Portfolio Manager Perspective: Let’s Talk Factors

We recently caught up with Jason Collins, portfolio manager for SEI’s global equity portfolios, to talk about SEI’s approach to factors and why they matter to investors.

Q. How do you define factors? How do you think about them?

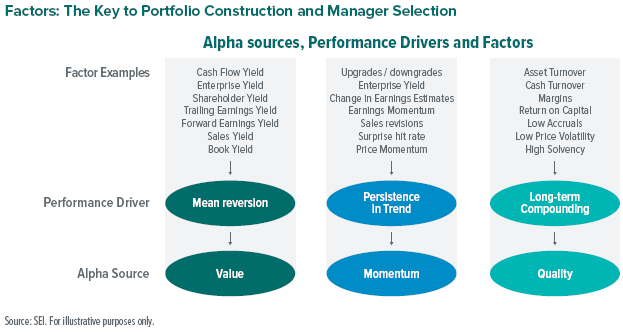

A. A factor is a characteristic that can be measured and used to explain

why the price of a group of stocks might move together in a coordinated manner. While those characteristics could be style factors (like value or growth) that most investors are familiar with, there could be other things as well. Specific sectors, for example, can be factors; technology stocks will share common characteristics and perform differently than energy stocks. Sensitivity to macro variables, such as interest-rate changes or oil prices, could also be factors.

Not every factor is attractive or alpha generating. Some factors may help reduce risk or limit drawdowns, while others are simply random sources of risk that create noise but are not likely to be rewarded in the long run.

If we are talking about whether a company is an energy or communications company, it can only be one of those things. However, every stock sits on a spectrum of factors. For example, all stocks sit somewhere on the spectrum of value—either very cheap, somewhat cheap, fairly priced or expensive—even if not thought of as value stocks. Every stock will similarly have an aspect of growth or an aspect of volatility. These things are not mutually exclusive.

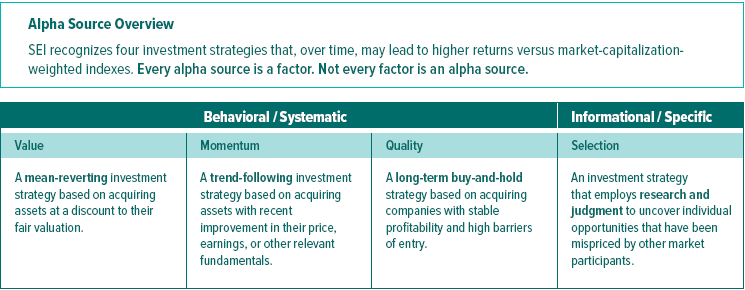

When we think of factors, we most often think about which ones have been historically rewarded and are expected to lead to higher returns over time. When we construct portfolios and research third-party investment managers (managers), we look for exposure to factors that we expect to be rewarded.

Q. How do you use factors when evaluating and selecting managers? What do you look for?

A. When we speak to managers, our first starting point is to philosophically understand how and why they run money the way they do. Portfolio analysis helps us understand factor characteristics, how they vary over time, and the sensitivity and intensity that the portfolio is exposed to among those factors. We attempt to reconcile the manager’s investment philosophy with the analytics that we can see. The objective being to select managers and combine them in a way that intentionally tilts the portfolio toward the desired alpha sources.

Q. How important is the steadiness of the factor for a particular manager? Do you permit multi-strategy discretionary managers that might move a portfolio from value to growth as the market dictates?

A. We want the primary factor we are looking to capture to be stable, although we might expect the secondary factors to be more variable. Each underlying investment manager plays a distinct role in our portfolios, and there should be a certain level of predictability around each manager’s profile from a style and factor perspective. Therefore, we should also have some level of predictability around a manager’s relative performance profile. We tend not to favor managers with a more agnostic style because it would increase the chance that our portfolios would become unbalanced in the future.

If we understand the manager’s profile, we should be able to construct an overall portfolio that is more stable than would be expected by an ever-changing profile. Our managers do not have to be pure single-factor managers. Some may balance, for example, value and quality. We are comfortable with that. But what we want to see is that the primary factor exposure dictated by the manager’s philosophy is stable. If we are allocating to a value manager, we typically want that portfolio to have a consistent value tilt. Secondary factor exposures might move around, and there will be points in time when the cheap stocks in the market may be defensive, low-volatility stocks, which tilt the portfolio away from volatility as a factor. There will be other times when the cheap stocks are high-risk and more cyclical, and to have value exposure, a portfolio might have a positive volatility tilt.

Q. What happens when a manager’s style appears to drift from the intended exposure?

A. We don’t generally want managers to exhibit style drifts from what was intended. While factor analysis is a useful framework, we also have to apply some experience and common sense in interpreting where alpha is coming from. Recent markets have been interesting. We saw, particularly a few months back, that momentum had rotated into cheaper value stocks. There was an unusual situation of seeing notably prominent momentum tilts in some value manager profiles. They didn’t suddenly drift in style or chase momentum; it was that the momentum had rotated into those value names both from earnings and price momentum perspectives. Last year, momentum was almost synonymous with growth because the high-momentum stocks were also the growth stocks. With the rotation into value during the winter and first part of this year, we first saw momentum underperform, but then we saw it come back, mostly as value stocks began to make up a larger portion of momentum portfolios.

One of the other things we have recently seen is some value manager portfolios become more expensive. At first glance, it looks like they style-drifted into expensive stocks; however, these managers had bought into a lot of names, such as airlines and leisure companies, that had been initially hit hard by pandemic lockdowns. These were clearly not expensive stocks, but because their earnings had collapsed, metrics like price/earnings ratios had sharply increased (or even fallen into negative territory). From a pure factor perspective, these stocks looked expensive, and the portfolio styles appeared to have drifted when they had not. So despite an analytical framework, interpretation is still sometimes required.

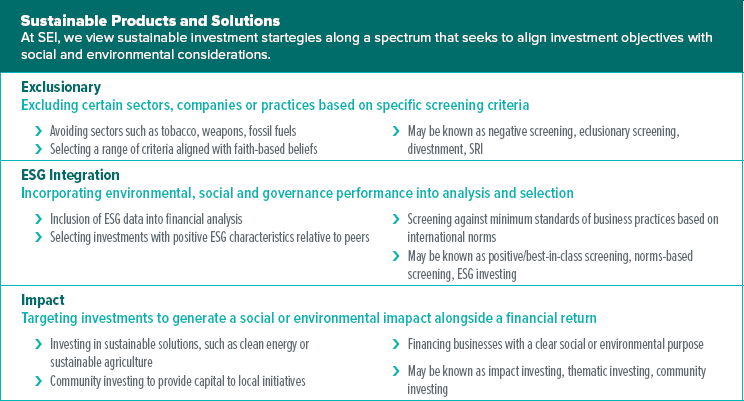

Q. How do you think about ESG? Is it a factor, or is it a separate dialogue?

A. ESG investing can mean different things to different people. We view ESG as a subset of Sustainable Investing. We know that ESG scores can be used to measure company characteristics, and from that, an ESG factor can be created. Those scores and tilts are available through style analytics. To some extent, ESG (and Sustainable Investing as a whole) can be thought of as a factor to be incorporated into an investment process, either as an overlay or alongside other factors. ESG naturally sits more comfortably with some factors than others.

To be simplistic, quality companies tend to score higher from an ESG perspective. If you are a quality-oriented manager, it is easier to work ESG into what you are doing naturally. ESG is likely thought of as a measure of quality in itself. Companies that score poorly are likely to be riskier and more subject to changing regulations. If you are a value manager, then you are attracted to companies that have some sort of controversy. At the moment, a lot of those companies might be in energy and are, therefore, more likely to score poorly in ESG.

So yes, we can think of ESG as a factor, but one that aligns itself with certain investment styles and other factors. For some managers, it is going to be more difficult to naturally incorporate it without compromising what they do or being overly constrained.

Q. How frequently do you look at factor exposures within a portfolio?

A. We examine portfolio analytics at least monthly and often more frequently. Sometimes, the metrics change little, while other times, they can change rapidly in a short period. We also take a factor lens to market-data analytics each month to gauge how attractive certain factors might be relative to each other. We examine valuation dispersions, factor trends, and risk profiles.

We don’t necessarily take corrective action each month, but we do seek to be dynamic through a market cycle to keep a given portfolio in balance. If momentum stocks become value, then so will the portfolio, so adjustments do need to be made to keep balance. Additionally, we sometimes get strong signals, and so tactically, we may choose to shift a portfolio’s factor profile by allocating differently to particular managers. Currently, we think that historically elevated value dispersions are a positive signal for value that might take several years to normalize, which should create a tailwind for value going forward.

Q. How patient are you with a manager that is invested in a factor tilt that should be outperforming in the long term but is not producing in the short term?

A. There is no hard rule. Our starting point is that we want to allocate to factors strategically that we think will outperform over time. Value has struggled over the last 10 years, but we do expect value to pay off over the long run. Taking a forward view, we believe the next 10 years will reward value, simply because of the current level of valuation dispersions. In the context of allocating to a manager, if they are continuing to build portfolios that follow a philosophy and process and are not tempted to stray from that due to short-term underperformance, we will generally stick with them. For example, we would likely terminate a value manager that strayed into growth stocks due to short-term performance pressures. As long as a manager continues to construct a portfolio that we believe will contribute over the long run, we would likely be indefinitely patient.

Glossary

Growth stocks exhibit steady price or earnings growth above that of the broader market.

Macro variables are fiscal or geopolitical events that broadly affect the economy.

Market-capitalization-weighted indexes weight each index component by market capitalization.

Mean reversion assumes that security prices and returns eventually revert to long-term average levels.

Sectors represent areas of the economy in which businesses sell similar products or services.

Volatility measures the dispersion around the average return of a security.

Yield is a return measure for an investment over a set period of time, expressed as a percentage.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone. Diversification may not protect against market risk.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Sustainability guidelines may cause a manager to make or avoid certain investment decisions when it may be disadvantageous to do so. This means that these investments may underperform other similar investments that do not consider sustainability guidelines when making investment decisions. There can be no assurance goals will be met.

If a product or strategy is subject to certain sustainable investment criteria it may avoid purchasing certain securities when it is otherwise economically advantageous to purchase those securities, or may sell certain securities when it is otherwise economically advantageous to hold those securities.

Sustainability is not uniformly defined and scores and ratings may vary across providers.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investments (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.