Quarterly Market Commentary: Banking on volatile markets.

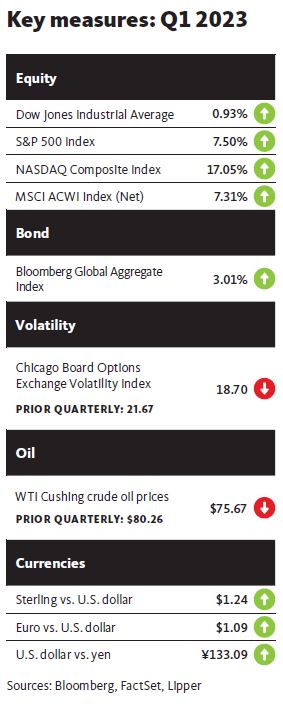

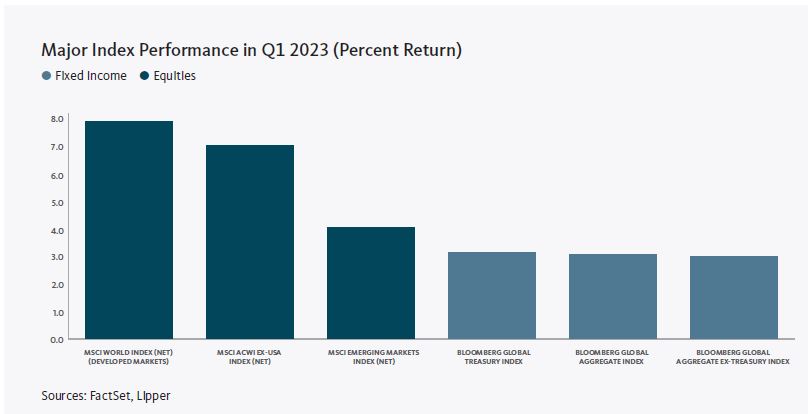

Global equity markets finished in positive territory for the first quarter of 2023, amid numerous periods of volatility in reaction to the latest monetary policy actions and public comments from central banks. Additionally, late in the period, turbulence in the banking sectors in the U.S. and Europe led to a selloff in equity markets globally before stocks rallied towards the end of the quarter.

In early March, California-based Silvergate Capital, a major lender to the highly speculative cryptocurrency industry, announced that it was entering a voluntary liquidation due to significant losses following massive withdrawals of funds by depositors. Soon thereafter, two U.S.-based regional banks–Silicon Valley Bank (SVB) and Signature Bank–failed after depositors withdrew funds on fears regarding the valuation of the institutions’ bond portfolios. The Federal Deposit Insurance Corporation (FDIC), an independent agency that insures deposits, and examines and supervises financial institutions, was appointed as receiver to SVB on March 12 after the California Department of Financial Protection and Innovation closed the bank. Occurring on the heels of the collapse of Silvergate Capital, SVB’s failure prompted investors to reconsider the safety of their positions across the banking industry. Signature Bank, which was shut down by New York state regulators on March 12, also was closely aligned with the cryptocurrency industry. In a separate matter, 11 of the largest U.S. banks deposited $30 billion with First Republic Bank, another troubled lender.

The bank troubles were not limited to the U.S. Swiss lender Credit Suisse also came under pressure after suffering significant investment losses in 2021 and 2022. Credit Suisse reported that clients had withdrawn 110 billion francs (US$119 billion) of funds in the fourth quarter of 2022. The Swiss National Bank, Switzerland’s central bank, announced that it would provide the embattled bank with 50 billion francs (US$54 billion) in financial support. Soon thereafter, Swiss bank UBS took control of rival lender Credit Suisse in an emergency 3 billion franc (US$3.2 billion) deal negotiated by Swiss government regulators. While this development was not directly related to the failures of the U.S. regional banks, the timing resulted in significant declines in the share prices of other banks worldwide.

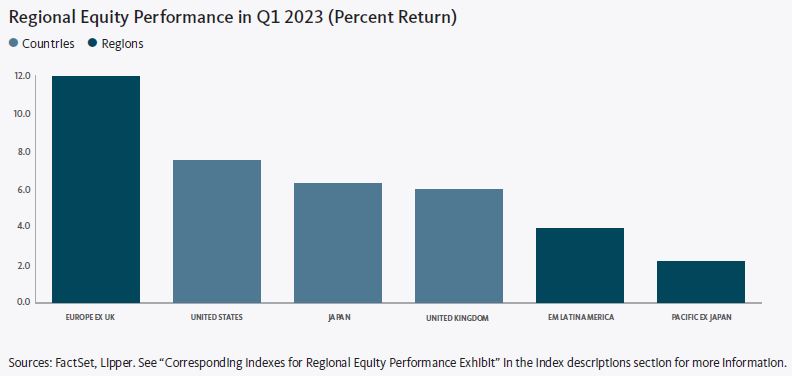

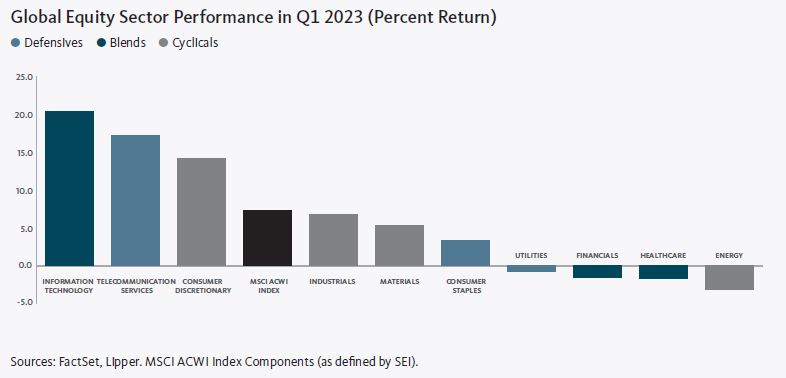

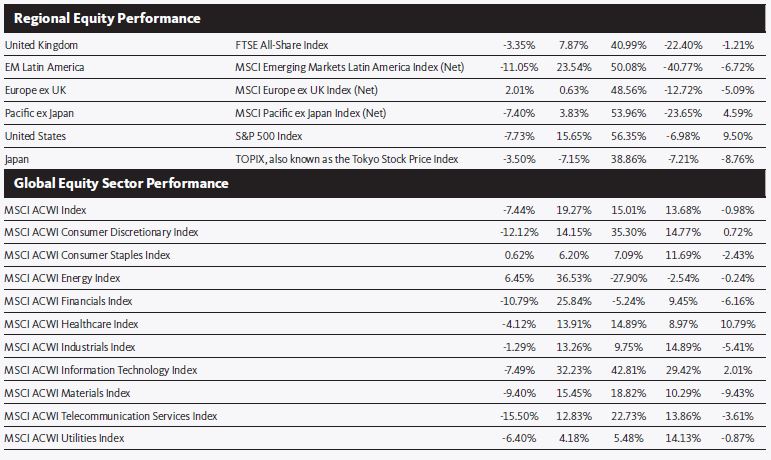

Developed markets garnered positive returns over the quarter and outperformed emerging markets. Europe was the top-performing region among developed markets for the quarter due primarily to strength in Ireland and the Netherlands. North America also performed well. The Far East region generated the largest gains in emerging markets, buoyed by robust performance in Taiwan and Korea.

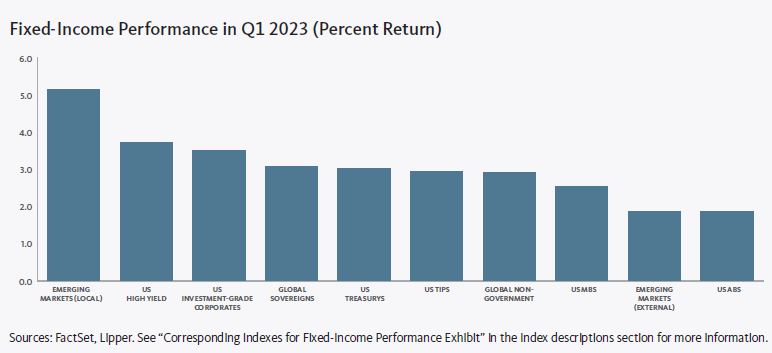

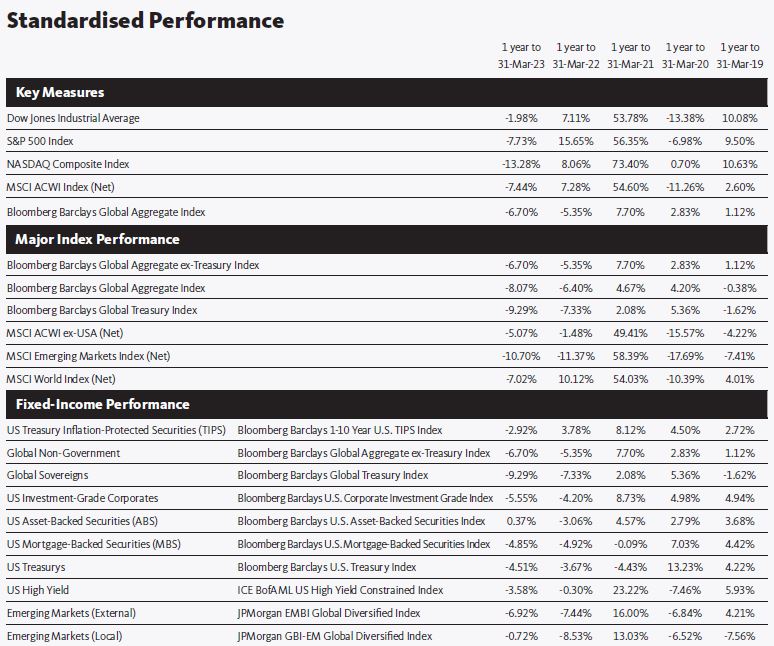

U.S. fixed-income assets ended the quarter in positive territory as Treasury yields declined for all maturities of one year or greater (yields and prices have an inverse relationship). High-yield bonds (below-investment-grade fixed-income securities) were the top performers for the period, followed by corporate bonds and U.S. Treasurys.2 Mortgage-backed securities (MBS) saw relatively more modest gains.3 The yields on two-, three-, five-, and ten-year Treasury notes decreased 0.35%, 0.41%, 0.39%, and 0.40%, respectively, over the quarter. The spread between ten- and two-year notes widened 0.05% to -0.58% during the period, further inverting the yield curve.

Global commodities markets generally lost ground over the quarter. The West Texas Intermediate (WTI) crude-oil spot price decreased 5.9% in U.S. dollar terms, while Brent crude oil fell 7.1% amid concerns that additional interest-rate hikes from central banks may weigh on global economic growth and reduce demand. However, the prices for both commodities rallied sharply over the last two weeks of the quarter amid easing worries about the banking crisis and supply concerns after Turkey stopped pumping oil from a pipeline in Kurdistan following an arbitration decision that the oil could not be shipped without the consent of Iraq’s government. The New York Mercantile Exchange (NYMEX), a commodities trading exchange, natural gas price tumbled nearly 47% during the quarter as an unusually mild winter in the U.S. continued to weigh on demand during the home-heating season. The gold spot price was volatile, but ended the quarter with an 8.1% gain. The gold price rallied sharply in January due to weakness in the U.S. dollar and declining U.S. Treasury yields before falling in February on investors’ worries that the Fed’s rate hikes may lead to a recession in the U.S., which would hamper demand for precious metals. The spot price then rose during the banking crisis in March, as investors generally view gold as a “safe-haven” asset during times of uncertainty. Wheat prices fell 12.6% during the quarter as Egypt made a large purchase tender for Russian wheat at a relatively low price. Additionally, in March, Russia renewed a deal with Ukraine that allows the shipment of Ukrainian grain through the Black Sea.

In the U.S., all eyes (and ears) were on the Federal Reserve (Fed) over the quarter. During a speech in early February, soon after the Federal Open Market Committee (FOMC) had implemented a 25-basis-point (0.25%) increase in the federal-funds rate, Fed Chair Jerome Powell commented that the central bank’s efforts to cool inflation are “likely to take quite a bit of time. It’s not going to be smooth. So we think we’re going to have to do further [rate] increases, and we think we’ll have to hold policy at a restrictive level for some time.” The subsequent banking crisis in March may have tempered the Fed’s aggressive rate-hiking policy. At a news conference following the announcement of a 25-basis-point (0.25%) increase in the federal-funds rate to a range of 4.75%-5.00%, a reporter inquired about the possibility of interest-rate cuts later this year. Powell responded, “That’s not our baseline expectation.” He acknowledged that the FOMC members had considered a pause in the rate-hiking cycle, given the recent turmoil in the banking sector. He also noted that prior to the onset of the banking crisis, the Fed had discussed the possibility of a more hawkish 0.50% rate increase as U.S. economic data remained relatively strong.

On March 15, U.K. Chancellor Jeremy Hunt unveiled the government’s new budget, which directly addresses the nation’s tight employment situation. Among some of the proposals: increasing vocational training; providing tax incentives, enhancing access to capital and easing certain regulations to encourage the creation of new enterprises. Elsewhere, the labour tensions between U.K. public employees and the government appeared to be easing. The administration of Prime Minister Rishi Sunak had been plagued by public-sector employee strikes and other job actions since late 2022, as pay increases have not kept up with the U.K.’s inflation rate, which was up 10.4% year-over-year in February, according to the Office for National Statistics (ONS).5 Several National Health Service (NHS) unions–including the Royal College of Nursing, GMB and Unison–supported the government’s offer of a pay raise of 2% in 2022-2023, followed by a 5% increase in 2023-24, with larger raises for the lowest-paid employees.6 While labour issues in the health care industry appeared to be resolved, a problem arose in another area. Leaders of the National Education Union, the U.K.’s largest teachers’ union, urged their members to reject the government’s offer of a 4.5% wage increase over the next academic year “in the strongest possible way,” commenting that the proposal was an “insulting offer from a government which simply does not value teachers.

Within the eurozone, the proposal of President Emmanuel Macron to raise the minimum retirement age for the country’s public pension program from 62 to 64 led to civil unrest in that country. There were many violent demonstrations and several large labour unions staged widespread job actions in opposition to the plan. The tensions were exacerbated as Macron did not put the measure up for a vote in the National Assembly, France’s lower house, in which his political party does not have a majority. Fears of recession in Germany arose as the nation’s economy contracted by a greater-than-expected annual rate of 0.4% in the fourth quarter of 2022. High inflation weighed on consumer spending and investments in buildings and machinery during the period.

The Russia-Ukraine conflict raged on. In March, President Xi Jinping of China met with Russian President Vladimir Putin in Moscow to discuss China’s proposal to end the conflict with Ukraine. The Biden administration criticised the plan as “the ratification of Russian conquest,” as it proposed a ceasefire that would recognise Russia’s right to occupy territory in Ukraine and provide Putin with time to bolster the nation’s military forces.

Economic data

U.S.

- The U.S. consumer-price index (CPI) rose 0.4% in February, down 0.1% from January, according to the Department of Labor, and was up 6.0% year-over-year. Higher housing and services costs contributed significantly to the rise in inflation in February. The government attributed the year-over-year upturn in the CPI to sharp increases in prices for energy services and food. Core inflation, as measured by the CPI for all items less food and energy, was up 0.5% in February and 5.5% over the previous 12 months.

- The Department of Labor reported that U.S. payrolls expanded by 311,000 in February, down sharply from 517,000 for the previous month. The unemployment rate, which had dipped to a 54-year low in January, rose 0.2% to 3.6%. The leisure and hospitality, retail trade, and government sectors saw the largest employment gains for the month. Average hourly earnings rose 0.2% in February and 4.4% year-over-year. The slowdown in wage growth over the past several months suggests that employers may be having less difficulty finding new workers.

- According to the Census Bureau, U.S. retail sales–a gauge of consumer spending that comprises more than two-thirds of gross domestic product (GDP) dipped 0.2% in February but rose 5.4% year over year. Non-store retailers and general merchandise stores posted the largest gains in February and over the previous 12-month period, respectively. Conversely, the Census Bureau reported that sales for furniture and home furnishings stores saw the most significant downturn for the month, while electronics and appliance stores recorded the greatest year-over-year decline in sales.

- The Department of Commerce reported that U.S. GDP grew at an annual rate of 2.6% in the fourth quarter of 2022, marking a slowdown from the third quarter’s increase of 3.2%. The U.S. economy expanded by 2.1% for the 2022 calendar year. The reading was also modestly lower than the government’s initial fourth-quarter estimate of 2.9%. The revised estimate resulted from downward revisions to exports and consumer spending. This was partially offset by a downward revision to imports (which are subtracted from the calculation of GDP). The upturn in GDP for the quarter was attributable to increases in private inventory investment (a measure of the changes in values of inventories from one time period to the next), consumer spending, nonresidential fixed investment (purchases of both nonresidential structures and equipment and software), federal government spending, and state and local government spending.

U.K.

- According to the Office for National Statistics (ONS), consumer prices in the U.K. rose 1.1% month-over-month in February—a notable reversal of the 0.4% decrease in January. The year-over-year inflation rate increased 10.4% over the previous 12-month period, up from the 10.1% annual rise in the previous month. Housing and household services (mainly from electricity, gas, and other fuels), as well as food and non-alcoholic beverages, were the primary contributors to the year-over-year increase in prices. Core inflation, which excludes volatile food and energy prices, came in at an annual rate of 6.2% in February, up from a 12-month increase of 5.8% in January.

- The ONS also reported that U.K. GDP increased 0.3% in January 2023, following a decline of 0.5% in December 2022, and was flat for the three month period ending in January. The services sector grew 0.5% in January, led by education, transportation and storage, and arts, entertainment and recreation. Conversely, production output fell 0.3% for the month due mainly to downturns in manufacturing of basic pharmaceutical products and pharmaceutical preparations, and machinery and equipment.

- The S&P Global/CIPS Flash UK Manufacturing Output Index declined 1.9 to a two-month low of 49.0 in March due to a decrease in demand. A reading below 50 indicates contraction in the manufacturing sector.

- The S&P Global/CIPS Flash UK Services PMI Business Activity Index was down 0.7 to 52.8 in March, but indicated expansion for the second consecutive month. There was particular strength in the services sector.

Eurozone

- Inflation in the eurozone slowed by 1.6% to 6.9% in the 12-month period ending in March. Natural gas prices decreased 0.9% year-over-year, while food, alcohol and tobacco costs climbed 15.4% for the same period.

- Eurozone manufacturing activity declined in March, with the S&P Global Flash Eurozone Manufacturing Output Index falling 1.2 points to 49.9.

- Services activity in the eurozone reached a 10-month high in March, with the S&P Global Flash Eurozone Services PMI Activity Index increasing 2.9 points to 55.6.

- According to Eurostat’s third estimate issued in March, eurozone GDP was stable in the fourth quarter of 2022. The eurozone economy grew 1.8% year over year in the fourth quarter and expanded 3.5% for the 2022 calendar year.

Central banks

- The Fed raised the federal-funds rate to a range of 4.75%-5.00% in two increments of 0.25% on February 1 and March 22. In a statement announcing the rate increase in March, the Federal Open Market Committee (FOMC) noted that, despite the current financial difficulties, “The banking system is sound and resilient. Recent developments are likely to result in tighter credit conditions for households and businesses and to weigh on economic activity, hiring, and inflation. The extent of these effects is uncertain.” The FOMC also commented that it “anticipates that some additional policy firming may be appropriate in order to attain a stance of monetary policy that is sufficiently restrictive to return inflation to 2 percent over time.” The statement omitted the Fed’s longstanding reference to “ongoing increases in the (federal-funds) target range,” suggesting that the central bank may be nearing the end of its rate-hiking cycle.

- The Bank of England (BOE) increased its benchmark rate by an aggregate of 0.75% to 4.25% over the quarter. The central bank noted its ongoing concerns about inflation, as the government’s consumer-price index rose 10.4% year-over-year in February (the most recent available data). Even in the midst of a banking maelstrom, BOE Governor Andrew Bailey warned that further policy-rate hikes may be needed.

- The European Central Bank (ECB) boosted its benchmark interest rate from 2.0% to 3.0% in two increments of 0.50% in February and March. In its rate-hike announcement in March, the ECB commented that “Inflation is projected to remain too high for too long” that the increase was “in line with [the ECB’s] determination to ensure the timely return of inflation to the 2% medium-term target.”

- The Bank of Japan (BOJ) left its benchmark interest rate unchanged at -0.1% following its meetings in January and March. At a news conference after the announcement of the interest-rate decision in March, outgoing BOJ Governor Haruhiko Kuroda said that the central bank “has been taking various steps to mitigate the side effects of its monetary easing. I can say that the benefits of our monetary easing have far exceeded the demerits.” Kazuo Ueda will succeed Kuroda as BOJ governor in April.

SEI’s view

Economists have been struggling for the past several months to find the right analogy to describe the future trajectory of growth and inflation in the U.S. The optimists favour the term “soft landing,” whereby growth in business activity slows just enough to reduce inflation pressures without causing a recession. Pessimists see a “hard landing” ahead as the global economy stumbles into recession due to overly tight central-bank monetary policies. Still others see “no landing” whatsoever—economic growth actually accelerates, along with inflation. SEI suggests a fourth possibility: a “holding pattern” in which the economy moves in circles with no estimated time of arrival. Economic growth slows, but not enough to push inflation back to the 2% target rate that the Fed and other major central banks have set as their goal.

The tumult in the banking system isn’t over yet; even after this crisis stage passes, smaller banks will face ongoing pressure to raise deposit rates to more competitive levels, while borrowing from the Fed and U.S. government agencies to improve their liquidity. A recession becomes likelier due to the important role that community and regional banks play in the U.S. financial system. According to the Fed, smaller banks (below the 25 largest banking institutions ranked by domestic assets), account for roughly two-thirds of commercial bank loans. They also comprise a very large proportion of credit extended to small businesses.

SEI is assuming that the current banking crisis will be quelled by the government’s “whatever-it-takes” attitude. If that belief proves wrong, the Fed could indeed blink and cut rates as the futures curve applies; however, the surge of funds being injected into the banking system may well make the job of reducing inflation that much more difficult. The FOMC has underestimated the extent and persistence of core PCE inflation for nine consecutive quarters. And, in every quarter since March 2021, the FOMC members have forecast a return to a 2.0% to 2.5% within the next two years. The latest forecast follows the same trajectory, with core PCE inflation falling to 3.6% by December 2023, 2.6% by December 2024, and 2.1% by December 2025. By contrast, PCE core inflation ended 2021 at 4.8% and 2022 at 4.7%.

The current crisis in the banking sector doesn’t seem to be dissuading other central banks from pursuing their inflation-fighting goals. In particular, the ECB surprised the markets by raising its three key policy rates by 0.5% in March, as members of the Governing Council strongly hinted they would prior to onset of the recent market turbulence. The ECB’s rationale was clear—the mandate is to bring inflation back to its 2% target rate, and the central bank will use its monetary toolset (interest rates and security sales from its balance sheet) in an effort to achieve this goal.

The ECB is not ignoring the financial stability and the underlying health of the banking system, however. Rather, ECB President Christine Lagarde insists there is another set of tools that can be used for that purpose, including liquidity support via its various asset purchase and lending programs, such as the Transmission Protection Instrument (TPI). The TPI was introduced in July 2022, and can be used to counter disorderly market conditions that pose a serious threat to the transmission of monetary policy across the euro area. It gives the central bank the ability to buy the public-sector securities of sovereign and regional governments and agencies with remaining maturities between one and 10 years. There is no preordained limit to the purchases that can be made, and the ECB will have wide discretion regarding which securities to purchase from which member countries.

We believe that recent events in the financial markets have raised the odds of recession in the U.S. beginning later this year or in early 2024. As has been the case following previous recessions, wage pressures most likely will ease and inflation should fall as well. However, global financial markets are probably getting ahead of themselves, pricing in near-term cuts in policy rates and a rapid decline in inflation back below 2% within a year. Both cyclical factors (tight labour markets and consumer resiliency especially) and secular factors (a persistently tight labour market, an emphasis on supply chain resiliency over efficiency, higher capital costs, and higher future tax burdens) suggest to us that inflation will remain higher than what central banks and market participants expect. The Fed and other central banks are facing a severe challenge in their attempt to fight inflation while simultaneously ensuring financial stability. If push comes to shove, we expect the central banks to choose financial stability, leaving the inflation fight for another day.

Glossary of Financial Terms

Yield is the income returned on an investment, such as the interest received from holding a security. The yield is usually expressed as an annual percentage rate based on the investment’s cost, current market value, or face value.

A recession is a significant and prolonged downturn in economic activity.

Monetary policy refers to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Treasury Inflation-Protected Securities (TIPS) are U.S. Treasury bonds that are indexed to an inflationary gauge to protect investors from a decline in the purchasing power of their money.

Mortgage-backed securities (MBS) are pools of mortgage loans packaged together and sold to the public. They are usually structured in tranches (a slice or portion of a structured security) that vary by risk and expected return.

Asset-backed securities (ABS) are created from pools of income-generating assets such as credit cards, and auto, mortgage and student loans.

Yield curve represents differences in yields across a range of maturities of bonds of the same issuer or credit rating (are (which is used to assess the risk of default of companies or countries). A steeper yield curve represents a greater difference between the yields. A flatter curve indicates the short- and long-term yields are closer together.

An inverted yield curve occurs when short-term yields exceed long-term yields. While an inverted yield curve historically has predicted economic recessions, it is an indicator—not a forecast.

The federal-funds rate is the interest rate charged to lending institutions on unsecured overnight loans. It is set by the U.S. Federal Reserve’s Federal Open Market Committee. The rate is increased when the Federal Reserve wants to discourage borrowing and slow the economy and decreased when the Federal Reserve wants to spur economic growth.

Inflation is the rate of increase in prices over a given period of time.

Gross domestic product (GDP) is the total monetary or market value of all the goods and services produced in a country during a certain period.

A soft landing refers to a moderate economic slowdown following a period of growth.

A hard landing refers to a notable economic slowdown or downturn following a period of rapid growth, usually resulting from a government’s attempts to slow inflation.

Quantitative tightening refers to efforts by central banks to decrease the supply of money in the economy.

Index Descriptions

The MSCI All Country World Index (ACWI) is a market capitalization-weighted index that tracks the performance of over 2,000 companies, and is representative of the market structure of 48 developed and emerging-market countries in North and South America, Europe, Africa, and the Pacific Rim. The index is calculated with net dividends reinvested in U.S. dollars.

The ICE BofA U.S. High Yield Constrained Index is a market capitalization-weighted index which tracks the performance of U.S. dollar-denominated below-investment-grade (rated BB+ or lower by S&P Global Ratings and Fitch Ratings or Ba1 or lower by Moody’s Investors Service) corporate debt publicly issued in the U.S. domestic market.

The ICE BofA U.S. Corporate Index includes publicly issued, fixed-rate, nonconvertible investment-grade (rated BBB- or higher by S&P Global Ratings and Fitch Ratings or Baa3 or higher by Moody’s Investors Service) dollar-denominated, U.S. Securities and Exchange (SEC)-registered corporate debt having at least one year to maturity.

The ICE BofA U.S. Treasury Index tracks the performance of fixed-rate, nominal debt issued by the U.S. Treasury.

The S&P U.S. Mortgage-Backed Securities Index tracks the performance of U.S. dollar-denominated, fixed-rate and adjustable-rate/hybrid mortgage pass-through securities issued by Ginnie Mae (GNMA), Fannie Mae (FNMA) and Freddie Mac (FHLMC).

The S&P 500 Index is a market-weighted index that tracks the performance of the 500 largest publicly traded U.S. companies and is considered representative of the broad U.S. stock market.

Consumer-price indexes measure changes in the price level of a weighted-average market basket of consumer goods and services purchased by households. A consumer price index is a statistical estimate constructed using the prices of a sample of representative items whose prices are collected periodically.

A purchasing managers’ index (PMI) tracks the prevailing direction of economic trends in the manufacturing and service sectors.

The S&P Global/CIPS Flash UK Manufacturing Output Index measures the activity level of purchasing managers in the manufacturing sector of the U.K. A reading above 50 indicates expansion in the sector; below 50 indicates contraction.

The S&P Global Flash UK Services PMI Business Activity Index measures the activity level of purchasing managers in the services sector. A reading above 50 indicates expansion in the sector; a reading below 50 indicates contraction.

The S&P Global Flash Eurozone Manufacturing Output Index measures the activity level of purchasing managers in the manufacturing sector of the eurozone. A reading above 50 indicates expansion in the sector; below 50 indicates contraction.

The S&P Global Flash Eurozone Services PMI Activity Index measures the activity level of purchasing managers in the services sector of the eurozone. A reading above 50 indicates expansion in the sector; below 50 indicates contraction.

Important Information

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the Strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. There is no assurance as of the date of this material that the securities mentioned remain in or out of the SEI Strategies. Positioning and holdings are subject to change. All information as of 31 March 2023.

Information contained herein that is based on external sources or other sources is believed to be reliable, but is not guaranteed by SEI, and the information may be incomplete or may change without notice. This document may not be reproduced, distributed to another party or used for any other purpose.

There are risks involved with investing, including loss of principal. Diversification may not protect against market risk. There may be other holdings which are not discussed that may have additional specific risks. Narrowly focused investments and smaller companies typically exhibit higher volatility. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors, in addition to those associated with their relatively small size and lesser liquidity. Bonds will decrease in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. SEI products may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

Index returns are for illustrative purposes only, and do not represent actual account performance. Index returns do not reflect any management fees, transaction costs or expenses. Indexes are unmanaged and one cannot invest directly in an index.

Not all strategies discussed may be available for your investment.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The views and opinions within this document are of SEI only and are subject to change. They should not be construed as investment advice.

The views contained herein are not to be taken as advice or a recommendation to buy or sell any investment in any jurisdiction. Our outlook contains forward-looking statements that are judgments based upon our current assumptions, beliefs and expectations. If any of the factors underlying our current assumptions, beliefs or expectations change, our statements as to potential future events or outcomes may be incorrect. We undertake no obligation to update our forward-looking statements.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI UCITS Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI UCITS Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”) to provide general distribution services in relation to the SEI UCITS Funds either directly or through the appointment of other sub-distributors. The SEI UCITS Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI UCITS fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI UCITS Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. Please refer to our latest Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Document, Summary of UCITS Shareholder rights (which includes a summary of the rights that shareholders of our funds have) and the latest Annual or Semi-Annual Reports for more information on our funds, which can be located at Fund Documents.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds.

Singapore

The offer or invitation to subscribe for or purchase shares of the Sub-Funds (the “Shares), which is the subject of this Information Memorandum, is an exempt offer made only: (i) to “institutional investors” pursuant to Section 304 of the Securities and Futures Act, Chapter 289 of Singapore (the “Act”), (ii) to “relevant persons” pursuant to Section 305(1) of the Act, (iii) to persons who meet the requirements of an offer made pursuant to Section 305(2) of the Act, or (iv) pursuant to, and in accordance with the conditions of, other applicable exemption provisions of the Act.

No exempt offer of the Shares for subscription or purchase (or invitation to subscribe for or purchase the Shares) may be made, and no document or other material (including this Information Memorandum) relating to the exempt offer of Shares may be circulated or distributed, whether directly or indirectly, to any person in Singapore except in accordance with the restrictions and conditions under the Act. By subscribing for Shares pursuant to the exempt offer under this Information Memorandum, you are required to comply with restrictions and conditions under the Act in relation to your offer, holding and subsequent transfer of Shares.

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

The SEI UCITS Funds have not been authorised by the SFC in Hong Kong and will be an unregulated collective investment scheme for the purpose of the Securities and Futures Ordinance of Hong Kong (the “SFO”). Shares of the SEI UCITS Funds may not be offered or sold by means of any document in Hong Kong other than (a) to professional investors as defined in the SFO and its subsidiary legislation or (b) in other circumstances which do not result in the document being a “prospectus” as defined in the Companies Ordinance (“CO”) or which do not constitute an offer to the public within the meaning of the CO. This document does not constitute an offer or invitation to the public in Hong Kong to acquire shares in the SEI UCITS Funds. These materials have not been delivered for registration to the Registrar of Companies in Hong Kong.

It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. This information is only directed at persons residing in jurisdictions where the SEI UCITS Funds are authorised for distribution or where no such authorisation is required.

The Shares may not be offered, sold or delivered directly or indirectly in the US or to or for the account or benefit of any US Person except pursuant to an exemption from, or in a transaction not subject to, the registration requirements of the Securities Act of 1933 and any applicable state laws.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

SEI has not considered the suitability or appropriateness of any of the SEI UCITS Funds against your individual needs and risk tolerance. SEI shall not be liable for, and accepts no liability for, the use or misuse of this document by the Distributor. For all Distributors of the SEI UCITS Funds please refer to your sub-distribution agreement with SIEL before forwarding this information to your clients. It is the responsibility of every recipient to understand and observe applicable regulations and requirements in their jurisdiction. The Distributor is, amongst other things, responsible for ensuring that the Shares are only offered, and any literature relating to the SEI UCITS Funds (including this document) are only distributed, in jurisdictions where such offer and/or distribution would be lawful.

Issued in South Africa by SEI Investments (South Africa) (Pty) Ltd. FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

A number of sub-funds of the SEI Global Master Fund plc and the SEI Global Investment Fund plc (the “SEI UCITS Funds”) have been approved for distribution in South Africa under s.65 of the Collective Investment Schemes Control Act 2002 as foreign collective investment schemes in securities. If you are unsure at any time as to whether or not a portfolio of SEI is approved by the Financial Sector Conduct Authority (“FSCA”) for distribution in South Africa, please consult the FSCA’s website (www.fsca.co.za).

Collective Investment Schemes (CIS) are generally medium to long term investments and investors may not get back the amount invested. The value of participatory interests or the investment may go down as well as up. SEI does not provide any guarantee either with respect to the capital or the return of an SEI UCITS Fund. The SEI UCITS Funds are traded at ruling prices and can engage in borrowing and scrip lending. A schedule of fees and charges and maximum commissions is available upon request from SEI. The SEI UCITS Funds invest in foreign securities. Please note that such investments may be accompanied by additional risks such as: potential constraints on liquidity and the repatriation of funds; macroeconomic, political/emerging markets, foreign currency risks, tax and settlement risks; and limits on the availability of market information.

This commentary is intended for information purposes only and the information in it does not constitute financial advice as contemplated in terms of the Financial Advisory and Intermediary Services Act.

Please refer to our latest Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Document and the latest Annual or Semi-Annual Reports for more information on our funds, which can be located at Fund Documents.