Is now the time to step back into bonds?

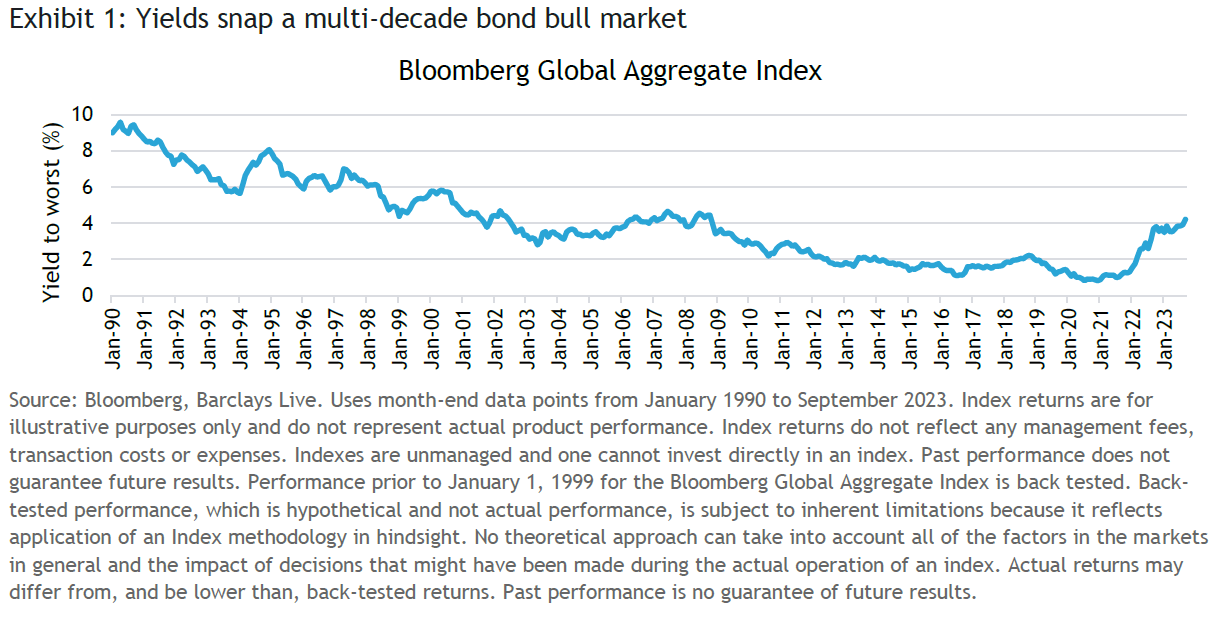

2022 was a terrible year for fixed income investors, with the bond market delivering its worst performance in living memory. The Bloomberg Global Aggregate Index lost 16.3% (-11.2% in USD hedged terms). At a regional level, the U.S. Aggregate Index was down 13.0%, while its Euro Aggregate counterpart registered a 17.2% loss. The Sterling Aggregate Index, meanwhile, fell an eye-watering 23.2%.

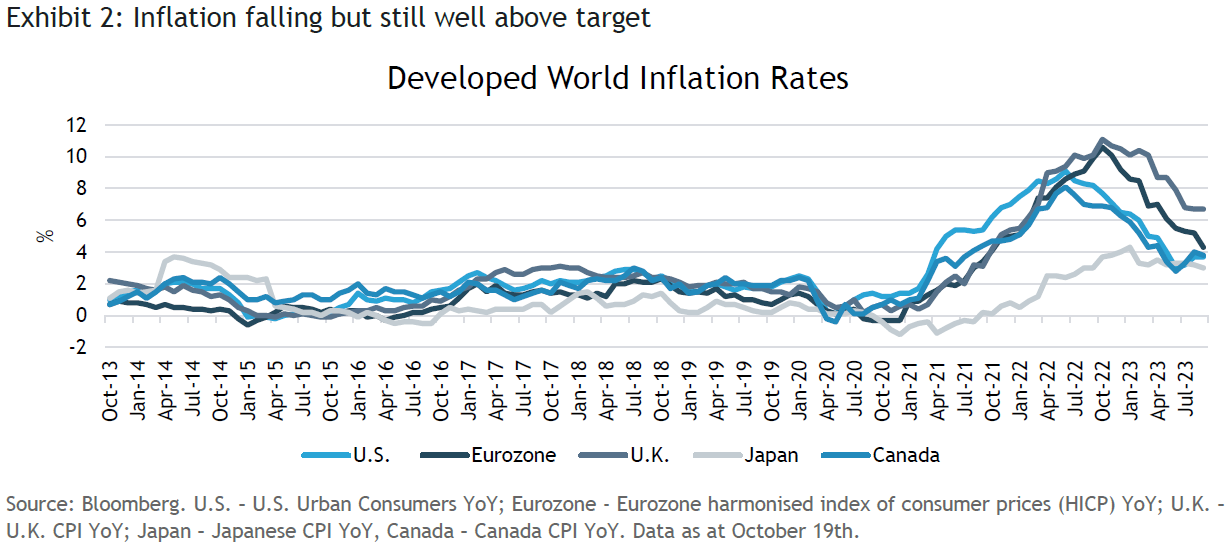

Factor in multi-decade highs in inflation, and bond investors suffered even more in real terms. Despite inflation falling in 2023, the year-to-date performance in fixed income has so far been underwhelming as yields have continued to rise, with the Bloomberg Global Aggregate Index down 3.8% (-0.2% in USD hedged terms).1

With the benefit of hindsight, it is easy to see how the bond market at the start of 2022 was vulnerable to a sharp correction. A combination of low starting yields and lengthened index duration meant that the yield ‘cushion’ for total returns was very low (yields did not have to rise by much for bonds to deliver negative performance). Moreover, the anchoring biases of central banks perhaps conditioned by the ‘lowflation’ of the 2010s meant that the Fed and others were slow to react to rising price pressures, creating a perfect storm for duration-sensitive assets heading into 2022. Still, the magnitude of losses in bond portfolios - in what’s meant to be a more defensive and lower volatility asset class - caught plenty off-guard. Furthermore, bonds had failed in their traditional role as a diversifier to equities. In central banks’ defence, Russia’s invasion of Ukraine and its impact on oil prices, exacerbated the global inflationary shock initially triggered by the fallout from COVID-19. Recent events in the Middle East could further complicate efforts to bring down inflation.

We think that a return to 2% inflation2 might be difficult to achieve anytime soon given that the disinflationary tailwinds that were in play in recent decades have likely run their course. Globalisation is being challenged by ongoing geopolitical tensions at a time when protectionism seems to be back in vogue, the inflationary consequences of which may mean interest rates having to stay higher for longer. Added to this are concerns about fiscal largesse and the amount of bond issuance that the market needs to digest over the coming years at a time when price-insensitive buyers (central banks) are stepping away.

None of this sounds like good news for bond investors. However, we believe that now is the time to adopt a more constructive outlook on owning duration (being long bonds). While the severe repricing of interest-rate risk over the last two years has been painful for bond investors, it does have positive implications for the asset class looking forward.

Conventional bonds exhibit an inverse relationship between price and yield; however, the relationship is non-linear. Positive convexity is a bond investor’s friend because it means that as yields rise, duration falls, and vice-versa. That is, bond prices become less (more) interest rate-sensitive at higher (lower) yield levels.

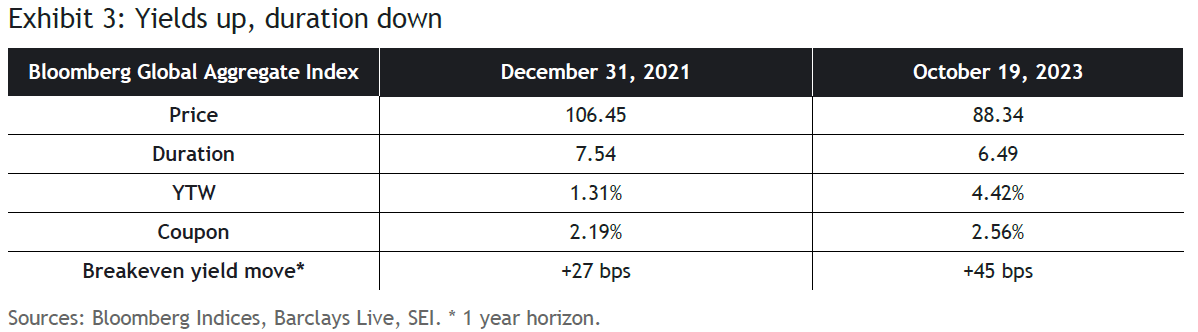

Indeed, as yields have risen in recent years, so too has the duration on bond indices fallen. For example, at the end of 2021, the Bloomberg Global Aggregate Index (“BGAI”) had a yield-to-worst (YTW) of 1.31% and a duration of 7.54. Today, the yield-to-worst on the index is 4.42%, while the duration stands at 6.49.3

Higher yields (and coupon rates) and lower duration result in more favorable breakeven levels 4 (how much yields can rise before returns turn negative).5 Bonds today, therefore, provide a greater margin of safety against rising yields (and further inflation surprises) than they did a few years ago.

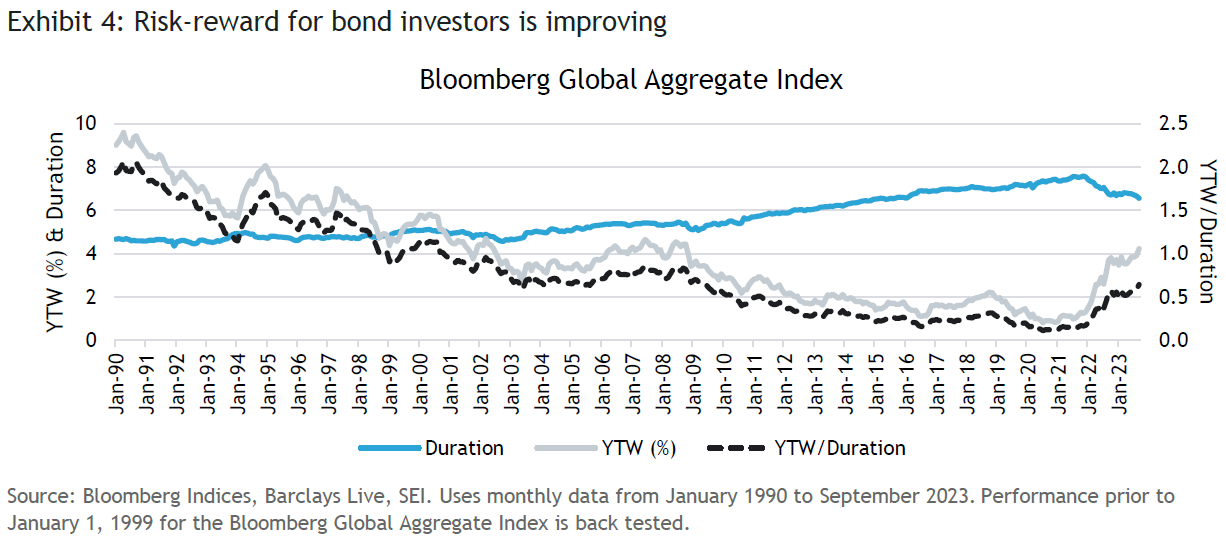

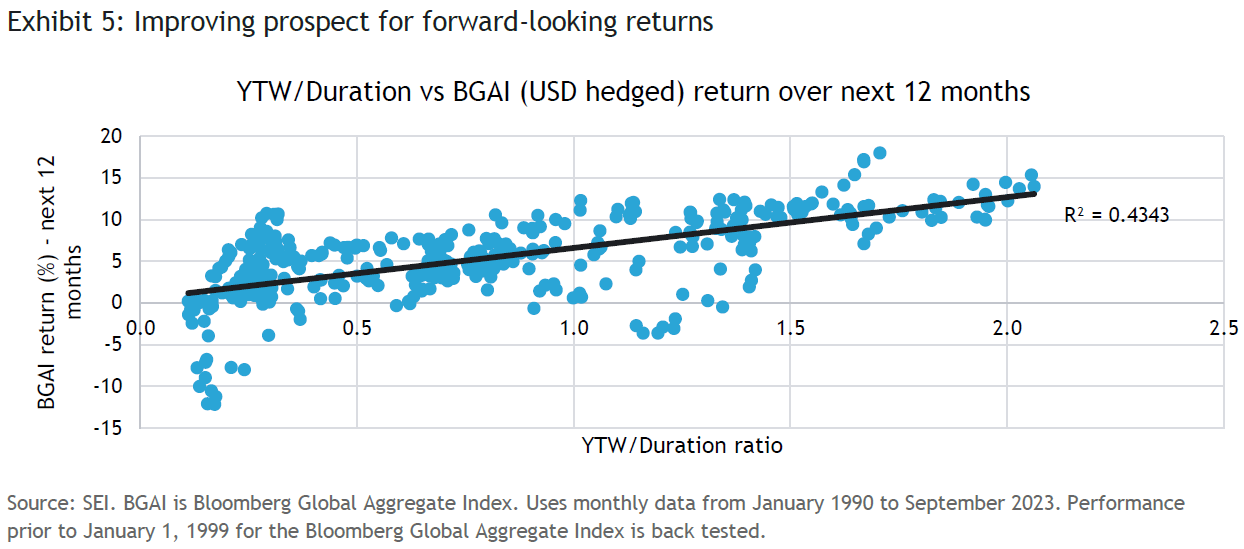

Another way of gauging the value or risk-reward offered by the bond market is to look at the yield-to-worst/duration ratio. This can be thought of as the compensation per unit of interest-rate risk. The graph below shows that this ratio (black line) on the BGAI is at its highest level since 2009.

Below shows the BGAI’s YTW/duration ratio plotted against the index’s forward-looking twelve-month return (in USD hedged terms). Encouragingly (and unsurprisingly), higher starting ratios tend to improve forward-looking returns.6

Bond investors suffered a brutal 2022, which was not helped by the low starting level of yields and extended duration on indices. Today, however, the case for owning duration is stronger as the metrics are stacked more in investors’ favor. Yields now offer a larger buffer against further rises in rates, which could occur if inflation remains elevated for longer. And this is before considering the bull case for bonds, which could easily materialize if the economy enters recession and/or equities and other risk assets experience a significant sell-off. Although the U.S. economy has so far remained remarkably resilient, it is difficult to see how 500+ basis points of Fed rate hikes doesn’t start to impact it in 2024. The case for owning high-grade bonds is stronger today than it’s been for many years.

Important information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person's nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

This document has not been registered by the Registrar of Companies in Hong Kong. In addition, this document may not be issued or possessed for the purposes of issue, whether in Hong Kong or elsewhere, and the Shares may not be disposed of to any person unless such person is outside Hong Kong, such person is a “professional investor” as defined in the Ordinance and any rules made under the Ordinance or as otherwise may be permitted by the Ordinance.

The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America and the Middle East FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.

SIEL is not licensed under Israel’s Regulation of Investment Advising, Investment Marketing and Portfolio Management Law, 5755-1995 (the “Advice Law”) and does not carry insurance pursuant to the Advice Law. No action has been or will be taken in Israel that would permit a public offering or distribution of the SEI Funds mentioned in this email to the public in Israel. This document and any of the SEI Funds mentioned herein have not been approved by the Israeli Securities Authority (the “ISA”).