The Odd Couple: Recessions and Value

As an investor in SEI’s portfolios you’re well aware that we believe value is an alpha source. Simply put we seek to buy companies that have attractive valuations because we believe there is significant long-term potential that they will outperform a broad market benchmark such as the S&P 500 Index. In practice, this means our portfolios will have a strategic (long-term) bias toward value (and other alpha sources like momentum and stability) when compared to the portfolio’s benchmark.

You’re probably also aware that a value bias has been quite painful over the past decade. It’s easy to find articles written by the financial press that declare value investing is dead. This isn’t the first time, nor will it be the last, that someone makes such a declaration—despite abundant academic research and historical data showing value investing has generated excess returns. Of course investors continually ask, “When will value outperform again? What will be the catalyst for this?” While, we certainly wouldn’t call a recessionary environment a perfect catalyst for value—and we believe trying to identify catalysts can be a counter-productive exercise anyway—our research does indicate that recessions have historically resulted in favourable environments for value investing.

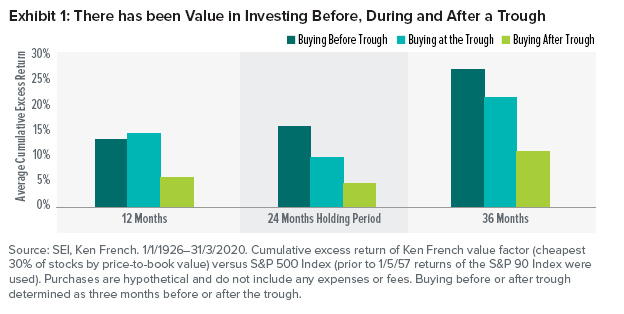

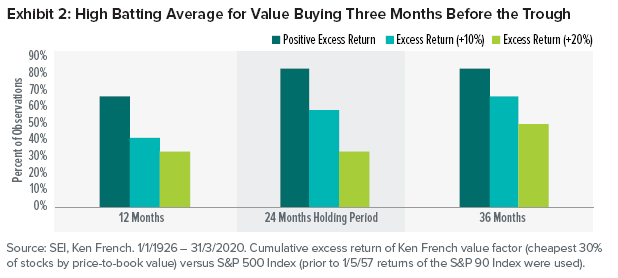

Just like trying to predict catalysts, attempting to time market events is a generally fruitless exercise. In Exhibit 1, we compare the average historical outcomes of hypothetical value investments made at the time of a recessionary trough as well as three months before and after the trough. Our research, based on data from noted academic and author Ken French, indicates that no matter the timing of a value investment, it has typically generated significant outperformance (Exhibit 1) following a recessionary trough. As illustrated in Exhibit 2 for hypothetical value investments made three months before a trough, the results have been fairly persistent. One could argue that the optimal timing for a value investment would actually precedes the recessionary trough. Therefore, we contend that a strategic allocation to value—which, by its very nature precedes a recessionary trough—is an appropriate way to position in this type of environment. Equity markets are widely considered leading indicators and generally begin to recover before the economy improves, meaning investing early may be beneficial.

We don’t know when the COVID-19 economic recession will bottom out. Annualised U.S. gross domestic product (GDP) for the first quarter of 2020 declined 4.8% according to an advance estimate from the U.S. Bureau of Economic Analysis. We expect second-quarter GDP reports to be significantly worse. This sets up the possibility that the latest recessionary trough has yet to come, perhaps arriving in the second quarter or later this year; of course we won’t actually know until after the fact. What we do know is that the data show that value has historically performed quite well at the beginning of an economic recovery, and has continued to outperform while the economy comes out of a recession into an expansion.

Index Definitions

S&P 500 Index: The S&P 500 Index is an unmanaged, market-weighted index that consists of 500 of the largest publicly-traded U.S. companies and is

considered representative of the broad U.S. stock market.

S&P 90 Index: The S&P 90 Index was a precursor to the S&P 500 Index. It was comprised of 50 industrial stocks, 20 railroad stocks and 20 utility stocks.

Glossary of Terms

Alpha source: Our strategies are designed to capitalise on long-term drivers of market performance through exposure to persistent sources of returns such as mean reversion, trend-following and stability.

Batting Average: Batting average is a statistical measure that illustrates how often in percentage terms an investment outperformed a specified benchmark.

Important Information

The opinions and views in this commentary are of SEI only and are subject to change. They should not be construed as investment advice.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

The SEI Global Assets Fund Plc, SEI Global Investments Fund Plc, and SEI Global Master Fund Plc (the “SEI Funds”) are structured as open-ended collective investment schemes and are authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The SEI Funds are managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, (together “SEI”) to provide general distribution services in relation to the SEI Funds either directly or through the appointment of other sub-distributors. The SEI Funds may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above. SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.