resources as possible are being thrown into the fight, supported by debt issuance that is absorbed primarily by the central banks.

Those who remember the 1970s are understandably worried by the inflationary potential of such extraordinary debt monetisation. If it does lead to inflation, it probably won’t be any time soon, in our opinion. Given our view that the economy will remain below full utilisation of labour or productive capacity for the next few years, we believe inflation is unlikely to break out of the 0%-to-3% range it has been in for much of the past decade.

Investors do not seem too concerned about the speed of Europe’s economic recovery or the impact of the health crisis on countries’ fiscal positions. The bond yields of the most economically-fragile countries remain close to those of German bund yields, although spreads have widened from pre-pandemic levels. The ECB has been quite successful in short-circuiting the liquidity crisis and flight-to-safety that threatened the euro area’s financial structure.

This laid-back view would be severely challenged if the 27 members of the EU fail to approve a €750 billion emergency fund when the EU’s leaders meet again in July. Although Germany has joined forces with France to push the package forward, there is still resistance from the likes of the Netherlands, Sweden, Denmark and Austria. There is disagreement, for example, over the split between grants and loans. Italy and Spain would be the biggest beneficiaries of grants to help offset their current fiscal dilemmas, while the remainder of the package would be distributed as conditional loans. Paying for the grants is an even greater source of contention. The European Commission (EC) would be empowered to issue long-term bonds, which would be paid down by giving the EC taxation authority (a power it currently does not have). The only alternative would be to increase contributions from member states (a bigger problem now that the UK is leaving the EU) or enact spending cuts in other parts of the EU budget.

Speaking of the UK, the COVID-19 crisis has pushed Brexit concerns off the front pages. As the 31 December transition deadline nears, it could become an economic factor nearly as important as a second wave of the virus. If a deal on the UK-EU trading relationship is to be delivered before year-end, it probably should be concluded by the end of October so that countries have time to approve the treaty into law. Any free-trade agreement would require the UK to agree to permanently align its rules and regulations to those of the EU on an array of matters. The UK would essentially bear much of the EU membership cost without having a voice at the table that sets the rules. It is becoming increasingly likely that there either will be a modest agreement that includes tariffs or, in the worst-case scenario, a no-deal result that falls back on the World Trade Organization’s most-favoured-nation rules.

While many factors determine equity performance, in the emerging-market space it has correlated with the extent of economic disruption caused by the virus. Asian and central European countries have pulled back the most on their mandates to restrict movement and social interaction. Latin America and India have eased some of those constraints, but not nearly as much as the other two regions. We continue to keep close tabs on China, as it was the first to lock down and first to unlock activity. We expect recovery patterns elsewhere in the world to follow that of China.

Central banks in the emerging world are also doing their part to help restore their economies. Interest rates have come down in almost every country in recent months to record-low levels in many cases. In addition, a dozen emerging-country central banks—including those with shakier reputations, such as South Africa and Turkey—are either buying or planning to purchase their government’s debt. We think this debt monetisation may lead to an inflation problem in the future.

It’s been said many times that bull markets climb a wall of worry. Maybe now they must learn to swim through waves of worry that include:

- The possibility of a second wave of COVID-19 infections forcing another round of extensive lockdowns and shelter-in-place orders that could lead to a double-dip recession

- A possible break down of political consensus regarding the way forward as economies struggle to regain strength

- The likelihood that economic recovery will take at least a year, and likely longer—and that few economies are likely to rebound fully to pre-pandemic levels, even if most countries manage to avoid a disruptive second wave of the virus

- Expectations that companies will face higher costs and increased inefficiencies; that taxes will almost certainly rise across many economies in the years ahead; and that bankruptcies and defaults will climb as government aid programs end

We believe that an ebb and flow of assorted concerns in the coming months will continue to spark volatility across financial markets. Such periods of instability are expected in any long-term investing plan; as such, SEI is just as prepared as always to navigate the current wave of deep uncertainty.

Glossary of Financial Terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to rise) and investor confidence is high.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Pandemic Emergency Longer-Term Refinancing Operations (PELTROs): PELTROs are a series of longer-term refinancing operations intended by the ECB to ensure sufficient liquidity and smooth money market conditions during the COVID-19 pandemic period. PELTRO operations are planned to be allotted on a near-monthly basis maturing in the third quarter of 2021.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly-traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.