No, This Time is not Different (We Still Prefer to Buy Low/Sell High)

In rising markets, investors can become hyper-focused on past performance—even more so during bubbles and other anomalies. With headlines declaring ‘Goldilocks’ tech stocks as the new defensives1, market concentrations reaching the 99th percentile on a historical basis2, and pronouncements of the death of value investing, we re-examine the basic principles of ‘buying low’ as well as the inherent risks of ‘buying high’.

Risks of Ignoring the ‘Margin of Safety’

The founders of value investing, Benjamin Graham and David Dodd, noted that ‘the margin of safety is always dependent on the price paid’3. In other words, paying a low price generally increases an individual’s odds of making a profitable investment.

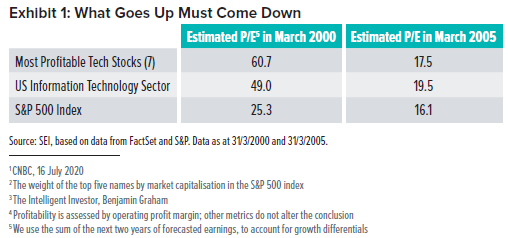

The risk of ignoring this basic principle was vividly illustrated during the tech bubble of 1999-2000. To make the comparison more relevant to today’s market, we examined the seven most profitable4 companies of the time within the US Large Cap Technology sector (the ‘FANGs of 2000’), namely Microsoft, Cisco, Intel, Oracle, EMC, Applied Materials and Texas Instruments. We deliberately avoided frothier ‘dot-com’ segments; the stocks we chose were recognised leaders in their field, with strong earnings and sales growth, high barriers of entry, and innovative edges.

Of course, greatness alone is not a sufficient characteristic for a successful investing strategy. With valuations 2-3x of the broad equity market, a lot had to go right for those firms—and a lot had to go wrong for others—to justify such premium pricing. Indeed, a lot did go right. 20 years later, these companies are still around and, arguably, are still thriving.

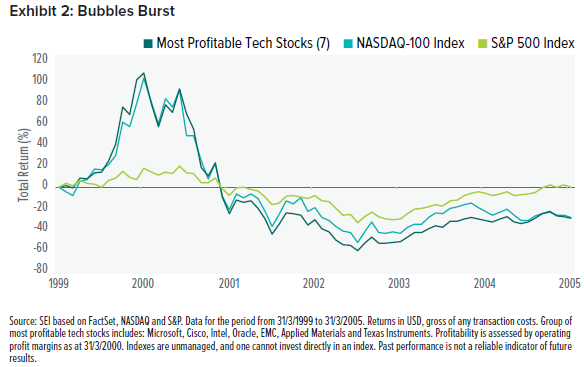

As shown in Exhibit 2, the same could not be said for the fortunes of investors in these companies. During the five years that followed the bursting of the tech bubble, valuations of these stocks came down to a reasonable premium and inflicted severe losses on investors who bought at or near the top of the market. Even when a lot went ‘right’, chasing performance by overpaying led to poor outcomes for the investors.

History Rhymes

As the old saying goes, history doesn’t repeat itself, but it rhymes. What parallels can we draw from the tech bubble experience? Plenty. For starters, today we are witnessing almost verbatim media headlines. ‘Dot com’ has been replaced with ‘cloud computing’, while ‘growth’ has been augmented with ‘quality’; ‘value’ now appears to be relegated to ‘junk’. These are all plausible, in fact, reasonable arguments. Except for one little problem: What might happen when prices for greatness revert to a more typical premium?

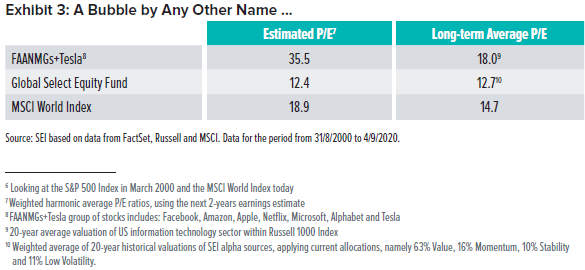

Looking at the valuations in Exhibit 3 below, we can see both good and bad news. We include the SGIF Global Select Equity Fund—a portfolio currently criticised for its adherence to undervalued securities. First, we note that at 19x the next two years’ earnings, the equity market now is not as expensive as it was in March 20006. Likewise, the ‘greats’ of today are expensive but not as bad as their peers 20 years ago. Unfortunately, ‘my bubble is smaller than yours’ is not a valid argument for overpaying. A bubble is still a bubble.

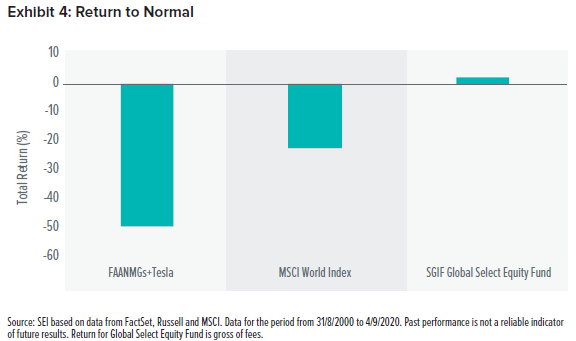

The Cost of Greatness

Let’s examine what might happen when we return to normal. By ‘normal’, we don’t mean that the COVID-19 crisis will dissipate. We mean that optimistic earnings forecasts will be realised, regulatory scrutiny will remain scarce, and innovation in the rest of the economy will disappear. We’ll assume that the Yahoo of today will not face competition from the Google of tomorrow. And we’ll deliberately disregard inevitable competitive threats, a foolish conjecture as investors in Nokia, Intel and IBM would likely attest. Making all of these unreasonably rosy assumptions, we then analyse what might happen if multiples for the same good earnings revert to more reasonable premiums.

The picture implies that, either earnings growth over the following few years will significantly surprise on the upside (over already generally optimistic projections from the analyst community), or returns are going to be disappointing, not just for FAANMGs but the broader MSCI World Index as well. Relying on the US Federal Reserve to further reduce the price of money and elevate valuations is also less plausible in a zero-interest-rate environment.

A More Prudent Approach

There is no silver bullet for long-term investment success. The unwinding of today’s bubble is unlikely to follow the precise pattern of the 2000s. We recognise relentless competitive forces at play, not only at the single-stock level but also at the alpha source and style level. In a world of ever-evolving ‘unknown unknowns’, diversification is the only prudent solution, as cliché as it sounds. To avoid the damage that Yahoo, Nokia and IBM saw in the 2000s is to ensure sufficiently broad allocations to other stocks, industries and asset classes. Whenever the fashion of the day favours a few, we remain sceptical and look elsewhere.

Our active strategies are based on processes that don’t rely on heroic assumptions. Our earnings advantage, or, to quote Benjamin Graham, ‘margin of safety’, is likely to cushion some of the blow when the normal becomes normal again. And no, we don’t believe that this time is different.

Important Information

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever. Investment in the funds or products that are described herein are available only to intended recipients and this communication must not be relied upon or acted upon by anyone who is not an intended recipient.

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

The SGIF Global Select Equity fund is structured as an open-ended collective investment scheme and is authorised in Ireland by the Central Bank as a UCITS pursuant to the UCITS Regulations. The fund is managed by SEI Investments, Global Ltd (“SIGL”). SIGL has appointed SEI Investments (Europe) Ltd (“SIEL”), an affiliate of SIGL, to provide general distribution services in relation to the fund. The SGIF Global Select Equity Fund may not be marketed to the general public except in jurisdictions where the funds have been registered by the relevant regulator. The matrix of the SEI fund registrations can be found here seic.com/GlobalFundRegistrations.Any reference in this document to any SEI Funds should not be construed as a recommendation to buy or sell these securities or to engage in any related investment management services. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application must be made solely on the basis of the information contained in the Prospectus (which includes a schedule of fees and charges and maximum commission available). Commissions and incentives may be paid and if so, would be included in the overall costs.) A copy of the Prospectus can be obtained by contacting your Financial Advisor, SEI Relationship Manager or by using the contact details shown below.

Data refers to past performance. Past performance is not a reliable indicator of future results. Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Returns may increase or decrease as a result of currency fluctuations. Investors may get back less than the original amount invested. SEI Funds may use derivative instruments which may be used for hedging purposes and/or investment purposes. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events.

In addition to the usual risks associated with investing, the following risks may apply: Bonds and bond funds are subject to interest-rate risk and will decline in value as interest rates rise. High-yield bonds involve greater risks of default or downgrade and are more volatile than investment-grade securities, due to the speculative nature of their investments. International investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Emerging markets involve heightened risks related to the same factors as well as increased volatility and lower trading volume. Narrowly focused investments, securities focusing on a single country, and investments in smaller companies typically exhibit higher volatility.

The opinions and views in this commentary are of SIEL only and are subject to change. They should not be construed as investment advice.

This information is issued by SEI Investments (Europe) Limited (SIEL) 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR, United Kingdom. SIEL is authorised and regulated by the Financial Conduct Authority (FRN 191713).

SEI sources data directly from FactSet, Lipper, and BlackRock unless otherwise stated.