Monthly Market Commentary :US Dollar Takes a Dip

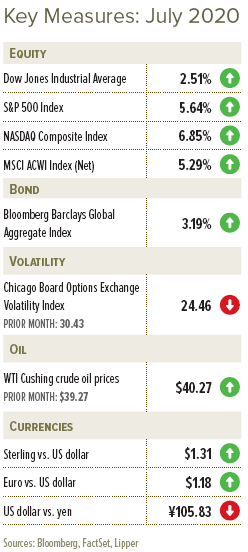

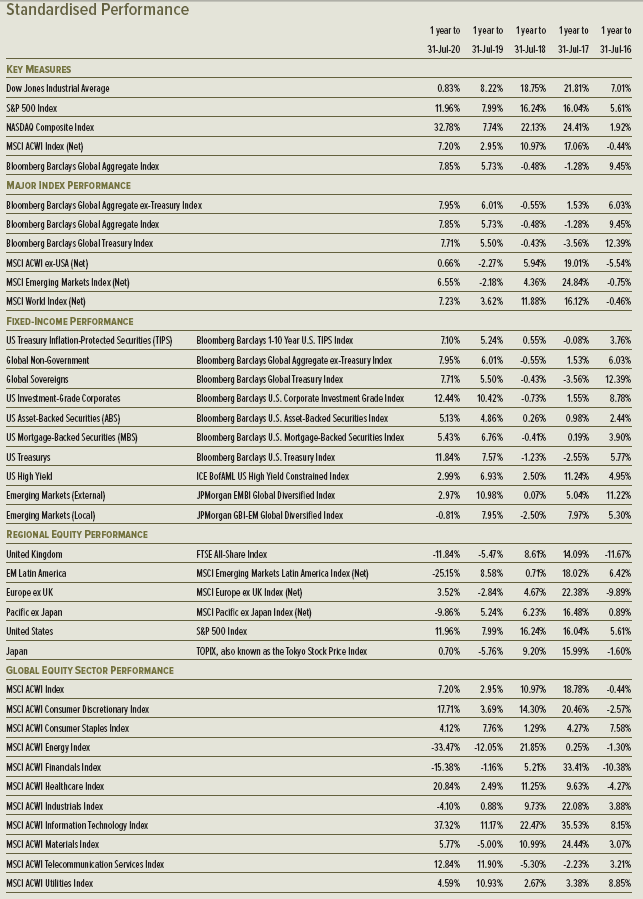

Global equity performance varied across base currencies by more than usual in July—ending slightly down in sterling, flat in euro, and much higher in US dollars. The remarkable dispersion was a result of the US dollar’s spot price dropping by more than 4% versus a basket of major currencies during the period, marking its largest one-month decline since September 20101.

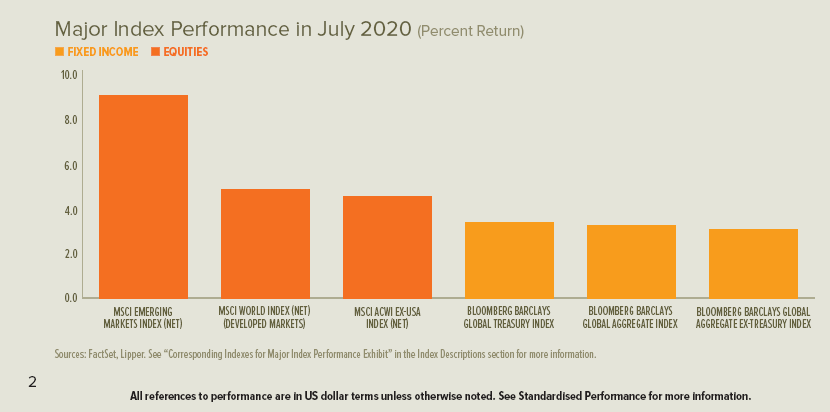

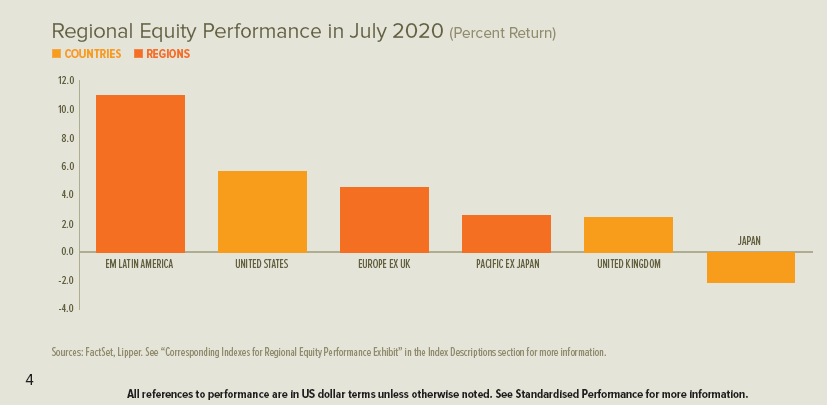

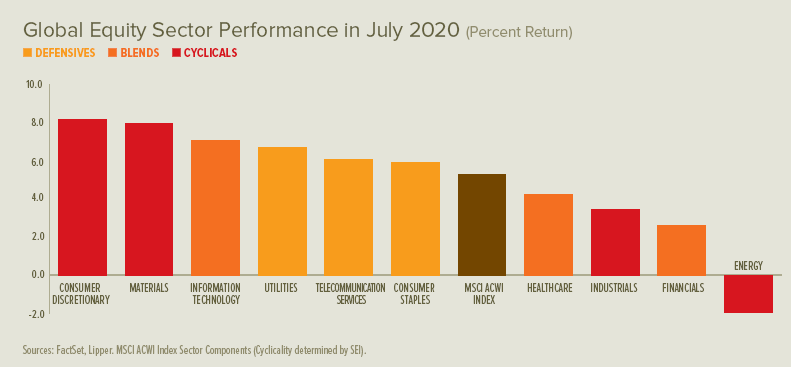

Emerging-market shares, led by China and Latin America, handily outperformed those of developed markets for July, while US equities outpaced other major developed markets. The gold futures price rose to an all-time high in US dollars during the month, finishing with a gain of more than 10%. Meanwhile, the West Texas Intermediate oil futures price increased by $1.00 during July, to end the period at $40.27; OPEC+ (the Organization of the Petroleum Exporting Countries, led by Saudi Arabia—plus Russia) announced plans in mid-July to begin relaxing oil-output cuts that had been instituted earlier in 2020 to counteract falling oil prices.

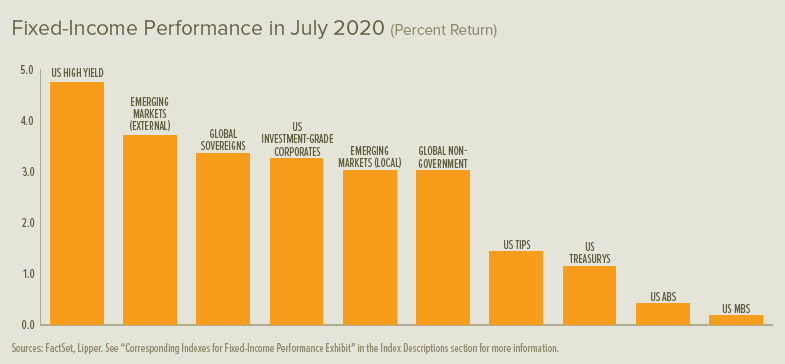

Government-bond rates generally declined across maturities in the UK, eurozone and US during July. UK gilt rates declined most dramatically in the intermediate-to-long-term segment of the yield curve; in the eurozone and US, government-bond rates dropped the most in the longest maturities.

The wide-ranging labour-market support that the UK’s Job Retention Scheme has provided was set to begin receding at the end of July. Effective August, companies are required to begin paying the national insurance and pension contributions for their furloughed workers; companies must also pay 10% of their wages starting in September, and then 20% by October. This expanding burden-sharing raises the possibility that employers will need to permanently lay off workers.

Her Majesty’s Treasury (HM Treasury) announced a patchwork of programmes during July targeted at bolstering dining and tourism in the UK. Restaurants and pubs, which opened their doors in July for the first time in several months, are expected to benefit from reduced taxes on food and non-alcoholic drink sales (from 20% to 5%); the tax cut also applies to tourist attractions and travel accommodations. Additionally, a 50% dining discount (up to £10 per diner) is set to begin in August. HM Treasury also unveiled a work placement programme for young adults; it also suspended taxes on some home purchases.

The EU struck a landmark accord to help fund an economic recovery from COVID-19-induced containment measures. The agreement’s €1.8 trillion price tag includes a €750 billion recovery plan (with more than half the figure intended as grants and the balance as loans), as well as funding for EU budgets through 2027. In a first, EU members agreed to partially fund the deal by issuing common EU debt, thereby tightening the fiscal union between member countries.

At the end of July, US President Donald Trump’s administration was still negotiating new fiscal-stimulus terms with the US House of Representatives—despite the end-of-July expiration of enhanced unemployment insurance benefits and protections from eviction within housing supported by the federal government. During the month, the US government reached deals with several pharmaceutical companies (one American, three European) to supply a combined 200 million doses of their pending coronavirus vaccines at a total cost of over $4 billion.

The United States–Mexico–Canada Agreement (USMCA) took effect on 1 July, officially replacing the North American Free Trade Agreement (NAFTA), while closure of the US-Canada border was extended (with few exceptions) until 21 August.

Tension between the US and China intensified throughout July. In a break from previous US policy that said maritime disputes must be resolved peacefully through UN-backed arbitration, the Trump administration formally denounced China’s territorial claims in the South China Sea as illegitimate. The US also imposed sanctions in response to human rights abuses against Muslim Uighurs and ethnic Kazakhs in the Xinjiang region; China issued retaliatory sanctions against US senators who criticized the abuses. The US gave China 72 hours in late July to close its consulate in Houston, Texas, claiming that Chinese diplomats helped steal US medical research on COVID-19; China followed through on its vow to retaliate, closing the US consulate in Chengdu.

The UK suspended its extradition treaty with Hong Kong in early July to protest China’s new security law for Hong Kong; it also banned using technology that belongs to Chinese telecommunication company Huawei for Britain’s high-speed wireless network. At the end of July, Hong Kong postponed elections for the territory’s legislature until next year, citing a resurgence of COVID-19 cases; this prompted protests from democratic groups.

At least 68 countries and territories postponed elections between 21 February and 26 July, also citing concerns about COVID-19 containment, according to the Wall Street Journal; at least 49 countries and territories committed to holding their elections as scheduled2. The US general election is almost certainly going to proceed in early November, as is set by federal law; any delay would require approval by both chambers of the US Congress, and one has publically confirmed it would reject any postponement.

Economic Data

- Solid growth returned to the UK’s services sector, according to an early July report, while manufacturing continued to rebound at a steady and moderate pace. Mortgage approvals re-accelerated to about 40,010 in June after bottoming at approximately 9,270 in May; associated lending jumped from about £290 million to approximately £1.22 billion in the same period. The latest available information on UK gross domestic product (GDP) showed a contraction of 19.1% from March to May 2020.

- The recovery in eurozone manufacturing remained subdued in July, while services activity accelerated, according to a preliminary report. Across the euro area, the unemployment rate increased by 7.8% in June, from 7.7% in May. The first reading of second-quarter GDP for the eurozone showed a contraction of 12.1%, its largest quarterly drop on record3. Germany’s economy shrank by 10% for the second quarter,

- US manufacturing activity expanded at a modest rate during July; new orders accelerated, while employment continued to contract. Services sector activity essentially maintained pace during the month, according to an early report, after moving lower in June. New US jobless claims bottomed in mid-July at 1.3 million per week before increasing through the end of the month. The US economy shrank at a 32.9% annualised rate during the second quarter, its sharpest decline on record since 19474.

Central Banks

- The Bank of England’s Monetary Policy Committee did not hold a meeting during July. Following its mid-June meeting, the central bank announced that it would expand its stock of asset purchases (from an initial £200 billion increase announced in March) by another £100 billion to £745 billion.

- The European Central Bank (ECB) held its benchmark interest rates firm after a mid-July monetary policy meeting, and emphasised the demand for and utility of its asset-purchase and lending programmes.

- The US Federal Open Market Committee made no monetary-policy changes following its late-July meeting, but reiterated its commitment to using its full range of programmes to help support current economic challenges. During July, the Federal Reserve Board of Governors announced extensions of temporary U.S. dollar-liquidity-swap and repurchase-agreement facilities with other central banks through March 2021.

- The Bank of Japan (BOJ) made no changes following its mid-July monetary policy meeting, maintaining its short-term rate and its target rate for the 10-year Japanese government bond.

SEI’s View

Despite mounting infections, hospitalisations and deaths from the pandemic—as well as the unprecedented stoppage of global economic activity—stock markets around the world have managed to mount a resounding comeback.

Our working assumption is that there will likely be another significant wave of infections going into the fall-to-winter flu season. The question is, how disruptive will it be to the global economy?

Even if a sustainable economic recovery gets under way, investors seem to be ignoring the possibility that it may be a long time before most companies achieve previous levels of profitability. The after-tax profit margins of US domestic businesses were already on a declining trend before the onset of the virus and shelter-in-place orders.

Margins around the globe will likely remain well below their previous peaks as long as COVID-19 is a severe health threat. Most businesses, to one degree or another, are expected to endure lower sales, higher costs and a decline in productivity. There also will probably be a deadweight loss for industries needing extra inventory on hand in order to guard against future shortages and supply-chain disruptions caused by periodic flare-ups of the virus. “Just-in-time” inventory management will turn into “just-in-case” inventory management, tying up cash. Supply chains will likely be diversified over time, a process that was already under way as a result of the trade war between China and the US.

The extraordinary March-to-April lockdown in the US necessitated fiscal measures unparalleled in both scope and speed of implementation. The result has been a tsunami of red ink. As of April 2020, the Congressional Budget Office projected the deficit will reach nearly 18% of US GDP in 2020, and improve to only 10% of US GDP in 2021. US debt relative to GDP is forecast to rise to 108% by the end of fiscal year 2021 versus 79% at the end of fiscal year 2019.

These are unsettling numbers. Many investors may wonder whether such a surge in government debt will provoke an economic crisis even after the pandemic runs its course. We don’t think that it will. The US has a large, dynamic economy and deep capital markets.

The policies pursued by the Federal Reserve have also served to keep interest rates low. Its balance sheet has ballooned this year, far exceeding the increases logged by the ECB or the BOJ.

The US certainly is not alone in engaging in a huge fiscal response that is then monetised by the central bank. In our opinion, governments are treating the fight against COVID-19 like they would a war. As many resources as possible are being thrown into the fight, supported by debt issuance that is absorbed primarily by the central banks.

Those who remember the 1970s are understandably worried by the inflationary potential of such extraordinary debt monetisation. If it does lead to inflation, it probably won’t be any time soon, in our opinion. Given our view that the economy will remain below full utilisation of labour or productive capacity for the next few years, we believe inflation is unlikely to break out of the 0%-to-3% range of much of the past decade.

Investors do not seem too concerned about the speed of Europe’s economic recovery or the impact of the health crisis on countries’ fiscal positions. The bond yields of the most economically-fragile countries remain close to those of German bund yields, although spreads have widened from pre-pandemic levels. The ECB has been quite successful in short-circuiting the liquidity crisis and flight-to-safety that threatened the euro area’s financial structure.

The COVID-19 crisis has pushed Brexit concerns off the front pages. As the 31 December transition deadline nears, it could become an economic factor nearly as important as a second wave of the virus. The UK and EU should probably reach a deal on their trading relationship by at least 31 October to allow time for countries to approve the treaty into law before the end of 2020. Any free-trade agreement would require the UK to agree to permanently align its rules and regulations to those of the EU on an array of matters. The UK would essentially bear much of the EU membership cost without having a voice at the table that sets the rules. It is becoming increasingly likely that there either will be a modest agreement that includes tariffs, or (in the worst-case scenario) a no-deal result that falls back on the World Trade Organization’s most-favoured-nation rules.

While many factors determine equity performance, it has correlated in the emerging-market space with the extent of economic disruption caused by the virus. Asian and central European countries have pulled back the most on their mandates to restrict movement and social interaction. Latin America and India have eased some of those constraints, but not nearly as much as the other two regions. We continue to keep close tabs on China, as it was the first to lock down and first to unlock activity. We expect recovery patterns elsewhere in the world to follow that of China.

Central banks in the emerging world are also doing their part to help restore their economies. Interest rates have come down in almost every country in recent months, to record-low levels in many cases. In addition, a long list of emerging-country central banks—including those with shakier reputations, such as South Africa and Turkey—are either buying or planning to buy their government’s debt. We think this debt-monetisation may lead to an inflation problem in the future.

It’s been said many times that bull markets climb a wall of worry. Maybe now they must learn to swim through waves of worry that include:

- The possibility of a second wave of COVID-19 infections (or, arguably, a continuation of the first wave in some countries) forcing another round of extensive lockdowns and shelter-in-place orders that could lead to a double-dip recession

- A possible breakdown of political consensus regarding the way forward as economies struggle to regain strength

- The likelihood that economic recovery will take at least a year, and likely longer—and that few economies are apt to rebound fully to pre-pandemic levels, even if most countries manage to avoid a disruptive second wave of the virus

- Expectations that companies will face higher costs and increased inefficiencies; taxes will almost certainly rise across many economies in the years ahead; and bankruptcies and defaults will climb as government aid programs end

We believe that an ebb and flow of assorted concerns in the coming months will continue to spark volatility across financial markets. Such periods of instability are expected in any long-term investing plan; as such, we are just as prepared as always at SEI to navigate the current wave of deep uncertainty.

Glossary of Financial Terms

Bear market: A bear market refers to a market environment in which prices are generally falling (or are expected to fall) and investor confidence is low.

Bull market: A bull market refers to a market environment in which prices are generally rising (or are expected to rise) and investor confidence is high.

Debt issuance: Debt issuance is when companies or governments raise funds by borrowing money from lenders. The borrower, or issuer, agrees to pay the lender (or bondholder) interest along with full repayment in the future.

Fiscal policy: Fiscal policy relates to decisions about government revenues and outlays, like taxation and economic stimulus.

Fiscal Stimulus: Fiscal stimulus refers to government spending intended to provide economic support.

The United States–Mexico–Canada Agreement (USMCA): USMCA is a trade deal struck by the three named counties, which took effect on 1 July, thereby replacing the North American Free Trade Agreement (NAFTA).

Index Descriptions

S&P 500 Index: The S&P 500 Index is an unmanaged market-capitalisation-weighted index comprising 500 of the largest publicly-traded US companies and is considered representative of the broad US stock market.

Important Information

Data refers to past performance. Past performance is not a reliable indicator of future results.

Investments in SEI Funds are generally medium- to long-term investments. The value of an investment and any income from it can go down as well as up. Investors may get back less than the original amount invested. Returns may increase or decrease as a result of currency fluctuations. Additionally, this investment may not be suitable for everyone. If you should have any doubt whether it is suitable for you, you should obtain expert advice.

No offer of any security is made hereby. Recipients of this information who intend to apply for shares in any SEI Fund are reminded that any such application may be made solely on the basis of the information contained in the Prospectus. This material represents an assessment of the market environment at a specific point in time and is not intended to be a forecast of future events, or a guarantee of future results. This information should not be relied upon by the reader as research or investment advice regarding the funds or any stock in particular, nor should it be construed as a recommendation to purchase or sell a security, including futures contracts.

In addition to the normal risks associated with equity investing, international investments may involve risk of capital loss from unfavourable fluctuation in currency values, from differences in generally accepted accounting principles or from economic or political instability in other nations. Bonds and bond funds are subject to interest rate risk and will decline in value as interest rates rise. High yield bonds involve greater risks of default or downgrade and are more volatile than investment grade securities, due to the speculative nature of their investments. Narrowly focused investments and smaller companies typically exhibit higher volatility. SEI Funds may use derivative instruments such as futures, forwards, options, swaps, contracts for differences, credit derivatives, caps, floors and currency forward contracts. These instruments may be used for hedging purposes and/or investment purposes.

While considerable care has been taken to ensure the information contained within this document is accurate and up-to-date, no warranty is given as to the accuracy or completeness of any information and no liability is accepted for any errors or omissions in such information or any action taken on the basis of this information.

This information is issued by SEI Investments (Europe) Limited, 1st Floor, Alphabeta, 14-18 Finsbury Square, London EC2A 1BR which is authorised and regulated by the Financial Conduct Authority. Please refer to our latest Full Prospectus (which includes information in relation to the use of derivatives and the risks associated with the use of derivative instruments), Key Investor Information Documents and latest Annual or Semi-Annual Reports for more information on our funds. This information can be obtained by contacting your Financial Adviser or using the contact details shown above.

SEI sources data directly from FactSet, Lipper, and BlackRock, unless otherwise stated.

The opinions and views in this commentary are of SEI only and should not be construed as investment advice.