Moving Past COVID-19: A Road Map for Investors

The world is finally beginning to move beyond COVID-19 thanks to the steady rollout of effective vaccines. While the pathway back to normal is not expected to unfold in a smooth, straight line, especially given recent outbreaks in various regions and uneven distribution of available vaccines, the overall direction seems clear. In our view, the world is entering what will likely be one of its strongest economic recoveries since World War II—and that could foster economic dynamics and market conditions that look quite different from those of recent decades.

Preparing for future possibilities

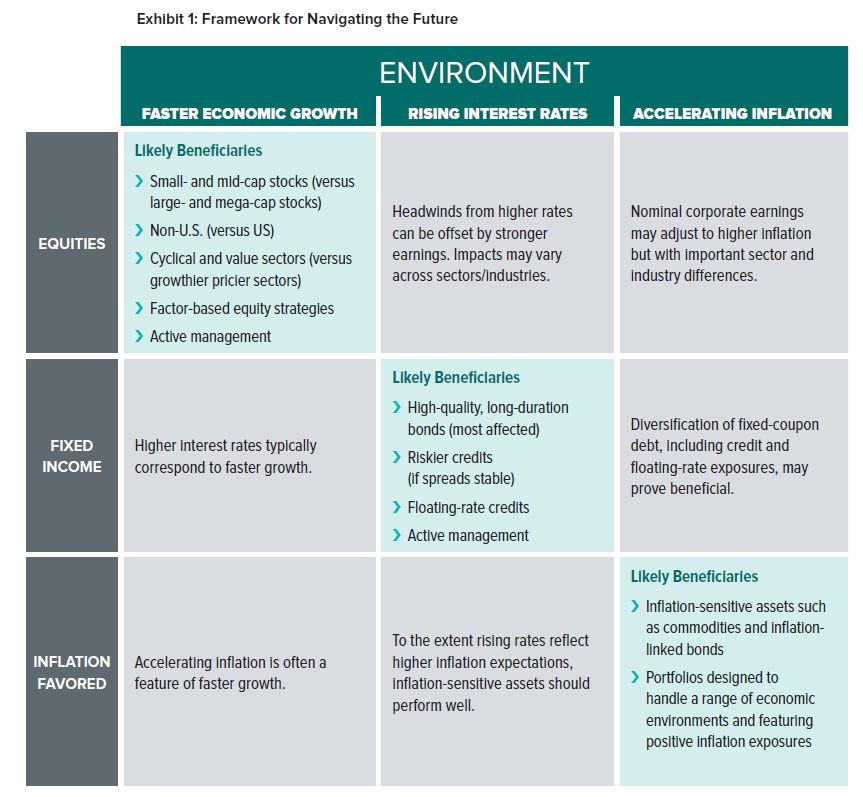

The impending recovery is likely to spur faster economic growth, higher interest rates, and accelerating inflation. Historically, these forces are closely interrelated and can have meaningful impacts across asset classes. We constructed a post-COVID-19 “road map” to help investors think about and navigate financial markets in the quarters and years ahead. To keep things simple, we categorized asset classes at a very high level (equities, fixed income and inflation-favored) and we focused most closely on three relationships that we think are fairly intuitive:

- Faster economic growth and equity markets

- Higher interest rates and fixed-income markets

- Accelerating inflation and inflation-favored assets

The resulting road map is shown in Exhibit 1 on the next page.

The impact of faster growth on equity markets

Continued vaccine expansion should eventually foster a return to pre-COVID-19 levels of economic activity—boosted by pent-up business and consumer demand, still-supportive fiscal measures, and accommodative central-bank policies. Higher interest rates and inflation could pose challenges for equities, but the effects should vary by sector, industry and geography.

Within equity markets, we believe an acceleration of economic growth will likely favor:

- Cyclical sectors and industries over less cyclical sectors and industries

- Smaller companies over larger companies (especially richly priced, mega-cap, technology-oriented names that outperformed in 2020 and for several years before)

- Non-U.S. stocks over U.S. stocks

- We believe active management and SEI’s factor-based framework could prove especially helpful in this type of environment.

The impact of higher interest rates on fixed-income markets

Faster economic growth accompanied by accelerating inflation should put renewed upward pressure on interest rates. This would have important implications for the bond market, as rising interest rates put downward pressure on the prices of existing bonds—an effect that is most pronounced for higher-quality, longer-duration securities.

We witnessed a fairly dramatic such fall in long-dated government-bond prices when interest rates made a sharp upward adjustment during the first quarter of 2021. Meanwhile, riskier credits such as high-yield bonds held up relatively well. High yield could persist as a bright spot for fixed income under rising rates as long as default expectations don’t pick up meaningfully. Floating-rate securities, typically backed by bank loans and consumer credit, could outperform given their lower sensitivity to rising rates (again, only as long as the default outlook doesn’t deteriorate).

As we see it, the upshot here is threefold:

1. Active management should prove helpful in fixed income, as with equities.

2. Despite the headwinds created by higher interest rates, bond returns will likely remain positive1 (we will detail this in a forthcoming paper).

3. High-quality bonds should continue to offer solid portfolio-diversification benefits given their low correlation to stock-market returns.

The impact of accelerating inflation on inflation-favored assets

When constructing portfolios at SEI, we carefully take into account high or accelerating inflation as a risk because it can wreak havoc on a generic stock-and-bond portfolio that lacks effective diversification against rising inflation. The disinflationary environment of the last four decades—marked by steadily falling inflation—has supported the performance of these simplified portfolios, and a shift toward higher inflation could spell trouble for many of them. In our view, the likeliest scenario will see sharply accelerating inflation in the short-term (due both to year-over-year comparisons with the steep drop in prices at the onset of COVID-19 lockdowns and lingering supply bottlenecks) and slightly higher longer-term inflation (due to strong economic growth and accommodative fiscal and monetary policies).

However, a more durable shift in the policymaking zeitgeist toward even larger fiscal deficits and more concerted central-bank activism would risk dislodging and raising longer-term inflation expectations—which many of today’s investors may have never experienced. To mitigate inflation risk, we typically espouse strategic exposures to inflation-favored assets like commodities, inflation-linked bonds and specialized equity portfolios. We believe these positions could prove their worth in the quarters and years ahead.

SEI’s view

Of course, it’s important to consider some of the risks to our outlook and, by extension, this road map.

An obvious risk is the emergence of COVID-19 variants capable of causing substantial “breakthrough” infections among vaccinated people and thus delaying a full reopening of the global economy. Other risks that are important to monitor include continuing vaccine distribution inequities and widespread hesitancy to take vaccines in parts of the world where they are available.

Premature tightening of fiscal and monetary policies could also put the brakes on a robust recovery. While it should be noted that U.S. fiscal policy is currently doing a lot of the heavy lifting for the global economy (most countries are running smaller deficits in 2021 than they did in 2020, while the U.S. Treasury is planning to keep the taps open), fiscal policies are unlikely to become restrictive overall in the near-term. And while a small number of central banks are beginning (or at least considering) a slowdown of their asset purchases, we expect this will happen only gradually—and they are unlikely to increase interest rates meaningfully in the next year or two.

Investor risk appetite will be important to monitor as a flight to safety would likely undermine the global reflation trend and support for riskier assets. In economic terms, reflation refers to inflation rising from a below-average level back toward its long-term trend. We typically view reflationary periods as economic regimes where both growth and inflation are accelerating.

Finally, there are interesting questions about business and household behaviors that will take time to answer. For example, a permanent shift toward higher saving, lower consumption and decreased investment would mean a weaker global recovery, all else equal.

Despite these important risks and some choppiness in recent economic data, the trend toward a strong recovery still looks intact. As such, we believe our post-COVD-19 roadmap should serve investors well.

Glossary of Financial Terms

Active management: Active managers aim to outperform a specific index, or benchmark. An active manager will continuously monitor and make changes to investments in an attempt to maximize returns.

Cyclical: Cyclical stocks and sectors are those whose performance is closely tied to the economic environment and business cycle.

Factor: Factors are market inefficiencies that can be capitalized upon to improve risk-adjusted investment returns.

Factor-based equity strategies: SEI’s factor-based equity strategies employ a rules-based approach to portfolio construction that provides systematic exposure to factors.

Factor-based framework: SEI’s factor-based framework refers to our factor research and, by extension, our factor-based investment strategies. Our framework employs composite indexes of underlying ratios that we have determined to be appropriate measures of factors such as value, momentum and stability.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Flight to safety: A flight to safety occurs during periods of market stress when investors sell higher-risk assets in favor of purchasing lower-risk assets.

Floating-rate credit: A floating-rate credit is a debt investment with interest payments that float or adjust periodically based upon a predetermined benchmark.

Inflation-favored assets: Inflation-favored assets include commodities, inflation-linked bonds, specialized equity portfolios and other assets that have a positive relationship with the rate of inflation.

Long duration: Duration is a measure of risk in bond investing and indicates how price-sensitive a bond is to changes in interest rates. Duration is measured in years and securities with longer durations are more sensitive to interest-rate changes.

Mega-cap stocks: Mega-cap stocks are companies with market capitalizations over $200 billion.

Monetary policy: Monetary policy relates to decisions by central banks to influence the amount of money and credit in the economy by managing the level of benchmark interest rates and the purchase or sale of securities. Central banks typically make policy decisions based on their mandates to target specific levels or ranges for inflation and employment.

Risk appetite: Risk appetite refers to the amount of risk that investors are willing to accept in their investment portfolios.

Risky credit: A risky credit is a debt instrument that carries higher credit or default risk and typically compensates investors with higher yields.

Value: Value stocks and sectors are those that are considered to be cheap and are trading for less than they are worth.

Yield: Yield is a general term for the expected return, in percentage or basis points (one basis point is 0.01%), of a fixed-income investment.

Zeitgeist: Zeitgeist refers to the spirit of the time, or the general trend of thought or feeling characteristic of a particular period of time.

Important Information

This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events or a guarantee of future results. Positioning and holdings are subject to change. All information as of the date indicated. There are risks involved with investing, including possible loss of principal. This information should not be relied upon by the reader as research or investment advice, (unless you have otherwise separately entered into a written agreement with SEI for the provision of investment advice) nor should it be construed as a recommendation to purchase or sell a security. The reader should consult with their financial professional for more information.

Statements that are not factual in nature, including opinions, projections and estimates, assume certain economic conditions and industry developments and constitute only current opinions that are subject to change without notice. Nothing herein is intended to be a forecast of future events, or a guarantee of future results.

Certain economic and market information contained herein has been obtained from published sources prepared by other parties, which in certain cases have not been updated through the date hereof. While such sources are believed to be reliable, neither SEI nor its affiliates assumes any responsibility for the accuracy or completeness of such information and such information has not been independently verified by SEI.

There are risks involved with investing, including loss of principal. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Past performance is not a reliable indicator of future results. Investment may not be suitable for everyone.

This material is not directed to any persons where (by reason of that person’s nationality, residence or otherwise) the publication or availability of this material is prohibited. Persons in respect of whom such prohibitions apply must not rely on this information in any respect whatsoever.

The information contained herein is for general and educational information purposes only and is not intended to constitute legal, tax, accounting, securities, research or investment advice regarding the strategies or any security in particular, nor an opinion regarding the

appropriateness of any investment. This information should not be construed as a recommendation to purchase or sell a security, derivative or futures contract. You should not act or rely on the information contained herein without obtaining specific legal, tax, accounting and investment advice from an investment professional.

Information in the U.S. is provided by SEI Investments Management Corporation (SIMC), a wholly owned subsidiary of SEI Investments Company (SEI).

Information provided in Canada by SEI Investments Canada Company, the Manager of the SEI Funds in Canada.

Information issued in the UK by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Investments in SEI Funds are generally medium- to long-term investments.

SIEL has appointed SEI Investments (Asia) Limited (SEIAL) of Suite 904, The Hong Kong Club Building, 3 Jackson Road, Central, Hong Kong as the sub-distributor of the SEI UCITS funds. SEIAL is licensed for Type 4 and 9 regulated activities under the Securities and Futures Commission (“SFC”)

This information is being made available in Hong Kong by SEIAL. The contents of this document have not been reviewed by any regulatory authority in Hong Kong. You are advised to exercise caution in relation to the offer. If you are in any doubt about any of the contents of this document, you should obtain independent professional advice.

This information is made available in Latin America FOR PROFESSIONAL (non-retail) USE ONLY by SIEL.

Any questions you may have in relation to its contents should solely be directed to your Distributor. If you do not know who your Distributor is, then you cannot rely on any part of this document in any respect whatsoever.

Issued in South Africa by SEI Investment (South Africa) (Pty) Limited FSP No. 13186 which is a financial services provider authorised and regulated by the Financial Sector Conduct Authority (FSCA). Registered office: 3 Melrose Boulevard, 1st Floor, Melrose Arch 2196, Johannesburg, South Africa.