Quarterly Market Commentary: Stocks retreat on higher for- longer interest-rate fears

Global equity markets experienced a downturn during the third quarter of 2023. There were numerous periods of volatility amid investors’ uncertainty regarding the implications of a higher-for-longer interest-rate environment, as well as worries about China’s weakening economy. These offset a market rally in July prompted by optimism that the Fed might be able to curb inflation

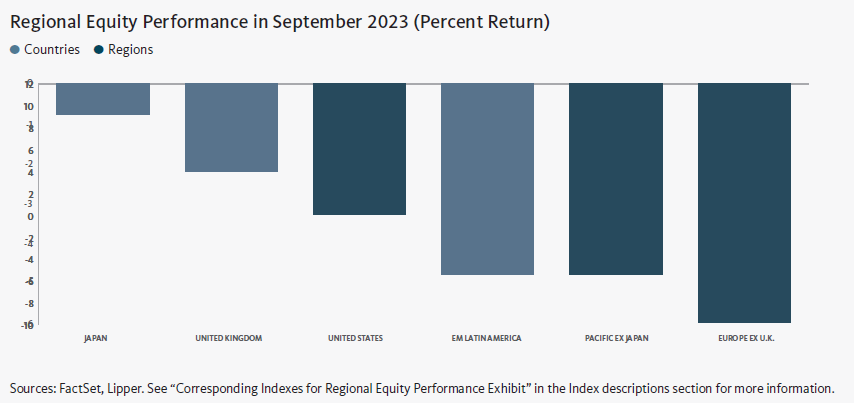

while piloting the economy to a soft landing. Emerging markets modestly outperformed their developed-market counterparts for the period. The Nordic countries recorded comparatively smaller losses and were the top performers among developed markets for the quarter, benefiting mainly from strength in Norway and Denmark. Europe was the weakest-performing developed market over the period attributable largely to notable losses in the Netherlands and Portugal. In contrast, within the emerging markets, Europe garnered a positive return and was the top performer during the month, bolstered mainly by a double-digit gain in Turkey. Conversely, the Eastern Europe ex. Russia region was the primary laggard among emerging markets due to weak performance in Poland.1

As widely expected, the Fed increased the federal-funds rate by 25 basis points (0.25%) to a range of 5.25%-5.50% at its meeting in late July, and subsequently left its benchmark interest rate in a range unchanged following its meeting in September. In a statement announcing the pause in September, the Federal Open Market Committee (FOMC) reiterated its commitment

to bringing inflation down to its 2% target rate and cautioned that “tighter credit conditions for households and businesses are likely to weigh on economic activity, hiring, and inflation. The extent of these effects remains uncertain.” The central bank also commented that it “would be prepared to adjust the stance of monetary policy as appropriate if risks emerge that could

impede the attainment of the Committee’s goals.”

China recently has experienced relatively weak credit growth, a downturn in exports, and a year-over-year decline in consumer prices. Lower demand for goods and services from Chinese consumers could have a negative impact on other countries’ exports of iron ore, crude oil, factory equipment, and luxury goods into the country. U.S.-based manufacturers of chemicals and heavy machinery have cautioned that they may experience a slowdown of sales in China. Additionally, a large property developer filed for protection under Chapter 15 of the U.S. bankruptcy code, which safeguards non-U.S. companies that are undergoing debt restructurings from creditors seeking to sue the firms or to freeze their assets in the U.S.

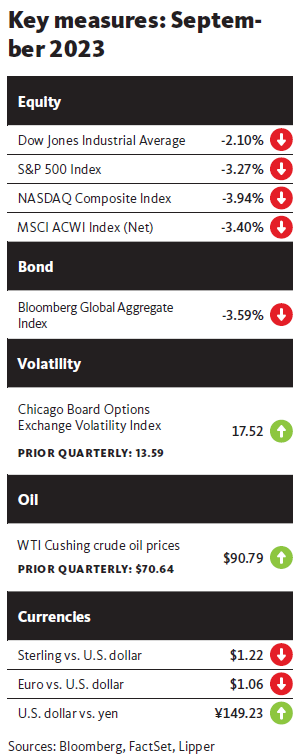

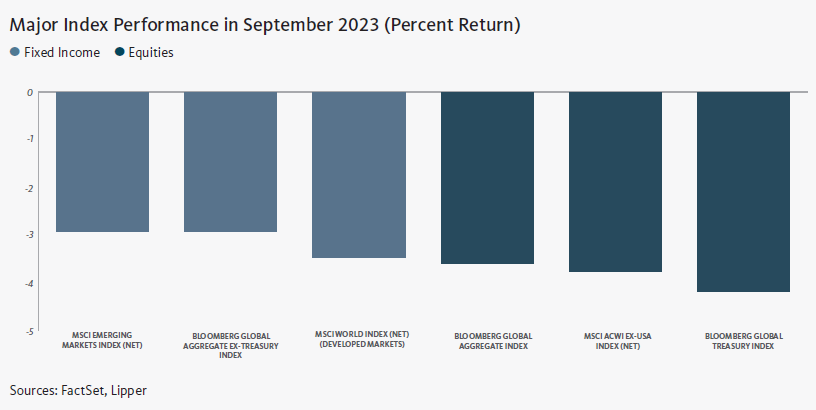

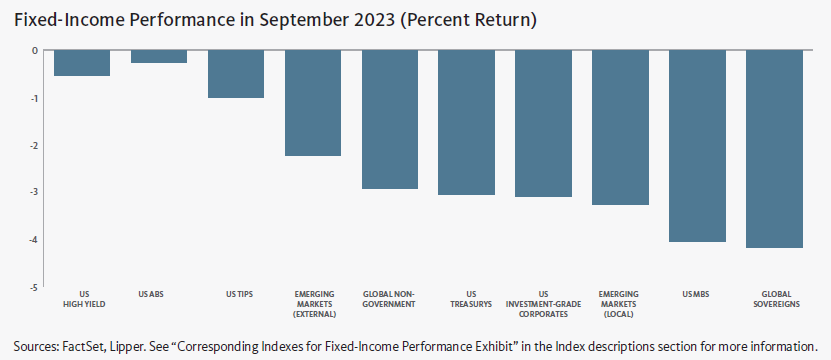

Most global fixed-income asset classes lost ground in the third quarter. However, U.S. high-yield bonds registered positive returns and were the top performers within the U.S. market for the period.2 U.S. corporate bonds, U.S. Treasurys, and mortgage-backed securities (MBS) declined.3 Treasury yields moved higher across all segments of the yield curve, particularly one- and two-month bills (bond prices move inversely to yields). According to the U.S. Department of the Treasury, yields on the 2-, 3-, 5- and 10-year Treasury notes rose 0.16%, 0.31%, and 0.47%, respectively, over the quarter. The spread between 10- and 2-year notes moved from -1.06% to -0.62% during the period, and the yield curve remained inverted.

Global commodity prices generally moved higher during the quarter. The West Texas Intermediate (WTI) crude-oil spot price and the Brent crude oil price climbed 28.5% and 23.7%, respectively, in U.S. dollar terms, on expectations that production output cuts from the Organization of the Petroleum Exporting Countries (OPEC) and Russia would continue through the end of 2023. The New York Mercantile Exchange (NYMEX) natural gas price rose 5.6% over the period, benefiting from strong demand due to record-high temperatures in the U.S., particularly in the southwestern region of the country. Conversely, the 3.3% decline in the gold spot price for the quarter was attributable to strength in the U.S. dollar. Wheat prices fell 16.8% over the period, hampered by Russia’s shipments of large quantities of cheaply priced grain.4

Economic data

U.S.

- The Department of Labor reported that the U.S. consumer-price index (CPI) rose 0.6% in August, following a monthly increase of 0.2% in July. The CPI advanced 3.7% year-over-year—up from the 3.2% annual rise in July. However, the 4.3% annual increase in core inflation, as measured by the CPI for all items less food and energy, represented a 0.4- percentage point decline from the 4.7% year-over-year upturn in July. Core inflation rose 0.3% month-over-month in August, following a 0.2-percentage point uptick in July. The government noted that more than half of the month-over-month increase in the overall CPI was attributable to higher gasoline prices, which climbed 10.6% in August. Housing costs also contributed to the upturn in inflation for the month. Food prices rose 0.2% in August, matching the previous month’s increase.

- According to the third estimate from the Department of Commerce, U.S. gross domestic product (GDP) grew at annualised rate of 2.1% in the second quarter of 2023, unchanged from the government’s second estimate released in August, and down 0.1 percentage point from the 2.2% rise in the first three months of the year. The largest increases for the second quarter were in nonresidential fixed investment (purchases of both nonresidential structures and equipment and software), consumer spending, and state and local government spending. These gains offset reductions in exports and residential fixed investment (purchases of private residential structures and residential equipment that property owners use for rentals). The marginal decline in the GDP growth rate for the second quarter compared to the first three months of the year was due to slowdowns in consumer and federal government spending, as well as a decrease in exports.

U.K.

- According to the Office for National Statistics (ONS), consumer prices in the U.K. rose 0.4% month-over-month in August—up sharply from the 0.3% decrease in July. Inflation advanced 6.3% over the previous 12-month period, down marginally from the 6.4% annual upturn in July. Prices for alcohol and tobacco, along with clothing and footwear, were the largest contributors to the rise in inflation in August, while food and alcoholic beverages, and alcohol and tobacco posted the most notable price increases over the previous 12-month period. Core inflation, which excludes volatile food prices, rose at an annual rate of 5.9% in August, down from the 6.4% rise in July.

- The ONS also reported that U.K. GDP dipped 0.5% in July (the most recent reporting period), after rising 0.5% in June, and increased 0.2% over the previous three-month period. Production output decreased 0.7% monthover- month in July, compared to the 1.8% growth rate in June. The services and construction sectors each fell 0.5% in July, versus upturns of 0.2% and 1.6%, respectively, during the previous month.

Eurozone

- Eurostat pegged the inflation rate for the eurozone at 4.3% for the 12-month period ending in September, down 0.9 percentage point from the 5.2% annual increase in August. Prices for food, alcohol and tobacco rose 8.8% in September, but the pace of acceleration slowed from the 9.7% annual rate for the previous month. Energy prices fell 4.7% year-over-year, following a 3.3% decline in August. Core inflation, which excludes volatile energy and food prices, rose at an annual rate of 4.5% in September, down 0.8 percentage point from August.5

- According to Eurostat’s third estimate, eurozone GDP grew 0.1% in the second quarter of 2023, marginal improvement from the flat growth rate in the first quarter, and increased 0.5% year-over-year. The economies of Lithuania and Iceland were the strongest performers for the second quarter, expanding 2.9% and 2.2%, respectively, while Poland’s economy contracted 2.2% during the period.

Central banks

- As previously noted, the Fed maintained the federal-funds rate in a range of 5.25% to 5.50% following its meeting in September. The Fed’s so-called dot plot of economic projections indicated a median federal-funds rate of 5.6% at the end of 2023, unchanged from its previous estimate issued in June, implying that the central bank could opt for an additional 25-basis point (0.25%) increase at one of its two remaining policy meetings this year. The Fed also projected a reduction in the federal-funds rate to 5.1% by the end of 2024—down from its current range of 5.25% to 5.50%, but higher than the central bank’s previous estimate of 4.6%.

- In a split 5-4 vote at its meeting on September 21, the Bank of England (BOE) left the Bank Rate unchanged at a 15-year high of 5.25%. Four BOE Monetary Policy Committee members supported a 25-basis point increase. In its announcement of the pause in its rate-hiking cycle, the BOE noted that “inflation is expected to fall significantly further in the near term, reflecting lower annual energy inflation, despite the renewed upward pressure from oil prices, and further declines in food and core goods price inflation. Services price inflation, however, is projected to remain elevated in the near term, with some potential month-to-month volatility.”

- The European Central Bank (ECB) increased its benchmark interest rate by 0.25% to 4.25% following its meeting in mid-September. In a statement announcing the rate hike, the ECB’s Governing Council noted, “Inflation continues to decline but is still expected to remain too high for too long… [We] will continue to follow a data-dependent approach to determining the appropriate level and duration of restriction. In particular, the Governing Council’s interest rate decisions will be based on its assessment of the inflation outlook in light of the incoming economic and financial data, the dynamics of underlying inflation, and the strength of monetary policy transmission.” Additionally, the ECB lowered its economic projections, and currently forecasts that the eurozone economy will expand by 0.7% in 2023, 1.0% in 2024 and 1.5% in 2025.

- The Bank of Japan (BOJ) left its benchmark interest rate unchanged at -0.1% following its meeting on September 21-22. In a statement announcing the rate decision, the central bank commented, “Japan’s economy has recovered moderately. The pace of recovery in overseas economies has slowed. Although exports and industrial production have been affected by the developments in overseas economies, they have been more or less flat, supported by a waning of the effects of supply-side constraints.” During its previous meeting in late July, the central bank set a rigid upper yield limit of 1.0% for the 10-year Japanese government bond (JGB). The 10-year JGB yield rose 37 basis points to 0.77% over the quarter.

SEI’s view

While predictions of a downturn in business activity during 2023 have been widely held since the end of last year, the U.S. economy has mostly surprised to the upside. Recession calls are now in the minority, with the latest plane analogy going from “hard landing” to “soft landing,” and even to “no landing.” Strong July results for retail sales, services consumption, industrial production, and housing starts resulted in the inflation-adjusted gross domestic product reaching an annualised 5.9% rate of gain in August. We do not believe this trend is sustainable. Although the consensus has swung away from this view, there is a reasonable probability of a recession in 2024.

Other major economies outside the U.S. are showing signs of weakness, despite advances during the first half of this year. Germany is already in recession and the U.K. may not be far behind. In these developed economies, businesses and consumers alike are feeling pressure from rising interest rates and persistent core inflation.

Hopes that China would offset slowing growth elsewhere have proven to be elusive. Although Chinese domestic travel and services consumption experienced a post-COVID-19 bounce, the economic data have been mostly disappointing. Consumer sentiment remains extremely depressed, with the latest quarterly reading showing a partial reversal of the early 2023 postlock down bounce. Chinese consumers and financial market participants appear largely unimpressed with the government’s efforts, both fiscal and monetary, to turn the economy around.

Inflation continues to fall as COVID-19-era supply-chain disruptions abate. However, it is SEI’s strong conviction that there has been a regime change when it comes to long-run inflation, and that it will run sustainably higher in the U.S. than the Federal Reserve’s (Fed) 2% target. Structurally tight labour markets, the shifting of global supply chains away from China, higher financing costs, the disruptions caused by the transition to a carbon-neutral regime, and a likely boost in corporate tax rates in the years ahead suggest to us that an inflation rate over 3% is more likely than one under 2%.

The Fed’s rate-hiking cycle is nearing an end, but this does not mean that the federal-funds rate will be moving lower anytime soon. We believe there could be one more interest-rate increase from the Fed, but as labour-market pressures ease, even this appears increasingly unlikely. The latest Federal Open Market Committee projections indicate an intention to keep the federal-funds rate higher for longer. In our view, it is unlikely the central bank will begin cutting rates before the second half of 2024.

Other major central banks are in similar positions. Given Europe’s stubborn inflation and lower policy-rate stance, the European Central Bank may raise its key interest rate once or twice more this cycle. The U.K. is closest to a wage price spiral, which may force the Bank of England to implement a monetary policy that is tighter than it would prefer. Meanwhile, the Bank of Japan is under increasing pressure to start raising its policy interest rate in order to firm up the yen.

Bond yields have risen despite lower inflation rates. We believe markets are responding to the increase in government debt issuance at a time when central banks are adding to supply pressures via quantitative tightening (i.e., selling bonds out of their portfolios).

SEI expects bond yields to remain elevated as investors adjust their expectations regarding the probability of higher-for-longer central bank interest-rate policy. We also believe that the term premium (the excess yield required to offset the additional risk in longer-dated bonds) will turn positive as investors demand compensation for taking on a greater level of uncertainty around future interest-rate risk.

Equity markets have entered a corrective phase. U.S. large-capitalization stocks are expected to trade in a broad range, with the S&P 500 Index currently closer to the upper end of this range. Growth companies with high price-to-earnings ratios are vulnerable to rising bond yields, and more cyclical and economically sensitive names within this cohort could face pressure from declining profit margins.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated.

This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information. Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Not all strategies discussed may be available for your investment.

Information issued in the UK by SEI Investments (Europe) Ltd, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.