Portfolio Manager Perspective: Five Questions About Global Equity

We recently caught up with Eugene Barbaneagra, portfolio manager for SEI’s global equity portfolios, to talk about SEI’s approach to value investing and his thoughts on what might happen as the COVID-19 pandemic recedes.

Q: Acknowledging that SEI’s global equity portfolios have been challenged for their adherence to undervalued securities, can we say there are any risk benefits to the funds, either historic or looking ahead?

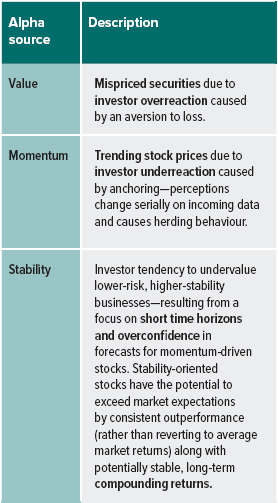

A: Our managers look for undervalued securities. On top of that, we diversify, with value, momentum and stability as our alpha sources. Furthermore, we have dynamically reduced momentum in favour of value due to the currently extreme dislocation between the two. Our global equity portfolios do not necessarily have lower standard deviations than the market, because these are not low-volatility products, and they will typically exhibit market-like volatility. However, our global equity portfolios are more diversified than their benchmarks, with less concentration in fashionable securities or sectors. They also typically have greater earnings per dollar invested than their benchmark. Further, we avoid expensive parts of the market, which historically and economically have implied a high valuation risk. Relative to a capitalisation weighted index, our global equity portfolios generally have stronger fundamentals and are less speculative.

Q: Having a value-style component and tilt has been a relative detractor to performance. What is it about the SEI investment philosophy that meant SEI was naturally unlikely to participate in the recent US tech boom?

A: Our philosophy is based on historical, economic and behavioural analysis. The result of that analysis recognises that there are three broad alpha sources: value, momentum and stability. Strategically, we buy cheap, and we avoid expensive, so we always have value. Will we participate through other alpha sources in the tech bubble? Yes, we do have alpha sources that will participate. Momentum managers will participate and mitigate underperformance. However, these high fliers will not go up forever, and at some point, they will revert and momentum will underperform. At the point of the bubble expanding, we do have an allocation to alpha sources that should benefit from that market dynamic. However, when we combine fundamental-based drivers (value and stability) with sentimental, momentum-based drivers, if value and stability are both lagging, momentum alone is unlikely to change the outcome substantially, only mitigate it. So in the mix, the aggregate portfolio will be underexposed to the frothiest parts of the market when returns are driven by the froth.

Q: How did we arrive at our value philosophy and our value tilt?

A: There is a proven rationale for our approach. Common sense, statistical analysis and hundreds of years of history clearly show that buying cheap is better than buying expensive, and having earnings is better than not having them. This is a strategic argument. Furthermore, there is a strong tactical logic, and I would say an increasingly relevant one, in a world when more and more people trade baskets of stocks in the form of exchange-traded funds and mutual funds. The price is that an investor must be willing to have patience over a full market cycle, including a bull market, bear market and bull market once again. This can be an extended period, sometimes a decade or longer.

While our momentum managers will generally own mega-cap tech stocks on the way up, it will not be at the same weighting as in the market-cap benchmark, creating a headwind when the top of the market is going up and a tailwind when going down. In the long run, we know a better diversified portfolio at the security level, which means less exposure to mega caps, is the preferred way to go.

Q: Value investing can be associated with cheap/junk that could either fail or bounce back big. Is that what the SEI equity portfolio looks like?

A: No. Value investing is not necessarily junk. There are two primary reasons why value works. The risk premium implies that some securities are just risky to hold. Today, for example, it might be risky to own airlines, oil or banks. It seems clear that some airlines and services companies will go bankrupt or be heavily diluted as a result of the current pandemic. But not all. And as compensation for taking this risk, just like an insurance premium, investors can get paid. That is the association with junk. The other part of value is the boring part of value. It’s the securities that are cheap relative to their profitability or intrinsic value. They have low enough price-to-earnings (P/E) ratios, and they are not high fliers. These could be supermarkets or consumer staples. These securities are held by value managers but are not bankruptcy risks. They are also not fancy technology stocks commanding large premiums. They will deliver earnings, and their ability to deliver earnings does not appear excessively risky. We allocate to a mix of managers who allocate to value across a diverse range of definitions for the alpha source.

Q: As COVID recedes, can we expect value to rebound?

A: We believe value will rally if COVID recedes. We could also see a value rally without COVID receding. If COVID continues as it is, most of the potential economic damage is likely already reflected in existing stock prices, and optimism is also already reflected in companies that have benefited from increased stay-at-home habits (online shopping, video meetings, etc.).

There is another possibility. For a bubble to burst, you don’t need any rationale. The tech bubble is just a bubble. Looking at good, profitable companies at the height of the previous tech bubble in 1999-2000, which actually were growing earnings, many of these companies still lost over half their value when the bubble burst, because they were so expensively priced. Expensive quality is better than expensive junk, but it is still expensive. At some point, which is impossible to forecast, the overpriced securities will underperform, and value should benefit.

Important Information

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.