Quarterly Market Commentary: New Year, Same Positive Trend

Economic Backdrop

UK Prime Minister Theresa May paid dearly for an early Christmas gift: Brexit divorce negotiations made sufficient progress in mid-December, as they were accepted by the European Council, but only after May’s government gave in to many EU demands regarding a financial settlement, citizen rights and the Irish border. This set up phase two of discussions concerning the post-divorce transition period and future relationship between the UK and EU. Talks are expected to start in late January. Elsewhere on the continent in late 2017, the European Commission voted to formally condemn Polish judiciary reforms that critics feared would politicize rule of law; the step could lead to a suspension of Poland’s EU voting rights. European Parliament voted for a similar censure to be applied against Hungary earlier in the year. Acting German Chancellor Angela Merkel prepared to sit down with one-time (and potentially future) coalition partners, the Social Democrats,on the first weekend of the New Year in an attempt to form a government.

A major tax overhaul passed US Congress and was signed into law by President Donald Trump on 22 December, to take effect in 2018. Of lesser note, a stopgap spending bill followed a similar path in late December to keep the US government funded through mid-January. In the traditionally Republican state of Alabama, a Democratic candidate won a contentious “special” (that is, off-cycle) Senate election to fill a vacant seat—narrowing an already-thin Republican majority. Further afield, protests erupted in Iran during the final week of the year, initially to confront poor economic conditions, and evolving to challenge the country’s entrenched leadership.

The Bank of England’s (BOE) Monetary Policy Committee voted unanimously to abstain from making changes in December after increasing the bank rate in November. The European Central Bank (ECB) also held firm in December, in addition to reiterating its October announcement that monthly asset purchases will be reduced and that rate hikes will only take place once these purchases conclude in September 2018 (as anticipated) or possibly later. The US Federal Reserve (Fed) increased its funds rate,as expected, in December and maintained projections for three additional hikes in 2018. Its latest quarterly forecast showed a more optimistic economic outlook over the next few years. The Bank of Japan (BOJ) maintained its quantitative and qualitative easing programme—preserving rate targets and asset-purchase levels—in both monetary policy meetings held during the fourth quarter.

UK stocks rallied sharply in December after a lacklustre October and an even weaker November, while European stocks cooled off at the end of the year following a short-lived climb in late October. US stocks charged into year-end with sustained strength. Japan retrenched in November after impressive gains through October, before making new highs at year-end. Long-term UK gilt rates slid and short-term rates held firm, while eurozone rates increased across all maturities (rates move inversely to prices). The US Treasury yield curve flattened as short-term rates increased and longterm rates declined. Oil prices climbed throughout the last three months of the year; West Texas Intermediate crude oil prices, a key indicator of movements in the oil market, topped $60 per barrel on the last day of 2017 for the first time since July 2015.

UK construction growth slowed as 2017 came to a close; manufacturing growth also came off a bit, but from admittedly strong levels. Labour-market conditions were mostly unchanged in November’s report, with generally low unemployment, although average year-over-year earnings growth increased for the August-to-October period. The last reading of overall third-quarter economic growth was unrevised at 0.4%, yet the year-overyear figure increased to 1.7%.

Eurozone manufacturing conditions remained in high-growth territory, marking the highest new-order levels in more than 17 years. Services sector growth also firmed, albeit at lower-but-still-strong levels. Consumer confidence reflected these buoyant conditions, advancing for the fifth consecutive month in December. The final third-quarter economic growth report remained at 0.6%, but increased to 2.6% in the year-over-year ending September 30, 2017.

While not quite in the eurozone stratosphere, the pace of growth for US manufacturing conditions also continued to accelerate as year-end approached. Joblessness remained low, suggesting another robust employment report for December, while consumer confidence fell only slightly in December from recent 17-year highs. The third reading of overall economic growth edged down to a 3.2% annualised rate.

Our View

We can sum up the year gone by with the exclamation that, at long last, the global financial crisis appears to be in the rear view mirror. In its place is synchronised expansion across most developed and emerging economies. Admittedly, developed economies continued to run at a rather sluggish pace of 2% to 2.5% gross domestic product (GDP) growth. This is, at best, a middling sort of performance in the context of the past five decades. Emerging-market economies, meanwhile, continued to expand at a clip well below that of the past 20 years.

Looking out over the next year or so, we think global growth can still be vibrant enough to allow risk assets to perform well. US tax legislation is hardly perfect: we believe it will not be as stimulative as advertised since tax cuts are skewed toward upper-income tax payers who tend to have a higher saving rate than the median household. But

the permanent corporate tax changes, repatriation holiday, and the full expensing of capital equipment purchases over the next five years are positive developments for economic growth and investment.

Security analysts, always an optimistic lot, are calling for an 11% rise in S&P 500 Index per-share operating earnings in 2018. Although earnings estimates tend to fade through the year as estimates adjust to reality, this time may be an exception because tax cuts have not yet been taken fully into account.

The major worry for investors comes down to the stock market’s valuation. A little more than three-fifths of the S&P 500 Index’s price gain in 2017 came from improving earnings, while the rest was due to a rise in the price-to-earnings (P/E) ratio. But elevated valuations can be justified by the low level of bond yields and the strong trend in profits growth. Of course the higher the valuation, the more vulnerable the stock market becomes to unexpected bad news. We certainly would not rule out a garden-variety correction in stock prices of 5% to 10% somewhere along the line. The market is overdue for one—in 2017, the S&P 500 Index didn’t even register a price correction of 3%.

We won’t be really concerned, though, unless there is a more aggressive swing in Fed policy toward monetary tightness—something we don’t anticipate in the coming year. It’s possible that the US will see inflation pressures finally begin to build in the New Year, but US companies have proven able to maintain profit margins without resorting to price increases.

Through the third quarter, the eurozone economy, as measured by inflationadjusted GDP, advanced by 2.6% on a year-over-year basis. By comparison, the US grew by only 2.3% over this period while the UK’s increase amounted to only 1.5%.

In our opinion, Europe has more growth potential. According to the World Economic Forum’s annual report on global competitiveness, the highincome countries of Western Europe have made important strides in improving labour-market efficiency over the last five years. We also would note that political concerns in the eurozone are far more muted compared with a year ago, although we have not yet seen the end of the heavy antiestablishment undercurrent.

Given our view that the region is a long way from employment levels that will stir inflation pressures, we expect monetary policy to be supportive of growth throughout the coming year even as the ECB proceeds with its taper of quantitative easing. Since these asset purchases will continue at least until the end of September, it appears that policy rates will stay put until 2019.

Thus the way is clear for further growth in economic activity during the year ahead. We should see a continuation of the past year’s strong revival in corporate revenues and earnings, and the MSCI European Economic and Monetary Union Index (Total Return) forward P/E ratio is no higher as of December 31, 2017, than it was at the start that year. Solid economic growth and cheap equity valuations are usually a good combination for investors.

These have not been easy days for UK Prime Minister Theresa May. The divorce stage of Brexit talks has finally concluded, with the UK mostly acceding to the EU’s demands. But Parliament has begun to flex its muscles—and disapproval there would force the parties back to the negotiating table. Keep in mind that any changes to the withdrawal agreement demanded by Parliament would also entail unanimous approval of the 27 EU members on the other side of the negotiating table.

The pace of UK economic growth has been decelerating since 2014, although there is no indication that a recession is around the corner. The BOE’s Monetary Policy Committee forecasted only two rate increases between now and the end of 2019. While time will tell whether the central bank’s view regarding future policy moves are accurate, policymakers in the UK face tremendous challenges over the next few years. We think investors should tread lightly until there are clearer signs that inflation

pressures have peaked and Brexit negotiations actually yield a favourable economic outcome for the country.

Japan is clearly benefiting from the global economic recovery. Exports to China are growing particularly quickly, and are now about equal to the share going to the US. Exports to the US and Europe also have accelerated, but not to the same extent.

Although there have been rumblings that the BOJ would like to take a step away from the extraordinary monetary policies that have been in place since the financial crisis, the central bank may find it difficult to do so. Domestic demand remains too weak and the population has begun contracting, a trend that will likely accelerate.

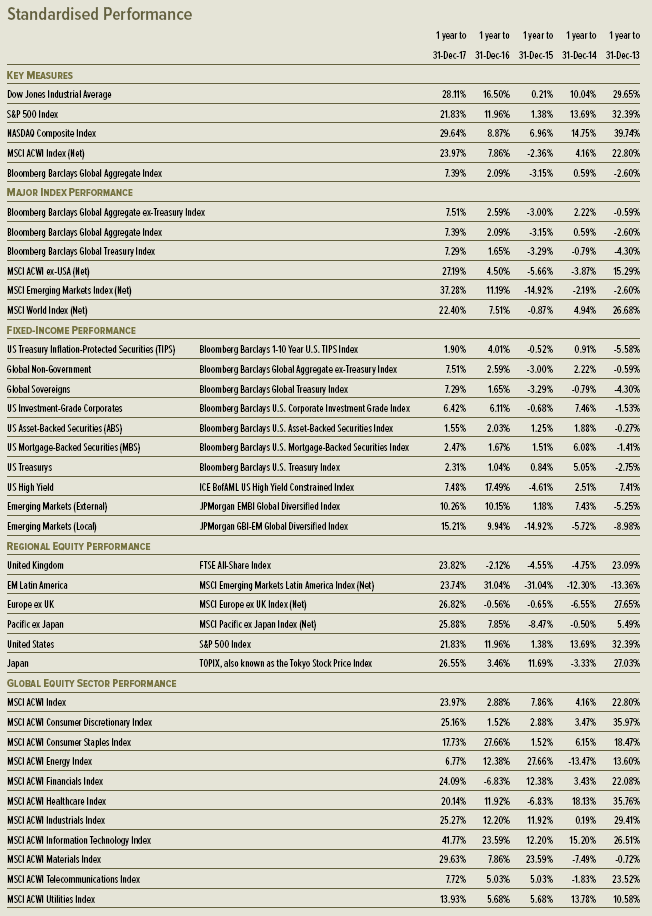

Japanese equities did well in 2017, with the TOPIX rising by 26.55%. Remarkably, the forward P/E ratio declined since the beginning of the year despite the improvement in economic fundamentals. It remains one of the more-cheaply valued stock markets among developed countries. Forwardearnings estimates have climbed sharply in the past year; we note that revenue estimates are also inflecting higher.

The MSCI Emerging Markets Index (Total Return) climbed by 37.28% last year, masking an even stronger contribution by China. Although China continued to reduce its dependence on heavy industry and increased the value added to GDP from service-producing industries, there was some backsliding last year. While these macro statistics need to be taken with a grain of salt, it appears that China’s growth has accelerated significantly from two years ago and advanced at its fastest clip since the 2012 to 2013 period. If China can maintain positive momentum, commodity prices should continue to rally as well.

We have held a positive view of risk assets for most of this long bull market. When speaking to investors who are nervous about the stock market’s valuation, we urge them to keep a longer-term focus. Timing the market in anticipation of a short-term correction should be discouraged. As we’ve seen in the past year, making a major de-risking move could result in a significant opportunity-loss at a time when the stock market’s momentum is quite positive and there are few, if any, signs of major economic imbalances or frothy valuations. Until we see a more significant deterioration in the economic and financial fundamentals that have underpinned the global bull market in risk assets over the past two years, our default investment stance is to stay the course.

There are many possible events and developments that could have a big negative impact, but we believe most have a low probability of actually happening. We will therefore maintain our “risk-on” bias until we see more evidence that such a stance merits revision.

Glossary of Financial Terms

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to do so) and investor confidence is high.

Fundamentals: Fundamentals refers to data that can be used to assess a country or company’s financial health such as amount of debt, level of profitability, cash-flow and inventory size.

Macroeconomic: Macroeconomic refers to the broad economy of a country or region, or the global economy.

Quantitative easing/tightening: Quantitative easing refers to expansionary efforts by central banks to help increase the supply of money in the economy; quantitative tightening refers to efforts by central banks to help decrease the supply of money in the economy.

Yield curve: The yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (likelihood of default). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the yields are closer together.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future performance.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts.These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.