Quarterly Market Commentary: Policies Provide Economic Life Support

The modern world has almost never before seen the kind of sudden, dramatic global transformation as it did in early 2020. The New Year brought major developments that included the UK’s official divorce from the EU, the signing of a “phase-one” trade deal between the US and China, and the emergence of COVID-19 in Wuhan, China. February was defined by the world’s evolving realisation that COVID-19 would not be contained to China despite quarantines, border closures and air-travel restrictions. Halfway into the same month, Europe and the US began to contend with a possible widespread outbreak that would demand extreme containment measures—all of which became reality by the middle of March, as both regions committed to suppression.

The arc of global financial markets during the first quarter of 2020 corresponded with the unfolding realisation that controlling the outbreak would require government-mandated shutdowns of “non-essential” activity—impacting large cross-sections of the world economy. Governments issued stay-at-home orders as public health leaders preached “social distancing” in order to “flatten the curve” (that is, slow the rate of transmission in order to provide health systems time to manage the viral outbreak).

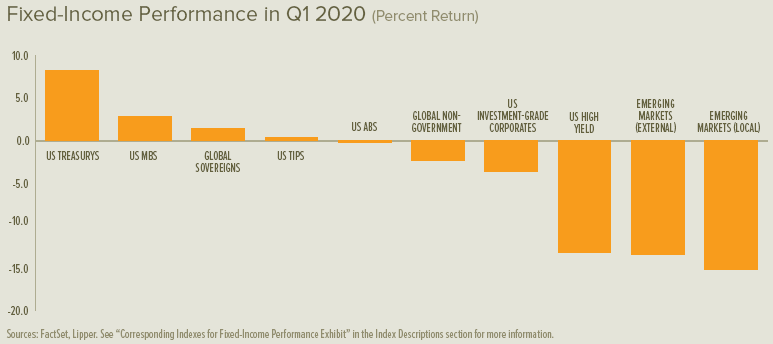

A dash for cash by investors concerned about the economic fallout created disorderly conditions across capital markets. Major developed government-bond rates plummeted to multi-year and all-time lows as credit spreads exploded for fixed-income securities regardless of credit quality, maturity, or other risk characteristics (yields and prices move inversely).1 A subsequent shortage in US dollar funding caused its value to spike against other currencies. Emerging-market currencies came under heavy pressure amid investment outflows and collapsing output, partially on US dollar scarcity and withering demand for oil (much of which is produced in emerging-market countries).

The US Federal Reserve (Fed) and other major central banks responded to the widespread disorder in March with a rapid return to great financial crisis-era playbooks. This appears to have helped reroute markets back toward orderly function.

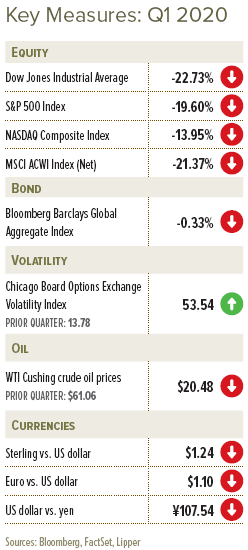

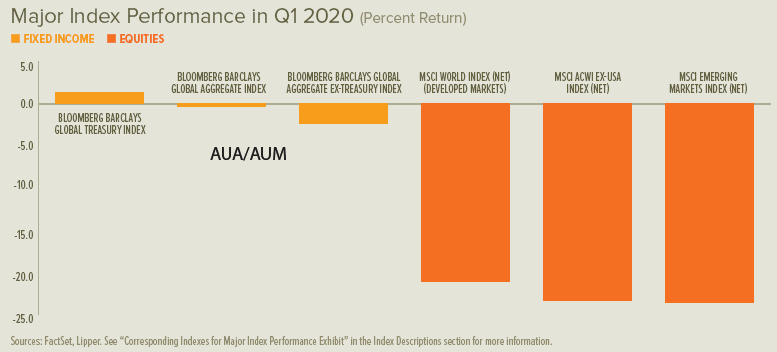

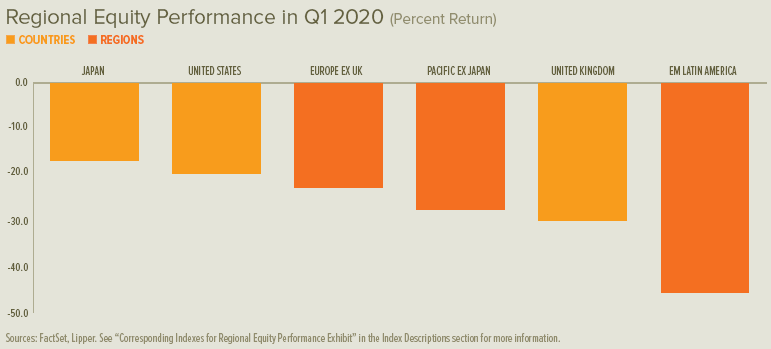

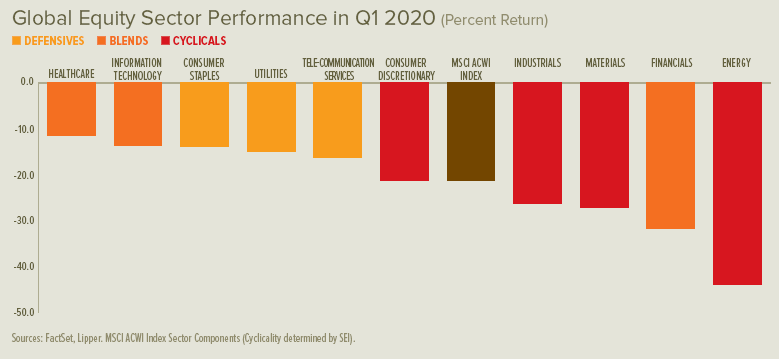

Equities in developed and emerging markets around the globe tumbled in the first quarter of 2020—by between approximately 20% and 30% in most major equity indexes. Peak-to-trough declines were even sharper in many areas since most shares outside of China either climbed or remained buoyant through mid-February, before daily volatility returned to levels last seen during the depths of the great financial crisis.

Dysfunction, unfortunately, was not limited to financial markets. Hospitals in European and US population centres reported shortages of medical supplies and personal protective equipment. Overextended health systems buckled under the strains; a scarcity of hospital beds spurred the construction of temporary field hospitals, from Milan’s fairgrounds to London’s ExCel Centre and Central Park in New York City. As the Western world was scrambling to build these facilities, China was already dismantling its temporary hospitals as the country’s infection rate slowed—closing its last just one day before the World Health Organization officially characterized COVID-19 a pandemic.

Economic fallout from widespread societal lockdown presented a separate severe challenge to governments around the globe. Trends that were many years in the making—including the explosion of online spending hurting brick-and-mortar retailers, the rise of video streaming entertainment at home, and the expanded business use of teleconferencing—accelerated due to the shift. Meanwhile, OPEC+ (that is, the Organization of the Petroleum Exporting Countries, led by Saudi Arabia—plus Russia) splintered in early March on plummeting demand. Russia would not agree to a proposed shared production cut intended to stabilise oil prices, which prompted Saudi Arabia to increase production in retaliation—triggering the largest one-day oil-price decline since 1991 on 8 March, sending oil prices to their lowest levels in 18 years.2

National government responses evolved sharply over time. The UK appeared intent on letting its population develop “herd immunity” through widespread infection in early March, acknowledging the likelihood of a high mortality rate. By mid-March, however, its government pivoted to suppression—closing most gathering places and recommending the postponement of local elections several months in advance. The country’s economic relief plans included replacing most of the income lost to suppression-related unemployment, additional health funding, faster paid sick leave and unemployment benefits, business relief via subsidized loans, and the refunding of sick pay to small firms.

In the US, the COVID-19 response differed at the state level, with governors of more than 30 states (who collectively represent over two-thirds of the national population) issuing stay-at-home orders by the end of the quarter, while others abstained from substantive lockdown measures. The number of Americans filing for unemployment benefits in the last full week of March hit a record-shattering high of 6.64 million, just one week after more than quadrupling the 1982 record of 695,000 jobless claims. President Donald Trump initially appeared to consider the outbreak a minor issue, but then shifted course, declaring a national emergency in mid-March and then eventually suspending import tariffs, enlisting the private sector to manufacture medical supplies, pausing evictions and foreclosures of government-sponsored mortgages, suspending government-sponsored student loan payments, and delaying most federal tax payments for three months. Congress passed three separate legislative acts appropriating more than $2 trillion in funding for large and small businesses, enhanced unemployment benefits, direct payments to Americans, state and local governments, and the health system.

The European Commission waived Maastricht limits (that is, requiring EU members to adhere to annual deficits of no greater than 3% of gross domestic product) in order to provide national governments fiscal budgetary flexibility. Italy passed one of the earliest government relief programmes, although it will almost certainly need to do more given the severity of its outbreak. Germany and France, among other nations, have also been working to introduce major fiscal stimulus.

Against the backdrop of an unfolding global crisis, Russia’s legislature and highest court affirmed a constitutional amendment allowing Vladimir Putin to remain president until 2036, adding another potential 12 years to his term.

Central Banks

- The Bank of England’s (BoE) Monetary Policy Committee cut the Bank Rate to 0.1%, the lowest in the 325-year history of the lending rate.3 It also announced a £200 billion asset-purchase programme, mostly of government bonds, to be conducted at a monthly pace that will eclipse previous rounds of quantitative easing (QE). Additionally, it has launched a so-called funding-for-lending scheme to spur banks to lend to small- and medium-sized enterprises, as well as a commercial paper facility, with no cap limit, to be financed by central bank reserves.

- The European Central Bank (ECB) announced a new QE package—the Pandemic Emergency Purchase Programme—amounting to €750 billion, which should bring total QE-related asset purchases to more than €1.1 trillion in 2020. The central bank has also altered issuer limits on the amounts and types of securities it can buy. If needed, the ECB can also use its Outright Monetary Transactions programme to purchase an unlimited amount of short-term government bonds.

- The US Federal Open Market Committee cut the fed-funds rate to near zero through two off-cycle cuts and committed to purchasing unlimited amounts of Treasurys and mortgage-backed securities (MBS). Additionally, the Fed established new, promoted existing and revived retired facilities to support commercial-paper funding, primary dealer credit intermediation, money markets, investment-grade corporate bonds (in primary and secondary markets), asset-backed loans, and central bank foreign-exchange swaps, along with high levels of reverse repo funding.

SEI’s View

Black swans, once largely presumed a myth because only the white variety was ever observed in nature, have become symbols of events that are exceptionally rare in occurrence and severe in impact. Today we are confronted with a black swan in the form of a pandemic, as COVID-19 continues its rapid spread and causes financial markets to plunge across much of the world.

The sudden and widespread stop in economic activity by government fiat is something that has never before been experienced on such a scale. The ultimate impact on GDP is truly anybody’s guess. The first quarter of 2020 could see a decline at an annual rate of between 3% and 5%. The second quarter will likely be one for the record books. Wall Street economists forecasted a quarter-to-quarter annualised decline ranging from 12% to 30% as of late March.

National governments have been quick to respond. All central banks are in crisis-fighting mode, having learned valuable lessons during the 2008-to-2009 great financial crisis, re-establishing unconventional bond-buying programmes and creating some new facilities to expand the types of accepted collateral in order to extend cash to companies that need it.

The Fed and other leading central banks have moved with an alacrity and forcefulness that we find commendable. But central banks cannot single-handedly support this economic shutdown. In our view, fiscal policy—in the form of direct income support, tax deferrals, loan guarantees and outright bailouts of industries badly damaged by the halt of economic activity—must be the prime tool used to conduct the response to this crisis.

The fiscal response is occurring with a speed and decisiveness that has seldom been seen. The U.S. Congress has passed into law a fiscal response that should top 10% of GDP—meaning that the overall deficit this year in the U.S. could approach 15% of GDP. Even before the ink dried on the latest package, there already is talk of the need for another funding package for states and local governments.

Other developed countries are looking to pursue a similar strategy of massive income support and liquidity injections. Germany, a country that typically keeps its wallet closed, is setting the example for Europe. The government has proposed a package equivalent to a whopping 30% of the country’s GDP, counting contingencies. Since Germany has built up large reserves in its existing income-support program, the supplementary budget is expected to push the country’s on-budget deficit only toward 5% of GDP in 2020, following several years of surplus.

Few other countries in Europe have the fiscal strength of Germany. Italy, the European epicentre of the virus, will be particularly hard-pressed to do all that will be needed to stabilise its economy. Italy’s government debt-to-GDP ratio is already well above other major European countries.

The only way a financial crisis can be averted is through the ECB backing up the debt. This is now-or-never time for the EU and eurozone. The stronger countries must come to the aid of the weaker, or face an intensified popular backlash that could threaten the unity of the economic zone. Unfortunately, Germany and the Netherlands are not yet ready to come to the rescue and are standing in the way of the EU issuing ”corona bonds.” We anticipate this opposition will melt in front of the unfolding disaster.

The onslaught of developments presented by the spread of COVID-19 and a simultaneous collapse in oil prices has forced financial markets to recalibrate prices sharply as expectations about different industries and the overall economy shift at a breakneck pace. Investors should gain some reassurance, however, from the fact that a virus-containment-induced earnings recession is generally only expected to last a couple quarters or so. If market prices are based on a long-term, multi-year expectation, then this fallout should represent a relatively small part of the market’s forward-looking focus.

In any event, there is no question that markets have entered deeply oversold territory in technical terms; although it is too soon to say that the market bottom has been established. Nonetheless, we are grateful that the chaotic trading seen in recent weeks has eased considerably thanks to the liquidity provided by central banks and the fiscal package passed by the US Congress.

Only time will tell whether markets have sufficiently discounted the pain that lies immediately ahead. We have to be cognisant of the fact that earnings estimates will be coming down hard—maybe by 40% to 50% on a year-over-year basis—over the next two quarters. These waterfall declines in earnings could drag equities down with them, but likely not to the same extent. It all depends on how willing investors are to look beyond the valley. If there is a belief that the fiscal and monetary measures taken in the past two weeks will successfully prop up the global economy, then markets should prove resilient. We think a great deal of volatility is still ahead of us, but another big decline along the lines of the past month could be avoided. Indeed, if there are signs that the infection rate is beginning to peak in Europe and the US, it might not matter at all where earnings go in the near term. Investors will likely begin to bid stock prices higher in anticipation of an economic recovery, as they almost always do.

During periods of chaos in financial markets, investors often picture professional portfolio managers frantically trading in an effort to avoid the worst of the carnage while seeking opportunities to profit. At SEI, that reality couldn’t be further from the truth.

With a pandemic crippling the global economy and an oil glut exacerbated by suspended activity around the globe, we find ourselves in an environment almost completely void of reliable information—which, to us, makes frantic trading an especially unwise approach to financial stewardship. So, what are we doing?

We stick to our investment philosophy and process, maintaining our view that diversification is a sound approach over full market cycles, which include bull markets (some of which last for more than a decade) and bear markets (which can vary in terms of length and severity).

Right now, as always, we are exploring how to deliver as diversified a portfolio as possible to all of our investors regardless of their risk tolerance. We’re considering the known risks inherent to the capital markets, as well as the uncertainty that comes with any long-term investing plan such as the black swan we’ve encountered in 2020.

We build and maintain long-term-oriented portfolios by being attuned to the evolving correlations, or relationships, between asset classes. We believe our strategies are robust and built to handle environments just like this.

With this in mind, what should you do?

For one thing, we think checking your portfolio’s balance every day is about as helpful as watching the news these days. It won’t do anything to ease your nerves. At a portfolio level, we encourage investors to stay diversified and avoid short-term trading in these volatile markets.

If you are a goals-based investor—and your portfolio is aligned with your goals, time horizon and risk tolerance—be patient. Time should be on your side.

If your portfolio was not aligned with your goals as the selloff began, we think it’s too late to sell now. Doing so may mean you’ll risk missing the rebound that will inevitably happen. No one—including those of us in the financial-services industry—knows exactly when that will take place. But we are confident that the markets will eventually have their comebacks. It may take months—but order will be restored.

Until then, read, watch, listen and learn. You’re seeing a real-life, albeit metaphorical, black swan. Use this experience to become a better, more informed investor. We will continue to monitor economic and financial-market developments and provide our insight to help you achieve that goal.

Glossary of Financial Terms

Bear Market: A bear market refers to a market environment in which prices are generally falling (or are expected to do so) and investor confidence is low.

Bull Market: A bull market refers to a market environment In which prices are generally rising (or are expected to do so) and investor confidence is high.

Federal-funds rate: The federal-funds rate is the interest rate at which a depository institution lends immediately-available funds (balances at the US Federal Reserve) to another depository institution overnight in the US.

Fiscal Policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Repo Funding: Repo (also known as a repurchase agreement) refers to a type of short-term borrowing for dealers in government securities. Central banks can increase the cash available to commercial banks by repurchasing the government securities that they own.

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly-traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.