Quarterly Market Commentary: Resolutions, Vaccines and New Highs Conclude a Strange Year

Capital markets began the fourth quarter of 2020 at a crossroad: After risk assets capped off the prior quarter with their first monthly loss since rallying in March, a recovery stumbled in mid-October on a global resurgence of COVID-19 cases. However, a sharp early-November advance that coincided with the US presidential election was propelled higher through the end of the calendar year by a series of constructive announcements relating to the effectiveness, approval, and distribution of COVID-19 vaccines.

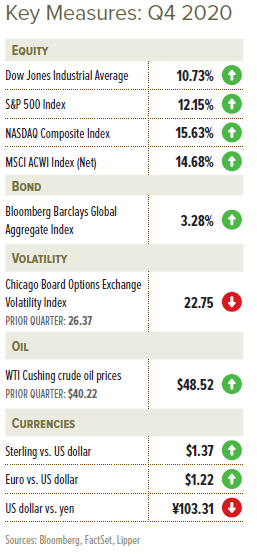

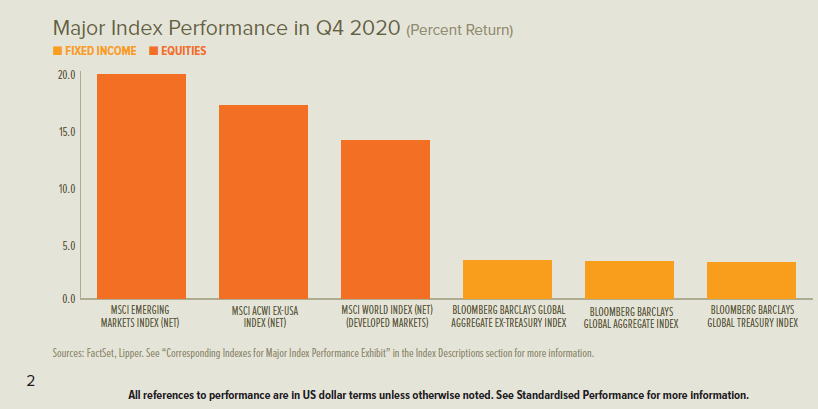

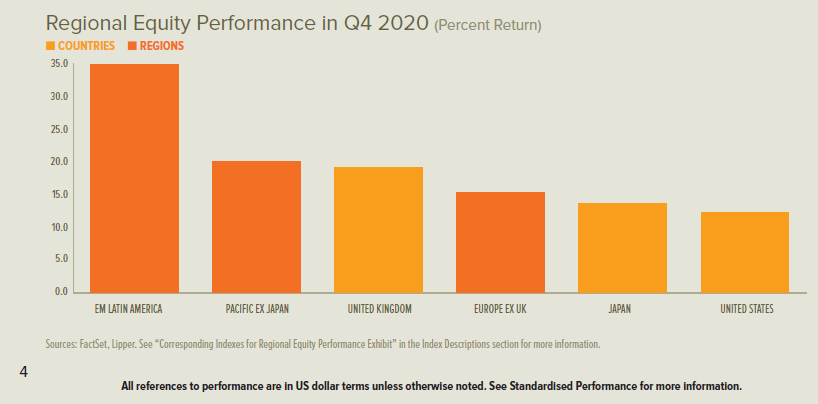

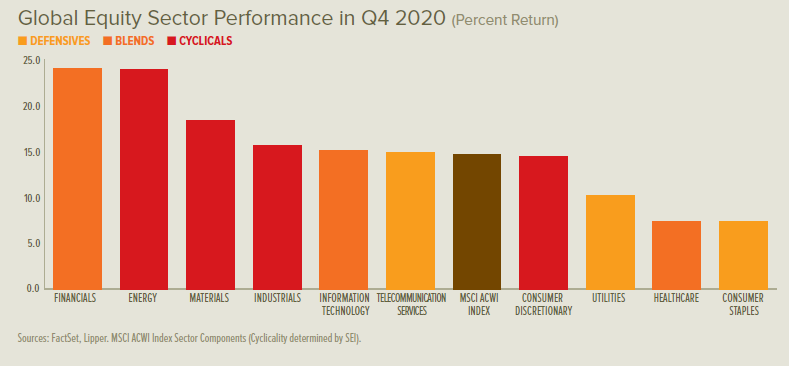

Emerging-market equities outpaced developed markets for the fourth quarter, pushing their full-year performance ahead. UK shares led major developed markets during the quarter, but ended up with a sizeable loss for the 12-month period1. European and Japanese shares followed the UK for the quarter, and both delivered positive returns for the full year; Japan fared much better than Europe in 2020. Meanwhile, US shares had a comparably modest quarter (albeit with a double-digit gain), but had the top major developed-market performance for the year. Sector-level performance was shaken up during the final three months of the year: Energy and financials both had huge rallies after lagging for most of 2020—making them the top performers by a wide margin during the fourth quarter—but still turned in full-year losses.

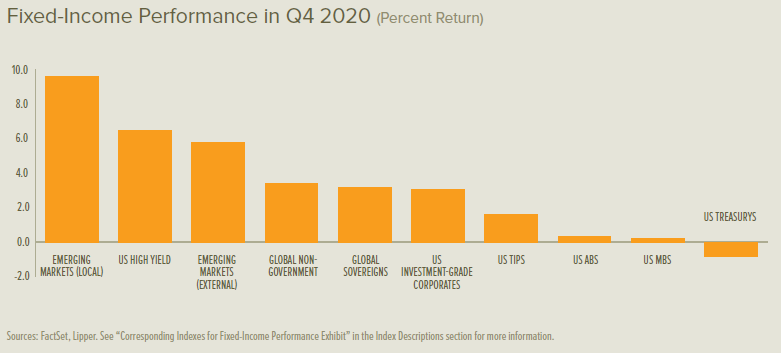

UK and eurozone government-bond rates declined for the fourth quarter. UK rates climbed through October and November before dropping sharply across the yield curve in December. Eurozone rates tumbled across the curve in October, but bounced higher during November and had mixed movements in December—resulting in a steeper overall curve. US Treasury rates generally increased throughout the fourth quarter, with the 10-year Treasury rate rising by more than any other maturity.

The approaching end of 2020 forced a scramble of deal-making on both sides of the Atlantic.

EU and UK negotiators attained a measure of resolution on Christmas Eve with an agreement governing some terms of their ongoing relationship. The EU-UK Trade and Cooperation Agreement contains many of the top priorities of each party:

- The EU was able to maintain its single market while avoiding a hard border in Ireland, while the UK avoided tariffs and quotas on goods traded with the EU.

- The EU agreed to reduce its fishing quota within UK waters by 25% over the next five years, which will be followed by annual negotiations.

- Both parties reserved the right to retaliate after judicial review if they believe the other party has tilted the playing field in an anti-competitive manner. The European Court of Justice will not have jurisdiction over trade disagreements.

Trade in services—which includes the financial industry—was not addressed under the scope of the deal, and each party’s citizens will be subject to visa restrictions when working or travelling for an extended period in the other party’s jurisdiction.

US lawmakers, meanwhile, struck a deal for $900 billion toward pandemic economic relief and $1.4 trillion in federal government funding, which President Trump signed on 27 December. The legislation included the following:

- Another round of forgivable small-business loans under the Paycheck Protection Program, with a $284 billion appropriation

- Extended unemployment payments through March 2021 for approximately 12 million Americans that were on the verge of exhausting their benefits, including a $300-per-week supplement to state-level payments

- Sustained eligibility of unemployment benefits for self-employed, contractors and gig workers, as established under the CARES Act in March 2020

- Preservation of eviction protections to the end of January 2021 and an appropriation of $25 billion to rent relief

Also included in the legislation were direct economic-relief payments of $600 per person to Americans in households below an income threshold—a payment figure that prompted Trump to withhold his signature for several days in favour of a $2,000 disbursement that passed the House of Representatives but never materialised in the Senate.

Earlier in December, the outcome of the US presidential election was formalised when state-level electors cast their votes in accordance with the certified results of each state’s popular vote, delivering a majority of electoral votes to President-elect Joe Biden. A legal campaign to contest the election results waged by President Trump and his allies was mostly retired at that point, although some Republican members of the U.S. Congress sought to object to the counting of electoral votes in early January as a symbolic gesture.

The Regional Comprehensive Economic Partnership (RCEP), a freetrade group composed of 15 Asia-Pacific countries including China, was formalised in mid-November. RCEP nations have a combined population of 2.2 billion people and produce about one-third of global gross-domestic product (GDP), representing the most expansive free-trade area on the planet2.

A sprawling cyberattack against hundreds of organisations—government agencies, corporations and non-government entities—was discovered in December. The targets were centred largely within the US, and several agencies of the federal government reported infiltrations dating as far back as March 2020. Solarwinds Orion software, which is designed to support business technology infrastructure, was the main gateway for the hack apparently perpetrated by Russian intelligence services3.

Economic Data

- UK manufacturing activity continued to grow at a healthy rate throughout October and November before accelerating in December. The UK services sector started the fourth quarter with strong growth that gave way to an outright contraction by November, with activity essentially maintaining pace in December. The overall UK economy grew by 16% during the third quarter after falling by 19.8% in the second quarter; the economy shrank by 8.6% year over year through the end of September.

- Growth in eurozone manufacturing activity remained healthy through October and November before strengthening in December. A contraction in the eurozone services sector deepened from October to November, and then moderated during December. The overall eurozone economy grew by 12.5% during the third quarter after declining by 11.8% in the second quarter; the economy had shrunk by 4.3% year over year through the end of the third quarter.

- US manufacturing growth picked up from a moderately healthy pace in October to stronger levels in November and December. US services sector growth started solidly in October before heating up in November and then reverting back to still-strong levels in December. New US jobless claims bottomed in mid-November, then climbed until mid-December before retreating through year end. The overall US economy grew at a 33.4% annualised rate during the third quarter after declining by an annualised 31.4% in the second quarter.

Central Banks

- The Bank of England’s Monetary Policy Committee expanded its quantitative-easing programme at its early-November meeting, committing a fresh £150 billion toward bond purchases for a total of £895 billion. There were no additional policy changes at its mid- December meeting. The Committee’s latest quarterly report projected that the UK economy would contract by 11% in 2020, a deterioration from the 5.4% contraction estimated a quarter earlier4.

- The European Central Bank (ECB) made no new changes to monetary policy at its late-October meeting. The December meeting produced a decision to increase the scale of asset purchases associated with its Pandemic Emergency Purchase Programme (PEPP) by €500 billion for a total of €1.85 trillion. PEPP purchases were also extended through at least early 2022. Additionally, the ECB planned to expand the use of its Pandemic Emergency Longer-Term Refinancing Operations (PELTRO) programme, which is designed to promote bank lending through subsidised loans.

- The US Federal Open Market Committee (FOMC) made no changes at either its early-November or mid-December meetings. The US Federal Reserve’s (Fed) latest summary of economic projections improved over the prior quarter, with expectations for higher economic growth and lower unemployment in 2021 and thereafter. The US central bank planned to extend four emergency lending facilities that were established in March into the New Year—yet also planned to return $455 billion of unused funding for five other lending facilities to the US Department of the Treasury and shutter the facilities at year end. President-elect Biden named former Fed Chair Janet Yellen as his nominee for US Secretary of the Treasury.

- The Bank of Japan (BOJ) also took no new actions following its late- October and mid-December monetary policy meetings. It will continue to implement all tools associated with its Quantitative and Qualitative Monetary Easing (QQE) with Yield Curve Control programme.

- Separately, the BOJ extended its crisis-response programme’s emergency funding measures by six months.

SEI’s View

We’re all looking forward to a better 2021. From the looks of it, investors have already begun to look beyond the valley.

Recent market chatter has hinted at the notion of a “Great Rotation” in capital markets, suggesting that investors may have begun to favour value and cyclical sectors over growth names. While we have seen some evidence of this, we believe it is too early to tell if this is the beginning of a major secular shift in equity investment themes.

Since September, value style equity indexes have outpaced their growth counterparts to varying degrees across geographies and market capitalizations, most notably within US large caps. We have observed several signs of potential normalisation that seem to support the prospects

for a style regime change.

- In October, US Treasury yields started to tick up. However, we would be surprised if rates moved sharply higher in 2021.

- The development of highly effective COVID-19 vaccines has helped investors shake off worries that the pandemic would last indefinitely.

- Regulatory developments in both the US and abroad have hinted that the dominance of large technology companies may no longer be as straightforward, long-lasting or profitable as some investors have grown accustomed.

No one knows if this shift is, in fact, a Great Rotation, but we think investors will prove willing to shrug off the likely prospect of more bad news during the difficult months that lay ahead, which could include slowdowns or pauses in vaccine manufacturing, distribution, administration and uptake.

Politics will also come into play, and can either act as a tailwind or a headwind. The US Congress struggled for months trying to get additional income support to the people and businesses most seriously affected by the economic disruptions politicians caused by the virus. They finally

came up with a $900 billion compromise that is limited in scope and falls far short of what is needed. Most of the benefits are set to expire in March and April, and it does not address revenue shortfalls facing state and local governments.

Policy depends on personnel, and there is no disputing the priorities of a Biden administration will be quite different from those of the Trump era. One of the most important nominations put forth by President-elect Biden is that of former Fed Chair Janet Yellen as Treasury Secretary. A close working relationship between the Treasury and the Fed will probably be reassuring for investors in the near term since there is little doubt that the central bank will continue its extraordinary efforts to support the economic recovery in 2021.

Casting our focus across the Atlantic, the last-minute Brexit deal provided a Christmas gift of sorts, at least in terms of removing a degree of uncertainty. While a skinny deal is better than none, the UK’s long period of intense uncertainty continues to a degree, as the deal addressed the transfer of goods but not commerce in services.

Barriers to trade introduce economic inefficiencies. Post-Brexit, UK prices will likely move a bit higher, GDP a bit lower and supply chains a bit more unreliable.

Looking at the forward price-to-earnings ratio of the MSCI United Kingdom, MSCI Europe ex-U.K. and the MSCI USA Indexes, we can see that the US market has consistently traded at a premium valuation over the past 15 years.

That premium has widened since 2017 and expanded significantly further in 2020. The other two markets have mostly traded at similar valuations to each other over time—but major divergence began to develop in 2019 and became more pronounced in 2020.

UK equity valuations, in our opinion, reflect much of the bad news. Maybe it is time to for investors to think about the things that could go right:

- First, of course, is the development and distribution of vaccines, which are expected to drive the global economy to higher ground in 2021. This should benefit the large energy, materials and industrial multinationals that make up nearly one-third of the market capitalisation of the MSCI United Kingdom Index.

- The country also appears competitive versus other advanced countries when measured by various benchmarks, such as relative unit labour costs.

- The government’s trade negotiators have already fanned out across the world to make sure that the UK retains the same trade agreements that it has enjoyed as a member of the EU.

- Prime Minister Boris Johnson has backed away from his attempt to renege on the Withdrawal Agreement that allows Northern Ireland to trade without border restrictions with Ireland and the rest of the EU. This decision saves a lot of headaches, especially with the incoming Biden administration having threatened to impose trade sanctions if the treaty was abrogated.

Like so many other relationships in the equity market, the underperformance of the eurozone benchmark has been going on for a long time. The European economy is more cyclical, value-oriented and less dynamic than the US economy. But that certainly does not prohibit a rebound in performance against the US stock market at a time when the latter appears to be excessively tilted toward technology stocks, the US dollar is weakening and a global economic recovery is at hand.

The pandemic has had one good outcome for Europe. It finally forced Germany and other fiscal “hawks” to allow an expansion in fiscal policy. This move away from budgetary austerity should be viewed in context. Most countries have experienced a sharp rise in red ink this year, and

the biggest deficits are outside the eurozone. The Europeans probably can afford to run higher deficits than the International Monetary Fund appears to be pencilling in for 2021. Italy almost certainly will. The memory of the European periphery debt crisis is still fresh in the minds of many policymakers who realise that pushing for fiscal austerity measures prematurely would probably be a mistake.

On the other hand, we think there is a greater need for other countries outside the eurozone to regain control of their finances. If those countries fail to do so, Europe could be the beneficiary of investment flows that would further prop up the euro and equity valuations.

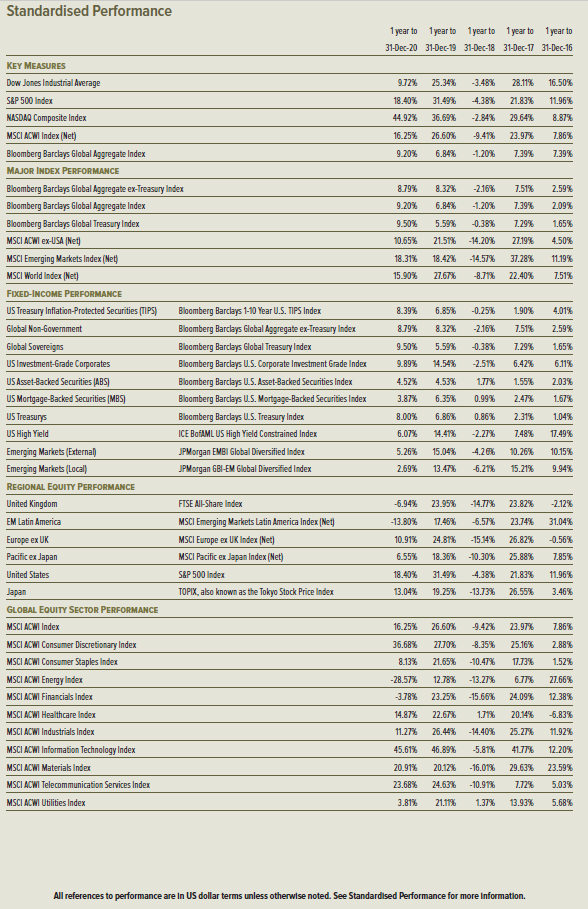

Emerging-market equities have been on a tear since they bottomed out last March. For 2020 as a whole, the MSCI Emerging Markets Index (total return) climbed by 18.3%—slightly better than the 15.9% gain registered by the MSCI World Index (total return), which tracks the performance of developed-country stock markets.

However, the MSCI Emerging Markets Index is still just above its previous high-water mark recorded in January 2018. Frontier markets have fared even worse. The MSCI Frontier Emerging Markets Index (total return) has yet to surpass its most recent pre-pandemic high level recorded last January.

Fortunately, not only has the combined firepower of global central banks prevented a liquidity crisis, it has also driven borrowing costs down to near record lows even as total emerging-market debt exceeds 200% of GDP. Only two problem debtors—Argentina and Turkey—had to increase their interest rates in recent months to stem investment outflows. As the world returns to normal, other nations may need to raise rates in order to attract sufficient investment inflows to sustain their fiscal and current-account positions.

A weak US dollar is an important catalyst for emerging-markets performance. Although the currency has weakened meaningfully this year and pushed emerging-market equities higher, the performance of emerging markets relative to developed markets has been in a narrow range. We expect the coming year will see emerging equities’ relative performance improve, partly because the US dollar should continue to weaken.

If the world economy enjoys a durable cyclical recovery in 2021, the dollar should continue to fall. This would also bolster the rebound in commodity prices. Commodities of all sorts have been moving sharply higher since the spring, with metals, raw industrials and foodstuffs rallying together for the first time since the 2009-to-2011 period.

Signs of a recovery should continue to reveal themselves as COVID-19 abates and economic activity normalises. In the meantime, fiscal spending and accommodative central-bank policy should prop up inflation. As the market prices in these developments, “long-duration” growth and

expensive high-profitability stocks should be pressured—while momentum investors are likely to rotate into new themes, potentially adding more fuel to this nascent cyclical rally.

Glossary of Financial Terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to rise) and investor confidence is high.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Pandemic Emergency Longer-Term Refinancing Operations (PELTROs): PELTROs are a series of longer-term refinancing operations intended by the ECB to ensure sufficient liquidity and smooth money market conditions during the COVID-19 pandemic period. PELTRO operations are planned to be allotted on a near-monthly basis maturing in the third quarter of 2021.

Pandemic Emergency Purchase Programme (PEPP): PEPP is a temporary asset purchase programme of private and public sector securities established by the ECB to counter the risks to monetary policy transmission and the outlook for the euro area posed by the COVID-19 outbreak.

Paycheck Protection Program: The Paycheck Protection Program is a loan offer by the U.S. government’s Small Business Administration (SBA) designed to provide a direct incentive for small businesses to keep their workers on the payroll. SBA will forgive loans if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.