The Party Throws a Congress: China’s Leadership Strengthens Control

The Communist Party of China’s (CPC) twice-per-decade National Congress—a culmination of key personnel decisions and constitutional revisions with great significance to the world’s most populous nation an second-largest economy—concluded this week. Its main event proceeded as expected: Xi Jinping retained his role as the CPC’s General Secretary for a second five-year term and, therefore, will remain President of the People’s Republic of China.

Key political bodies—the core Politburo Standing Committee (PSC), broader Politburo, Central Military Commission (CMC) and Central Commission for Discipline Inspection (CCDI)—were formally appointed by approximately 200 delegates (and about 150 alternates) elected to the Central Committee at the National Congress. As anticipated, these boards

underwent a higher-than-usual cycle of promotions and departures as an outsized number of members reached mandatory retirement age of 68.

Cutting Through the Red Tape

Elections at the National Congress are generally regarded as formalities to confirm decisions that were made in advance through negotiations that unfold from top leadership on down, rather than a genuine series of votes that determine leadership from the bottom up. The outcome can be viewed as a barometer of Xi’s influence and intentions.

Composition of the new PSC, the most powerful political body outside of the General Secretary, indicated that Xi is in no rush to appoint a successor. Given its prominence, the seven-member PSC is typically considered a stepping stone for future party leaders. But every member of the board would be too old at the next National Congress to serve two consecutive terms as General Secretary or President.

There are reasons for hope, however, that an heir apparent could arise at some point over the next five years. Several members of the new 25-member Politburo would be age-eligible to serve two terms as party leader at the next National Congress, although leap-frogging the PSC would break with precedent that extends back to the 1990s.

Additionally, Wang Qishan, head of the CCDI and the party’s preeminent corruption cop, did not retain his seat on the PSC. At 69, Wang had surpassed the mandatory retirement age, and his departure offers a measure of confidence—though certainly no guarantee—that Xi will also abide by the rule at the end of his second term. Perhaps the most explicit demonstration of Xi’s authority resided with an amendment to the party’s constitution that added his philosophy as a guiding principle. Past leaders have seen their contributions adopted into the constitution, but the inclusion of “Xi Jinping Thought on Socialism with Chinese Characteristics for a New Era” is especially notable for two reasons: Xi is one of only three party leaders whose names have been enshrined alongside their concepts, and he is the only one since Mao Zedong whose contribution was styled as “Thoughts.”

Embrace of the Party Lifestyle

China’s transition to a market-based economy commenced nearly forty years ago, at a time when the CPC’s leadership was beginning to acknowledge a need to distance the responsibilities of the party from those of the government. These developments were revolutionary in their own right, and would have amounted to political heresy only a few years earlier. Xi has a more-traditional perspective on party matters:the CPC is the sole substantive force within the Chinese government, and so it must be strengthened. This is the reservoir from which the CCDI draws its power to root out corruption and restore order within the party (which also happens to be a great message for Chinese citizens if the party seeks to hold a sense of legitimacy in their minds). If the CPC exists at the centre of the state in Xi’s model, the state, in turn, resides at the centre of the economy. China’s market integration has come a long way over the last few decades, and Xi appears dedicated to reasserting the role of centralised economic planning. We have witnessed the practical results of this approach during his first term, both at ground level (with expanded state ownership stakes of individual businesses and consolidation of state-owned entities) and more broadly (by using monetary and fiscal policy to deliver and withdraw support in an effort to balance growth and stability).

A Collective Effort Blooms

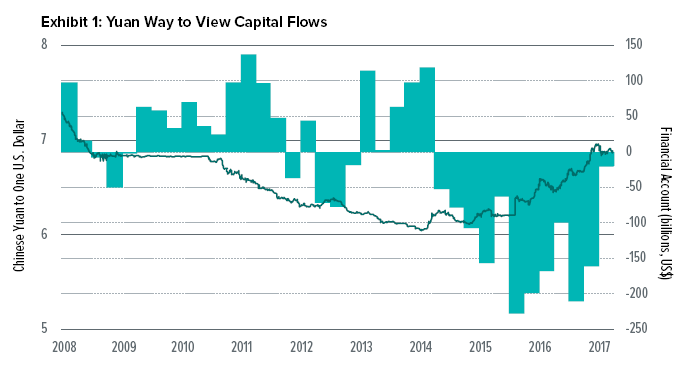

China managed to successfully balance growth and stability over the last five years, although a mid-2015 stock-market selloff and currency realignment jolted investors, driving back-to-back private capital outflows of $600 billion in both 2015 and 2016 (see Exhibit 1). That appears to have abated this year, and real gross domestic product (GDP) growth accelerated in the first half of the year even as the policy landscape grew a bit less accommodative.

A longstanding shift toward a consumption-based economy has continued on Xi’s watch, and was responsible for the largest share of growth through the first two quarters of 2017.

Consumption still trails fixed investment in overall economic activity, so there is plenty of room for improvement, and the burden on investment could benefit from some relief.

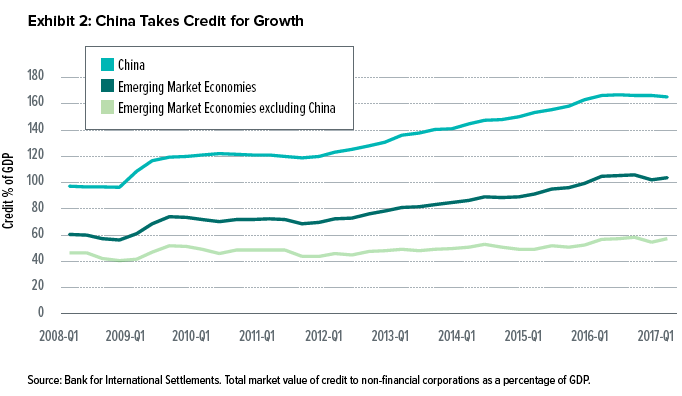

The great outstanding question about China’s economic future is whether it will be able to successfully manage its massive stockpile of debt.

Zhou Xiaochuan, governor of the People’s Bank of China PBOC), has made a point in recent weeks of stating that Chinese companies have too much debt and calling for financial reform. The central banker used a smaller forum at the National Congress to warn against the possibility of a Minsky Moment—the inflection point when a selloff begins after excessive optimism evaporates and questionable fundamental conditions are rapidly priced into asset valuations (named after economist Hyman Minsky).

Xi, for his part, addressed the issue in his opening Work Report to the National Congress, pledging to continue to work on reducing the country’s overall debt load. Exhibit 2 shows credit to China’s non-financial corporations equals more than 160 percent of GDP, roughly triple the level of other emerging-market economies.

High leverage amplifies the complex issues that China faces as it continues to modernise, and increases its risk under tighter economic conditions. But taking a heavy policy hand to this debt burden would constrain growth, so China’s central planners must maintain a delicate balance.

SEI’s View

The CPC’s National Congress is an important milestone on the political calendar that has provided an indication of how Xi will prioritise the next stage of his leadership. We did not expect much in terms of policy details aside from some high-level proclamations with shortlived market-moving consequences, and so were not surprised by the relatively benign reception of developments by investors.

Xi has tightened control of critical sectors of the economy in the past few years and can be expected to maintain this style going forward, so progress of reform should remain gradual and measured. We are inclined to expect the PBOC will intervene a bit more assertively in favour of stability at the expense of growth given the revitalised economic expansion in the

year to date and signs of firmer inflation pressures.

As a regional matter, China’s influence among neighbouring countries has been active and growing over the past decade. China has shifted its approach in the last year—introducing new trade initiatives and exerting economic power for national interest—as the new US presidential administration has unveiled its priorities.

Our Strategies

We don’t believe the National Congress itself presented any catalysts to shift our investment exposure to China. More broadly, China remains the largest country-level allocation within our emerging-market equity fund, and also a perennial underweight given its benchmark dominance.

Our Pacific Basin ex-Japan equity fund features an overweight to mainland China and underweight to Hong Kong that, taken together, are in line with the benchmark. Capital flows from the mainland to Hong Kong have pushed valuations higher there, warranting caution.

Our U.K. Dynamic Asset Allocation (DAA) Fund has a currency position based, in part, on concerns about China’s debt overhang and the likelihood of more modest economic growth than we’ve seen in recent quarters. We have paired a long exposure to the Indian rupee (based on favourable long-term growth prospects, a reform-minded administration and attractive carry) with short exposures to the Korean won, Singapore dollar and Taiwan dollar.

The latter group maintains significant economic ties with China and, unlike India, would likely be negatively affected by any potential disruptions there. A tighter policy approach after the National Congress could heighten pressure on the country’s economy as well as those of its trading partners. In the meantime, this position earns positive carry, given lower short-term rates than those offered on the rupee.

Definitions

Carry trade: A carry trade involves borrowing or selling a financial instrument with a low interest rate, then using it to purchase a financial instrument with a higher interest rate.

Long position: A long position is positioning to gain from future strength of a particular security or currency.

Short position: A short position is positioning to gain from future weakness of a particular security or currency.

Important Information

Past performance is not an indicator of future performance.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Additionally, this investment may not be suitable for everyone.If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular,

nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.