Quarterly Market Commentary: Recovery Rolls On as COVID Rate Climbs

Global equity markets delivered another quarter of outsized gains, moving further from the March 2020 lows as the economic recovery that took hold in the second quarter continued throughout the summer.

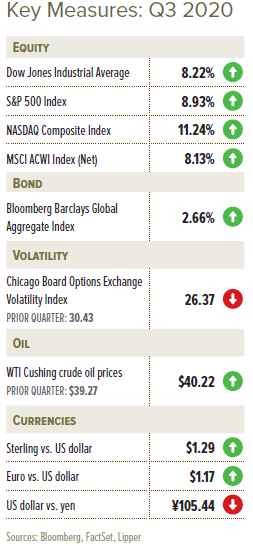

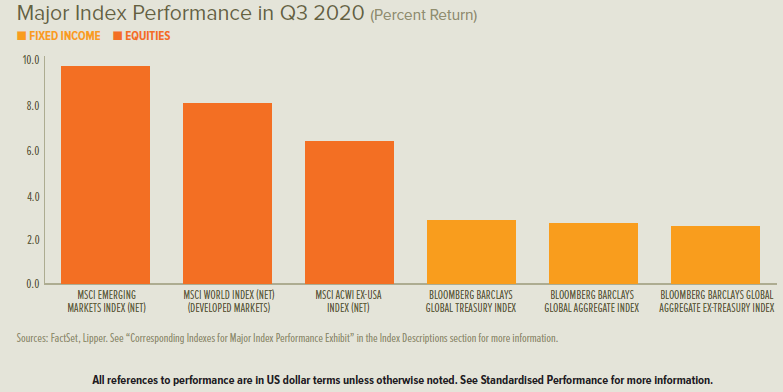

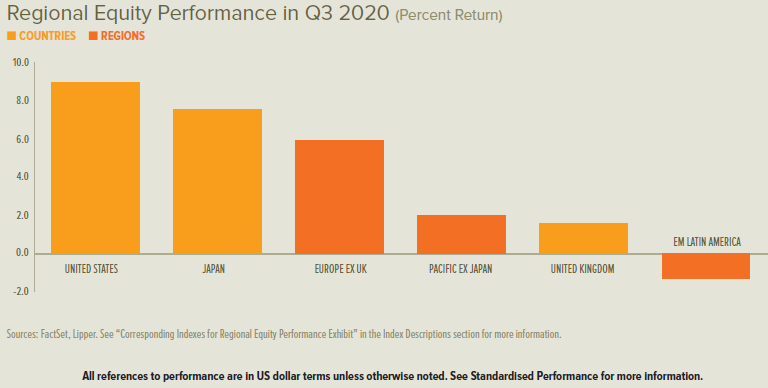

European shares moved higher over the full quarter with relative consistency, while UK equities were flat in July, higher in August and flat again in September (finishing lower in sterling but higher in US dollars). US shares climbed steadily for the first two months of the quarter until peaking at the start of September and mostly declining for the remainder of the period. Japanese equities advanced for the majority of the third quarter, while Chinese shares jumped in early July and finished the quarter with strong performance. Hong Kong equities also started July in a rally, but finished the third quarter on a downbeat after selling off in September.

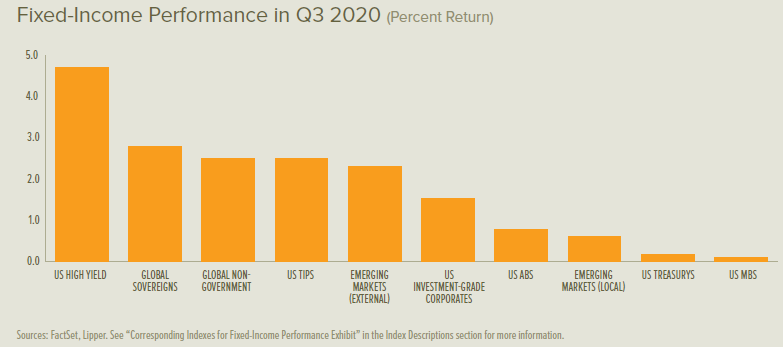

UK government-bond rates increased across most maturities during the third quarter. Eurozone government-bond rates generally decreased, although shorter-term rates were mixed in both markets. Short-to-intermediate-term US Treasury rates declined and long-term rates increased, resulting in a steeper yield curve. The US dollar continued to decline versus a broad trade-weighted basket of foreign currencies throughout most of the third quarter before beginning to recover in a mid-September reversal.

The number of people infected with COVID-19 in European countries continued to rise throughout the third quarter after having reached low points in June and July. Spain saw the earliest resurgence and ended the period with a greater percentage of its population infected than that of any other country in the region, followed first by France and then the UK. Upticks in Italy and Germany have been much more subdued. Meanwhile, the percent of infected US residents peaked in late July—already nearly matching the high point Spain would reach two months later—and continued to fall through mid-September before rising once again by quarter’s end.

Prime Minister Boris Johnson announced in late September new restrictions in England on pubs and restaurants, transportation, and group gatherings as COVID-19 cases in the UK climbed to their highest levels since the spring. At the end of the same month, the UK House of Commons voted for passage of an internal market bill that contradicts the Brexit divorce agreement. Johnson argued that the powers granted by the bill would allow the UK to override EU attempts to shut down trade between Northern Ireland and other parts of the UK. An amendment to the bill would require the government to gain parliamentary approval for any changes to commitments in the divorce agreement, representing a concession on the government’s behalf. Nevertheless, the EU announced it would pursue legal remedy given the bill’s contradictions with the Brexit agreement, even as trade negotiations continued.

US companies announced a large wave of layoffs for workers that had been furloughed earlier in the year as the quarter concluded. Employers in the worst-affected industries—airlines, travel accommodation, sports, entertainment, retail and education—have generally run short of resources after depleting the Paycheck Protection Program loans that were helping to support workforce retention. Prospects for additional fiscal stimulus dimmed amid election-season politics, with Democrats and Republicans holding firm on their respective funding demands. However, the US Congress did pass a resolution on the last day of the third quarter to continue funding the federal government through mid-December, avoiding a government shutdown.

Japan’s ruling Liberal Democratic Party selected Yoshihide Suga to succeed Prime Minister Shinzo Abe, who resigned during the quarter due to health issues. Elsewhere in Asia, China-Taiwan tensions flared around a high-level US government official’s visit to Taiwan; China was angered by what it saw as one of its territories assuming sovereignty by inappropriately conducting international diplomacy. Chinese planes made a show of force to coincide with the visit, prompting Taiwan to quickly mobilise its military jets. The island’s government had previously condemned nearby Chinese military drills as provocations. In Beijing, a military spokesman accused Taiwan’s ruling Democratic Progressive Party of “collusion” with the US, and said the US is trying to “use Taiwan to control China.”

The foreign ministries of China and India issued a joint statement in September declaring their intent to deescalate a territorial conflict that began in the spring along their Himalayan border.

US technology company Oracle and retailer Walmart won a joint bid in September to serve as trusted technology partners of TikTok’s US operations and, in order to appease US national security concerns, gain full access to TikTok’s source code. However, under the current proposal, Chinese parent company ByteDance will retain an 80% stake despite the Trump administration having sought majority ownership for the US companies. A US judge temporarily blocked an executive order signed by Trump to ban downloads and updates for TikTok and other popular Chinese apps beginning in September.

The Trump administration announced in September that it would not pursue a 10% tariff on US imports of Canadian aluminium previously announced in August, as trade is now expected to normalise in the coming months following high import levels earlier in 2020.

Israel normalised relations with the United Arab Emirates and Bahrain in early September in a US-brokered agreement that is expected to result in the mutual establishment of embassies and increased regional trade between the US allies.

The EU imposed sanctions on a “substantial number” of Belarusian officials in response to fraud and violence associated with the 9 August election victory that awarded President Alexander Lukashenko his sixth term after 26 years in power. EU leaders declared that the election—which Lukashenko was said to have won with 80% of the vote despite large, ongoing protests—would need to be rerun as it was “neither free nor fair.”

Armenia and Azerbaijan renewed a long-simmering conflict centred on control of the Nagorno-Karabakh region. Beginning in July, Armenia announced joint defence programmes with Russia—which Azerbaijan countered via military exercises with Turkey. Both sides accused the other of employing fighters from other regional conflict zones. By the end of September, skirmishes yielded to outright battles during which Armenia claimed Turkey shot down an Armenian fighter jet in Armenian airspace.

Economic Data

- UK manufacturing activity cooled a bit in September after returning firmly to growth territory in July and peaking in August. The UK services sector started the third quarter with solid growth, which heated up in August before settling back to a slower, but still-healthy expansion in September. The number of people claiming UK unemployment benefits drifted higher by 2.8% between July and August, reaching 2.7 million. The overall UK economy contracted by 19.8% during the second quarter and 21.5% year over year, slightly less than recorded by earlier estimates.

- A sluggish recovery in eurozone manufacturing activity through July and August warmed to healthier levels in September. Activity in the services sector plunged from a solid expansion at the start of the quarter to an outright contraction by September. Loans to non-financial European corporations grew steadily through July and August, at 7.0% and 7.1%, respectively, continuing a trend that began in April. The eurozone unemployment rate increased through August, jumping to 8.1% from 7.9% in July.

- The recovery in US manufacturing steadily progressed during the third quarter, ending in a solid overall expansion punctuated by strong new orders and steady employment. Services sector activity climbed out of contraction in July and returned to a healthy expansion by August, where it levelled off through September. New weekly claims for unemployment benefits declined modestly throughout the quarter, but remained above levels that were unprecedented before COVID- 19-induced lockdowns. The overall US economy contracted at a 31.4% annualised rate during the second quarter, improving a bit on preliminary readings.

Central Banks

- The Bank of England’s (BoE) Monetary Policy Committee held the Bank Rate at 0.1% throughout the third quarter after announcing at the end of the second quarter that it would expand its stock of asset purchases to £745 billion. Committee members have debated the implications of employing a negative interest rate at recent meetings.

- The European Central Bank (ECB) held its benchmark rates unchanged during the third quarter. ECB President Christine Lagarde expressed an expectation that the central bank’s Pandemic Emergency Purchase Programme (PEPP)—which was granted a higher ceiling for asset purchases in June that totalled €1.35 trillion—would need to be fully employed given the current outlook.

- The US Federal Open Market Committee (FOMC) kept the federal-funds rate near zero during the third quarter. During July, the Federal Reserve (Fed) Board of Governors announced extensions of temporary US dollar-liquidity-swap and repurchase-agreement facilities with other central banks through March 2021. In August, the FOMC introduced a new average inflation target that would allow above-target inflation following periods of below-target inflation. This change indicates that the FOMC will likely let the US economy run hotter than in the past before taking policy action to temper growth. At the end of September, the Fed announced it would extend an order through the fourth quarter of 2020 for large banks to cut dividends and halt stock buybacks given expectations for a higher rate of loan defaults.

- The Bank of Japan (BOJ) held course throughout the third quarter. Notably, newly elected Prime Minister Suga has expressed a desire to see more Japanese bank mergers on the belief that it is a crowded marketplace.

SEI’s View

It has already been an eventful and exhausting year, but we have a sense that the next few months could prove critical to the future course of the global economy and financial markets. Most countries were in V-shaped recovery mode during the third quarter, moving sharply off their low points in May and June. We assume that future lockdowns to contain COVID-19 outbreaks will be far more limited in scope. For developed countries, treatments have improved, vulnerable populations appear to be better-protected, and younger, generally healthier people are accounting for a much larger share of confirmed new cases.

But we doubt there will be a full return to normal economic behaviour until safe and effective vaccines are introduced and distributed globally. The news on this score has been positive, and probably is a key reason for the continued buoyancy of equities and other risk assets. According to the World Health Organization, researchers were testing 38 vaccines in clinical trials at the end of September, while 93 more were in pre-clinical testing.1 Ten vaccines have been approved for large-scale efficacy and safety trials. We think it is realistic to assume that a few different vaccines will be generally available by this time next year, which means that social distancing measures must still be followed well into 2021 and, most likely, into 2022.

There’s no disputing that US economic activity remains far below normal. Although incomes are now recovering as more people get back to work, the lack of additional income support may drag down consumer spending as we head into the end of the year. Business sentiment appears to have bottomed, but the outlook remains sufficiently uncertain to keep us in a watch-and-wait mode. We would not be surprised to see the official US unemployment rate move up in the months ahead as hard-hit industries eliminate jobs now that government support has run out.

In August, Fed Chairman Jerome Powell officially unveiled a new framework for conducting the central bank’s monetary policy. The Fed has decided to see how low the US unemployment rate can get before it causes the inflation rate to exceed the 2% mark by a meaningful extent. The FOMC’s own inflation projection does not envision a return to 2% inflation until the end of its forecast window in 2023, so it may be a long time before the federal-funds rate rises.

In our view, all that’s really left in the Fed’s monetary toolbox is quantitative easing, along with the provision of lifeline support to corporations as well as state and local governments through its various credit facilities. Monetisation of debt will likely continue until the pandemic crisis is well past and the US unemployment rate approaches its previous lows.

The US presidential election will have a major impact on the economy and financial markets in the months and years ahead. Still, we firmly believe that it would be a mistake to pursue even a short-term investment strategy that necessitates accurately predicting: (1) the election winner; (2) the policies proposed by the newly inaugurated president; (3) the ways in which Congress will modify those proposals throughout the legislative process; or (4) the impact those new laws would have on the economy and financial markets.

Regardless of the election’s outcome, we assume that both candidates would see their platforms tempered before they’re put into practice. There is a high degree of institutional inertia, which is partly deliberate (constitutional checks and balances) and partly happenstance (increasing polarisation of opinion in the country tends to favour a draw). While there could be some market volatility plausibly attributed to the election, it is usually best to pay strict attention to the fundamentals and to ignore the politics.

The UK is undergoing its own unique political melodrama, with Prime Minister Boris Johnson facing a rebellion among his own backbenchers and intense criticism from senior Conservatives over his proposal to renege on the withdrawal treaty that would allow Northern Ireland to trade without border restrictions with Ireland and the rest of the EU. The move to abrogate the treaty, if successful, would almost certainly lead to a hard Brexit—a reversion to the World Trade Organization’s most-favoured-nation trading rules with the EU. It also could breathe new life into the separatist movement in Northern Ireland itself, not to mention Scotland.

Prime Minister Johnson’s decision reflects his government’s frustration with EU negotiators. There are two main sticking points, one small (EU fishing industry demanding full access to UK waters) and one large (EU demanding the UK’s continued adherence to EU strictures on government financial assistance to private-sector businesses).

Obviously, a hard Brexit will not help matters. But the worst impact potentially will be sustained by financial companies and other service producing entities, since World Trade Organization rules deal mostly with tradable goods. The increase in tariffs, for the most part, will be bearable once border-related issues are worked out. In the meantime, the UK and the rest of Europe are facing a second wave of COVID-19 that could turn what’s been a V-shaped recovery into something looking more like a W.

This year’s pandemic and postponement of the summer Olympics proved to be a bitter ending to Japanese Prime Minister Shinzo Abe’s record breaking term in office. His push to lift Japan out of its deflationary spiral was somewhat successful. Prices mostly stopped declining in the aggregate, but there were few occasions when overall consumer-price inflation rose above 1%. Pandemic pressures have caused a return to outright deflation in recent months.

In our view, it is unlikely that radical changes will be made to the direction of policy under Japan’s new Prime Minister Yoshihide Suga. In the nearterm, the priority will be on the response to the coronavirus; fiscal policy will remain quite expansionary. The Bank of Japan will continue to buy most of the government-issued bonds, along with other types of corporate debt and equity, as it has been doing as part of its Quantitative and Qualitative Easing program over the past four years.

The contrast of the big Asian stock markets versus other large emerging market equities is dramatic. China’s strong gains can be chalked up to its rebound in economic activity. Although travel and other services are still constrained due to lingering concerns about the virus, infrastructure related spending and manufacturing have experienced an almost-complete recovery to pre-pandemic levels. Investors seem to be unfazed by the deterioration in the US-China economic relationship or by the increasingly fraught diplomatic relations between China and other countries.

Emerging markets are already showing some good news. The price of raw industrials bottomed in early May, and have since enjoyed a sharp move higher. If industrial commodity prices advance in a sustained, multi-year fashion as they have in previous cycles, it’s a good bet that emerging market corporate profits will also rise sharply.

Our optimism is somewhat tempered by the rising debt burden facing many emerging countries. Much of the increase in emerging-market debt has been tied to the corporate sector—especially in China, where private domestic, non-financial debt has reached an eye-watering 216% of GDP2. Of more concern are the mostly small-to-medium-sized countries that are running current-account deficits and are too dependent on external hard-currency debt, or do not have the reserves to easily cover their debt service.

The actions of the world’s major central banks back in March, especially the US Fed’s provision of US dollar liquidity, have helped to ease the strain on the market for emerging-country debt. Governments and other official lenders, meanwhile, have granted loan forbearance to nearly 80 countries; it’s a tougher job to get private creditors to agree to do the same. Nonetheless, emerging-market sovereign yields on dollar-denominated debt have fallen back toward their previous record lows, more than reversing the spike endured in March, prior to the Fed’s rescue operations.

Glossary of Financial Terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to rise) and investor confidence is high.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Pandemic Emergency Longer-Term Refinancing Operations (PELTROs): PELTROs are a series of longer-term refinancing operations intended by the ECB to ensure sufficient liquidity and smooth money market conditions during the COVID-19 pandemic period. PELTRO operations are planned to be allotted on a near-monthly basis maturing in the third quarter of 2021.

Pandemic Emergency Purchase Programme (PEPP): PEPP is a temporary asset purchase programme of private and public sector securities established by the ECB to counter the risks to monetary policy transmission and the outlook for the euro area posed by the COVID-19 outbreak.

Paycheck Protection Program: The Paycheck Protection Program is a loan offer by the U.S. government’s Small Business Administration (SBA) designed to provide a direct incentive for small businesses to keep their workers on the payroll. SBA will forgive loans if all employees are kept on the payroll for eight weeks and the money is used for payroll, rent, mortgage interest, or utilities.

Quantitative easing: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy.

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.