Quarterly Market Commentary: Markets rally on hopes for pivotal moves by central banks"

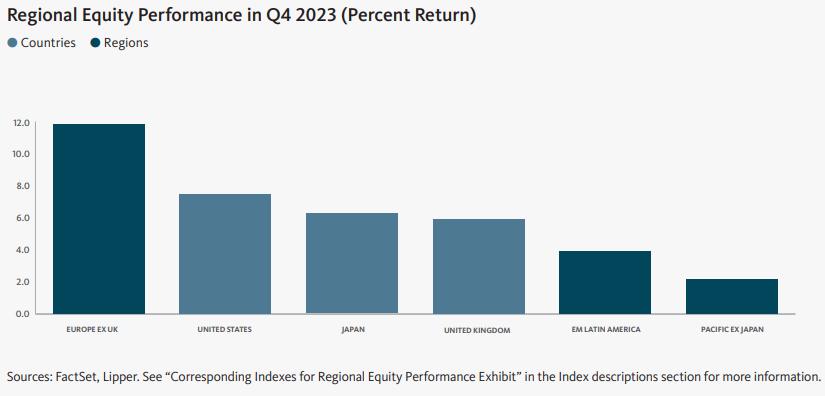

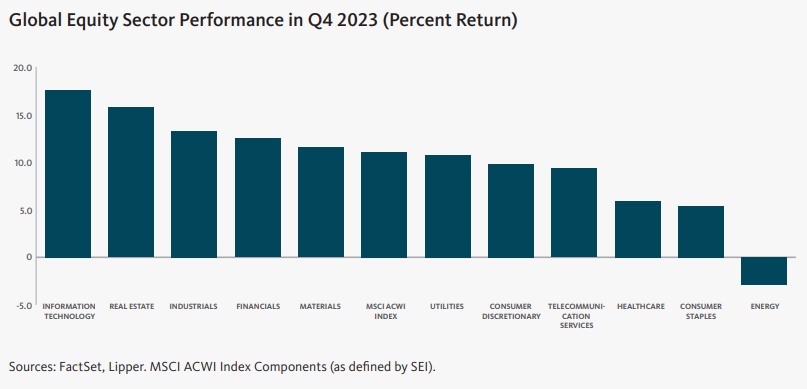

Global equity markets rallied sharply during the fourth quarter of 2023. Signs of slowing inflation spurred investors’ hopes that the Fed and other global central banks could begin to reduce interest rates sooner than previously expected. Additionally, there is optimism that the U.S. economy could be primed for a “soft landing,” in which growth and inflation slow but the economy does not enter a recession. Developed markets outperformed their emerging-market counterparts for the quarter.

North America was the strongest performer among the major developed markets during the fourth quarter, led by the U.S. The Far East region was the primary market laggard due mainly to underperformance in Hong Kong and Singapore. Eastern Europe was the top-performing region within emerging markets during the period attributable primarily to strength in Poland. In contrast, the Gulf Cooperation Council (GCC) countries—Bahrain, Kuwait, Oman, Qatar, Saudi Arabia, and the United Arab Emirates—recorded comparatively smaller gains and comprised the weakest-performing emerging-market region during the quarter.

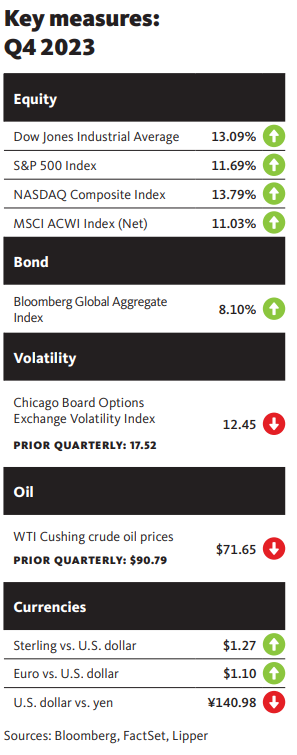

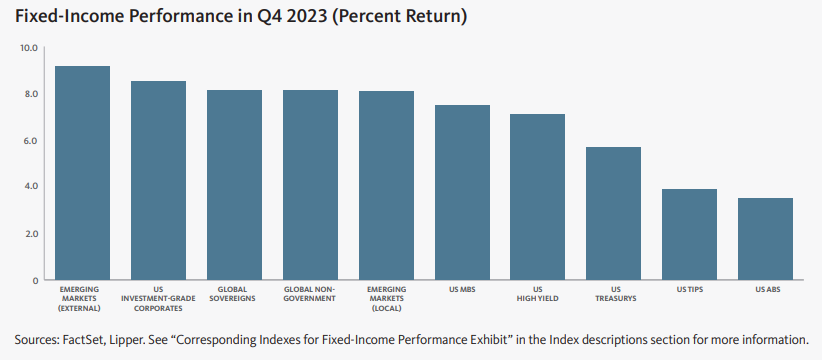

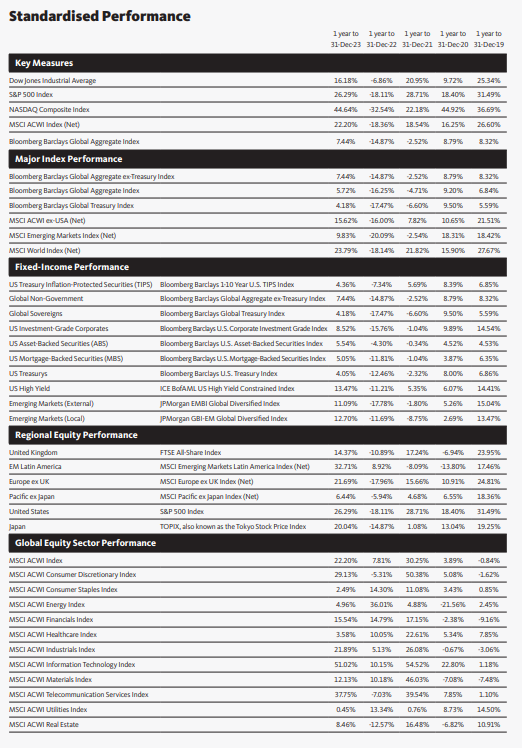

Global fixed-income assets, as represented by the Bloomberg Global Aggregate Bond Index, gained 8.1% in the fourth quarter. Corporate bonds were the top performers within the U.S. market for the month, while U.S. Treasury securities saw relatively smaller gains and were the most notable market laggards.2 Treasury yields moved lower across the curve, particularly for all maturities of one year or longer. Yields on 2-, 3-, 5- and 10-year Treasury notes decreased 0.80%, 0.79%, 0.76% and 0.71%, respectively, over the quarter. The spread between 10- and 2-year notes narrowed from -0.44% to –0.35% during the quarter, and the yield curve remained inverted.3

As widely expected, the Fed maintained the federal-funds rate in a range of 5.25% to 5.50% following its meeting on 12-13 December. In a statement announcing the continuation of the pause in its rate-hiking cycle, the Federal Open Market Committee (FOMC) commented, “In determining the extent of any additional policy firming that may be appropriate to return inflation to 2 percent over time, the Committee will take into account the cumulative tightening of monetary policy, the lags with which monetary policy affects economic activity and inflation, and economic and financial developments.” During a news conference following the FOMC’s meeting, Fed Chair Jerome Powell struck a cautious note regarding the central bank’s efforts to tame inflation, commenting, “No one is declaring victory. That would be premature.” Nonetheless, Powell acknowledged that FOMC members are considering when to begin to cut interest rates as inflation slows. “That begins to come into view, and clearly it’s a topic of discussion,” he noted.

On the geopolitical front, long-simmering tensions in the Middle East escalated to war following a surprise attack on Israel by Hamas in early October. In addition to the casualties resulting from Hamas’ initial incursion into Israel, the militant group and some of its allies abducted more than 200 soldiers and civilians. A one-week ceasefire in the military conflict between Israel and Hamas expired on November 30, after the two sides could not reach an agreement on an extension. The truce had led to several hostage and prisoner exchanges between Israel and Hamas. Each side blamed the other for the failure to extend the ceasefire, and fighting resumed following the expiration of the truce.

Elsewhere, President Joe Biden and China’s President Xi Jinping met in California in mid-November. The leaders of the world’s two largest economies agreed to resume military communications in an effort to improve relations between the countries amid speculation about China’s intention to invade Taiwan, as well as the Xi administration’s support of Russia in its ongoing conflict with Ukraine. At a news conference following the meeting, Biden noted that he and Xi had agreed that if there were concerns about “anything between our nations, or happening in our region, we should pick up the phone and call.” In late December, NBC News reported that Xi had informed Biden during the meeting that China’s government intended to reunify Taiwan with mainland China, though the timing has not yet been determined. Xi also said that China hoped to complete the takeover of Taiwan peacefully—not by force. A spokesperson for the U.S. National Security Council declined to comment on the situation, according to NBC News.4

Global commodity prices, as measured by the Bloomberg Commodity Total Return Index, declined in the fourth quarter. The West Texas Intermediate (WTI) and Brent crude oil prices fell 21.1% and 16.4%, respectively, due to a significant increase in production in the U.S. and weakening global demand. The New York Mercantile Exchange (NYMEX) natural gas price staged a rally in December, but still ended the fourth quarter with a 20.6% loss due to an increase in inventories and forecasts for above-average winter temperatures in the U.S. On the positive side, the gold spot price rose 11.0% for the period, bolstered by a decline in U.S. Treasury yields, as well as higher demand spurred by investors’ hopes that the Fed may begin to ease monetary policy sooner than previously anticipated. The 16.0% increase in wheat prices during the quarter was attributable to a reduction in exports from Ukraine due to the nation’s ongoing conflict with Russia.5

Economic data

U.S.

- The Department of Labor reported that the U.S. consumer-price index (CPI) ticked up 0.1% in November following a flat reading in October. The CPI advanced 3.1% compared to the same period a year earlier—down slightly from the 3.2% annual rise in October. Core inflation, as measured by the CPI for all items less food and energy, posted a 12-month increase of 4.0%, unchanged from the rise in October. Core inflation rose 0.3% in November versus 0.2% during the previous month. Housing costs made the largest contribution to the annual rise in the CPI in November, offsetting lower prices for fuel oil and gasoline. Food prices rose 0.2% and 2.9% during the month and previous year, respectively.

- According to the third estimate of the Department of Commerce, U.S. gross domestic product (GDP) grew at an annualised rate of 4.9% in the third quarter of 2023—down modestly from the second estimate of 5.2%, but sharply higher than the 2.1% year-over-year rise in the second quarter. GDP has increased for five consecutive quarters following declines in the first two quarters of 2022. The largest contributors to economic growth in the third quarter were consumer spending, private inventory investment (a measure of the changes in values of inventories from one time period to the next), and exports. These gains offset an increase in imports, which are a subtraction in the calculation of GDP.

U.K.

- The Office for National Statistics (ONS) reported that consumer prices in the U.K., as measured by the Consumer Prices Index (CPI), fell 0.2% in November, following a flat reading in October. The CPI rose 3.9% year-over-year, down from the 4.6% annual upturn in the previous month. The largest contributors to the 12-month rise in inflation included alcoholic beverages and tobacco, as well as food and non-alcoholic beverages. These more than offset declines in prices for housing, water, electricity, gas and other fuels, as well as transportation. Core inflation, which excludes volatile food prices, rose at an annual rate of 5.1% in November, down from the 5.7% year-over-year increase in November.6

- The ONS also announced that U.K. GDP dipped 0.1% in the third quarter of 2023, following a flat growth rate in the second quarter, and rose 0.6% over the previous year. Production output increased 0.1% during the quarter, compared to the 0.9% upturn during the second quarter. The services sector saw a downturn of 0.2% in the third quarter versus a 0.1% decrease during the second quarter. Output in the construction sector rose 0.4% in the third quarter, compared to a decrease of 0.1% over the previous three-month period.7

Eurozone

- Eurostat pegged the inflation rate for the eurozone at 2.4% for the 12-month period ending in November, down from the 2.9% annual increase in October. Prices for food, alcohol and tobacco rose 6.9% year-over-year in November, but the pace of acceleration slowed from the 7.4% annual rate for the previous month. Costs for services and non-energy industrial goods rose 4.0% and 2.9%, respectively, over the previous 12 months. Conversely, energy prices fell 11.5% year-over-year, following an 11.2% decline in October. Core inflation, which excludes volatile energy and food prices, rose at an annual rate of 3.6% in November, down 0.6 percentage point from the 4.2% year-over-year increase in October.8

- According to Eurostat’s second estimate, eurozone GDP decreased 0.1% in the third quarter of 2023, a modest downturn from 0.1% growth rate in the second quarter, and was flat compared to the same period a year earlier. The economies of Malta and Poland were the strongest performers for the third quarter, expanding 2.4% and 1.5%, respectively. GDP for Iceland fell 3.8% and Ireland’s economy contracted by 1.9% during the period.9

Central banks

- The Fed’s so-called dot plot of economic projections, released in December, indicated a median federal-funds rate of 4.6% at the end of 2024, down from its previous estimate of 5.1% issued in September, signaling that the central bank could cut interest rates by roughly 75 basis points (0.75%) next year. The dot plot also projected that core personal-consumption expenditures (PCE) inflation could slow from its most recent annual increase of 4.0% in November to 2.6% by the end of 2024. The PCE price index is the Fed’s preferred gauge of inflation, as it tracks the change in prices paid by or on behalf of consumers for a more comprehensive set of goods and services than that of the consumer-price index (CPI).

- In a split vote at its meeting on December 13, the Bank of England (BOE) left the Bank Rate unchanged at a 15-year high of 5.25%. Three of the nine BOE Monetary Policy Committee members supported a 25-basis point increase. In its announcement of the rate decision, the BOE commented, “In the most likely, or modal, projection, CPI inflation returned to the 2% target by the end of 2025 and fell below the target thereafter. The Committee continued to judge that the risks to its modal inflation projection were skewed to the upside, such that the mean projection for CPI inflation was 2.2% and 1.9% at the two- and three-year horizons.”

- The European Central Bank (ECB) left its benchmark interest rate unchanged at 4.50% following its meeting on December 14. In a statement announcing the rate decision, the ECB’s Governing Council commented, “Underlying inflation has eased further. But domestic price pressures remain elevated, primarily owing to strong growth in unit labour costs.” The central bank also reiterated its commitment “to ensure that inflation returns to its 2% medium-term target in a timely manner. Based on its current assessment, the Governing Council considers that the key ECB interest rates are at levels that, maintained for a sufficiently long duration, will make a substantial contribution to this goal. The Governing Council’s future decisions will ensure that its policy rates will be set at sufficiently restrictive levels for as long as necessary.”

- The Bank of Japan (BOJ) left its benchmark interest rate unchanged at -0.1% following its meeting in December. The central bank also maintained the upper yield limit of 1.0% for the 10-year Japanese Government Bond (JGB) that it had established in July 2023 as an “upper bound” rather than a stringent cap. In a statement announcing the monetary policy actions, the central bank noted, “Japan’s economy is projected to continue growing at a pace above its potential growth rate. The year-on-year rate of increase in the CPI (all items less fresh food) is likely to be above 2 percent through fiscal 2024, due to factors such as the remaining effects of the pass through to consumer prices of cost increases led by the past rise in import prices. Thereafter, the rate of increase is projected to decelerate owing to dissipation of these factors.”

SEI’s view

Among the seven largest developed economies, the U.S. was the standout performer in 2023. The U.K. and Europe posted minimal gains in overall economic growth in the first three quarters of the year, while Japan managed to register a notable year-to-date gain in GDP despite a contraction during the third quarter. Our more sanguine view on the U.S. contrasted with the consensus of economists, the majority of whom saw a better than 50/50 chance that the U.S. was or would soon be in recession.

We expect more subdued economic growth in the U.S. in 2024, perhaps deteriorating into a stagnant/mildly recessionary environment along the lines currently seen in much of Europe. While interest rates may no longer be rising, they remain high and are starting to bite harder. Households have smaller savings cushions to draw upon to sustain spending in excess of their incomes. Credit-card usage is up sharply and, as a result, delinquency rates are climbing. The situation is not yet critical or indicative of recession, but households will be more heavily reliant on a continued robust jobs market and strong wage growth in the months ahead. The good news is that the jobs market is still tight. However, there are signs of weakness cropping up.

Although we acknowledged this time last year that inflation was trending lower, the rate of increase has decelerated more dramatically in recent months than we had expected. The U.S. led the global acceleration of inflation in 2021 and 2022; in 2023, it has been leading the way down. Both the U.S. and the eurozone have enjoyed a fall in inflation back toward the 2% level, measured on a year-over year basis. The U.K. and France have been lagging in terms of inflation levels, but have, nonetheless, registered a rather sharp slowdown from their inflation-rate peaks.

Does the slowdown in inflation mean that central banks can confidently declare “mission accomplished”? In our opinion, the answer is a firm “no.” This is admittedly a minority view in the aftermath of the Fed’s latest policy meeting in December, but we note that the bulk of the improvement has come in volatile food and energy prices.

Consistent with the Fed’s benign assessment of the economic outlook, the central bank sees three federal-funds rate decreases next year, to 4.6%, four additional cuts in 2025, and more reductions in 2026 to 2.9%. Traders in the futures market appear even more optimistic than the Fed, pricing in 150-basis point (1.50%) of cuts in the federal-funds rate by the end of 2024. In contrast, we lean much closer to the Fed’s view, penciling in three 25-basis point reductions. It all depends, of course, on the strength of the economy and whether inflation stabilises or even backs up a bit from current levels.

Investor sentiment is currently enthusiastic over the prospect of a soft economic landing and a return to 2% inflation. In our view, both bonds and stocks appear to be overbought on a near-term basis, so some kind of price consolidation would not be surprising. The extent of any correction in risk assets will, of course, depend on changing perceptions on economic growth, the corporate-profits outlook, the path of inflation, and central-bank responses.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated.

This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information. Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index. Not all strategies discussed may be available for your investment. Information issued in the UK by SEI Investments (Europe) Ltd, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

This material is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

For professional clients only. Not suitable for retail distribution.